trending

trending

Despite growing institutional interest in account-to-account payments, US consumers remain largely unaware of the “Pay by Bank” option, according to new research from Trustly.

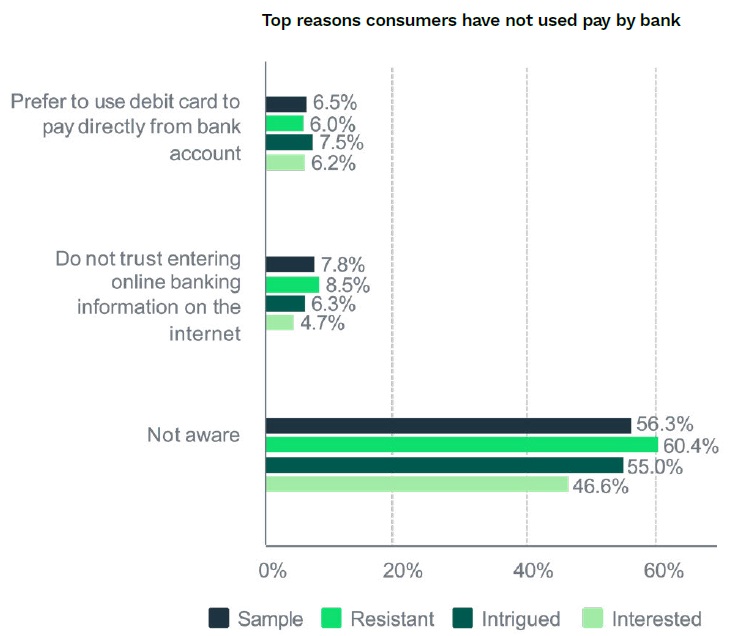

The findings reveal that more than half of American consumers (56%) do not know the service exists — a knowledge gap that dwarfs other barriers such as security concerns or a preference for debit cards.

Pay by Bank, which allows customers to pay merchants directly from their bank account without relying on card networks, has long been heralded as a cost-efficient alternative to credit and debit.

Yet in the US, uptake has lagged behind markets such as Europe, where open banking is reshaping payment flows.

The latest survey of 2,225 consumers highlights that the challenge is less about product design than visibility.

Incentives Drive Interest — If Consumers Know the Option Exists

The report categorises consumers into four groups: early adopters (6%), interested (18%), intrigued (22%) and resistant (53%). Crucially, resistance often stems from indifference rather than hostility.

The report categorises consumers into four groups: early adopters (6%), interested (18%), intrigued (22%) and resistant (53%). Crucially, resistance often stems from indifference rather than hostility.

When presented with rewards or discounts, attitudes shift significantly. Eighty-one per cent of respondents expressed interest in pay by bank when incentives were attached, compared with 47% without them.

Among current users, 41% said they would consider extending its use to ridesharing, suggesting non-retail sectors may provide fertile ground for expansion.

Even among those initially opposed, two-thirds indicated they would reconsider if discounts or loyalty benefits were offered.

Younger demographics, particularly Gen Z and millennials, were most receptive, with over 40% interested in using the method for moving funds between bank and brokerage accounts.

Beyond Retail: Where Adoption Could Take Hold

The research suggests that pay by bank may gain traction first in industries where consumers already link accounts directly, such as sports betting, investments or mobility services.

These sectors could act as natural testbeds for broader adoption. Ease of use is another underappreciated strength. Nearly four in ten existing users cited simplicity as the main appeal, but among non-users only one in five recognised convenience as a potential benefit.

Overcoming Habit and Inertia

The report points to a dual challenge: raising awareness while offering incentives strong enough to shift entrenched habits, such as reaching instinctively for a debit card.

For now, pay by bank remains a niche product in the US, but the combination of targeted education, clear communication of benefits, and integration into everyday use cases could propel it beyond early adopters.

Comments