trending

trending

Zelle has entered 2025 with unprecedented momentum, reporting 2 billion transactions and nearly $600 billion in payments during H1 2025.

The network, operated by Early Warning Services, recorded double-digit growth across key metrics, cementing its role as one of the most widely used person-to-person (P2P) payment systems in the US.

The total value of payments surged 23% year-on-year, up from $481 billion to close to $600 billion, while transaction volumes increased 19%.

The total value of payments surged 23% year-on-year, up from $481 billion to close to $600 billion, while transaction volumes increased 19%.

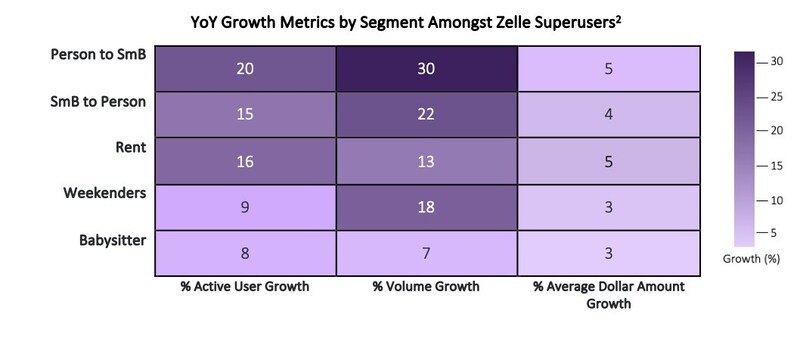

Small business usage represented the fastest-growing segment, with payments to small enterprises rising by 31% to 180 million.

For Zelle, this marks a shift from being primarily a peer-to-peer transfer tool towards becoming a core utility for entrepreneurs, freelancers and service providers.

Denise Leonhard, Zelle’s general manager, underscored its significance: “Whether it’s rent, childcare or paying a small business, Zelle is an essential and foundational part of everyday life for millions of Americans.”

A Barometer of Everyday Spending

Zelle’s growth also tells a broader economic story. The service reached its biggest-ever monthly volume in August, when users sent $108 billion.

Behind these figures lie indicators of household spending behaviour, with rent, utilities and childcare payments consistently topping the list of most common transactions.

Even as headlines warn of weakening consumer sentiment, Zelle’s data points to resilience.

Person-to-small-business transfers rose 30%, with average payment sizes increasing 5%, suggesting that households continue to support local services.

Meanwhile, payouts from small businesses to individuals rose by 22%, reinforcing Zelle’s growing role in the gig economy, where fast access to funds often makes the difference between meeting essential expenses or not.

Housing pressures are visible in Zelle’s dataset.

The average rent payment grew 5%, from $914 to $958, alongside a 13% increase in rent-related transactions.

Payments for childcare rose more modestly – 7% in volume and 3% in average size – but point to families continuing to invest in support networks despite cost pressures.

Discretionary activity also remains present: weekend payments grew 18%, with stable average transaction sizes, signalling cautious but ongoing spending at markets, local events and small retailers.

Fighting Fraud with ‘Trust Signals’

Rapid adoption of any payments network inevitably raises questions about fraud and scams.

Here, Zelle points to a long-standing partnership with Early Warning Services, a company with more than three decades of experience in combating financial crime.

Working alongside banks, law enforcement and federal agencies, Early Warning deploys predictive fraud detection and AI-based monitoring at scale.

Zelle’s approach is rooted in what it calls “Trust Signals” – billions of behavioural and transactional data points that allow fraudulent actors to be detected and excluded before money changes hands.

Participating banks and credit unions benefit from this infrastructure at no extra cost, helping them block suspicious transfers in real time.

The result, Zelle claims, is an extraordinarily low fraud incidence: just 0.02% of transactions are reported as scams or fraud.

For comparison, Americans statistically face higher odds of food poisoning (3%), car accidents (2%), or even unusual mishaps such as toilet-related injuries (0.07%) than encountering fraud on Zelle.

While no system is foolproof and criminal tactics evolve constantly, these figures underline the scale of the network’s protective architecture.

From Convenience to Critical Infrastructure

What began as a peer-to-peer payments convenience has evolved into a critical component of the US financial ecosystem.

With billions flowing monthly for rent, childcare, small business services and gig economy wages, Zelle is no longer simply a “nice-to-have” app.

It has become an essential rail underpinning household liquidity and community-level commerce.

As 2025 progresses, the question is less about whether Zelle will keep growing, and more about how it continues to balance speed and accessibility with the relentless challenge of fraud prevention.

For now, its trajectory suggests it will remain a barometer of American economic life – one small transfer at a time.

Comments