trending

trending

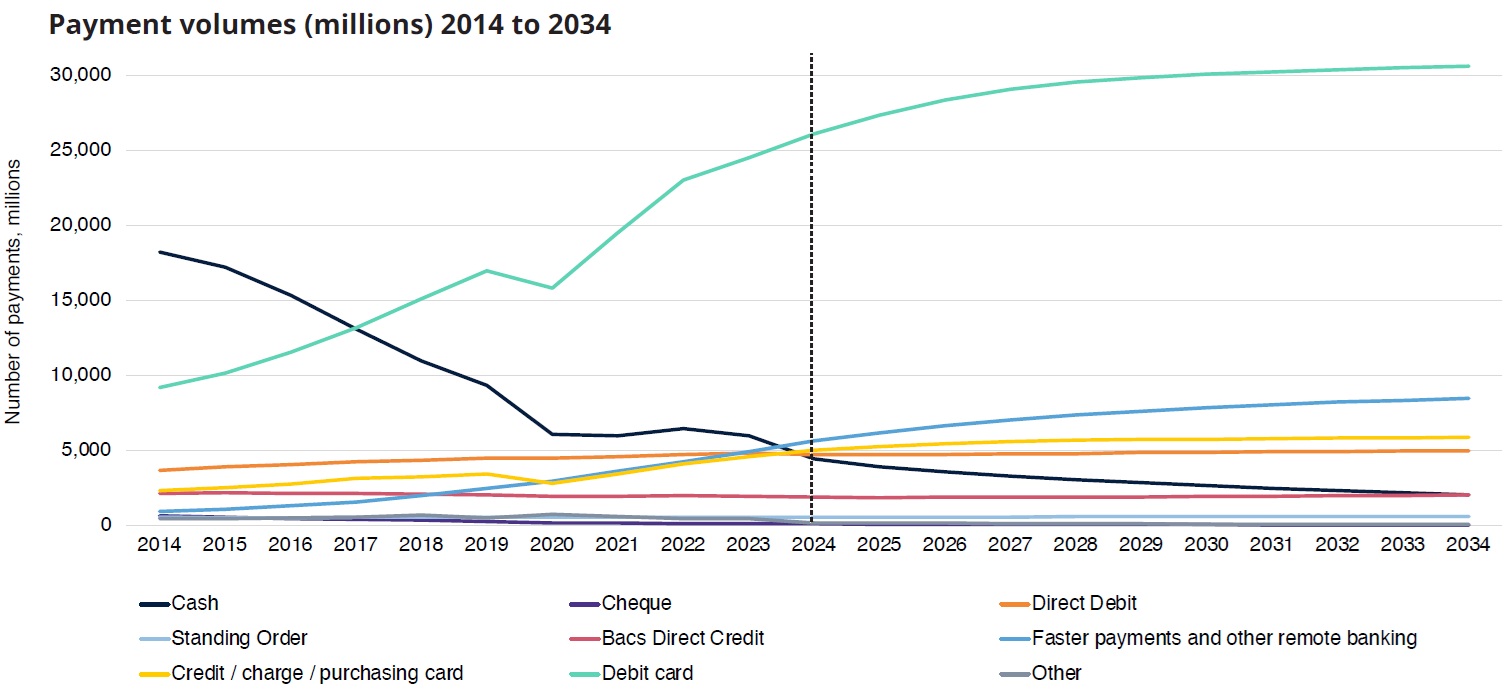

The UK payments landscape is undergoing one of the most profound shifts in its history. Figures from UK Payment Markets 2025 show that nearly 49 billion transactions were made in 2024, revealing striking patterns in how Britons are choosing to pay.

Debit cards remain the dominant force, mobile wallets are reshaping contactless payments, and cash—once the backbone of daily transactions—has slipped below 10% of all payments for the first time.

Debit cards consolidate dominance

In 2024, debit cards accounted for more than 26 billion transactions, representing just over half of all payments in the UK.

This sustained dominance reflects their ubiquity: nearly every adult holds at least one debit card, and acceptance continues to widen among small businesses that now use simple smartphone or tablet-based readers.

The growth of debit card use is also tied closely to mobile wallets.

Most consumers registering for services such as Apple Pay or Google Pay default to linking their debit cards.

As a result, mobile payments are not cannibalising debit cards but rather amplifying their role as the engine of UK payments.

Looking ahead, debit card volumes are projected to rise to over 30 billion by 2034, fuelled by contactless expansion, online commerce and near-universal acceptance across merchants.

Contactless reaches maturity—but mobile takes over

Contactless payments, once the star of Britain’s payment revolution, are showing signs of maturity.

Growth in 2024 slowed to just 3%, compared with 7% in 2023 and much higher rates in the years following the pandemic.

The technology has become the norm, with 153 million contactless cards in circulation—nearly nine in ten of all payment cards.

What is shifting rapidly, however, is the way contactless payments are being made.

For the first time, half of UK adults used mobile contactless payments regularly in 2024, up sharply from a third the year before.

Younger consumers continue to lead, but adoption is spreading across all demographics.

Mobile wallets are also expanding beyond the high street into online shopping.

Retailers increasingly offer “Pay with Apple Pay” or “Pay with Google Pay” at checkout, simplifying the process to a single click and eliminating repetitive data entry.

This frictionless convenience is pushing wallets further into the mainstream, potentially positioning them as the next growth engine in UK payments.

Cash slips further down the rankings

Cash’s long decline accelerated in 2024, with transactions falling to 4.4 billion, or just 9% of the total. For the first time, cash dropped below Direct Debit, Faster Payments and credit cards in usage.

Despite this, cash retains a loyal core of users. For some, it remains an essential budgeting tool or a preferred method in specific contexts.

The report suggests that while the UK will not become a fully cashless society in the next decade, cash will continue to lose ground, falling to around 4% of payments by 2034. The policy challenge is ensuring continued access to cash even as demand diminishes.

Faster Payments rise as a mainstream option

One of the most striking developments of 2024 was the surge in Faster Payments. With 5.6 billion transactions, this method overtook cash and Direct Debit to become the UK’s second most frequently used payment type.

Mobile banking is the key driver: three-quarters of UK adults now use mobile apps, with many extending beyond balance checks to making transfers, paying bills, and managing personal finances.

Businesses too are shifting towards real-time settlement. Half of all business payments in 2024 were made via Faster Payments, surpassing Bacs Direct Credit.

This signals a structural change in corporate payments, with speed and certainty increasingly prioritised.

Open Banking is poised to amplify this trend. “Pay by Bank” services, still in their infancy, could offer retailers a lower-cost alternative to card payments, further embedding account-to-account transfers in the UK’s payment mix.

Buy Now, Pay Later enters the mainstream

Another headline from 2024 was the rise of Buy Now, Pay Later (BNPL) services. One in four UK adults used BNPL at least once, compared with just 14% in 2023.

Adoption is highest among younger demographics, with more than a third of 25- to 34-year-olds using such services.

This shift underscores the evolving nature of consumer credit. While credit card volumes continue to grow modestly—rising to 5 billion payments in 2024—BNPL is competing for the same slice of discretionary spending.

The longer-term question is whether BNPL becomes a lasting fixture or simply a stepping stone to new credit innovations.

The future: incremental but irreversible change

The UK payments market is not heading for a sudden revolution but for a steady evolution. Debit cards and mobile wallets will remain the backbone of consumer payments, while Faster Payments gain strength as both consumers and businesses embrace real-time options.

By 2034, card payments are expected to account for 67% of all transactions, contactless to represent 43%, and cash just 4%.

Cheques will all but vanish, while Direct Debit, Bacs and standing orders will endure as niche but stable methods.

Ultimately, the direction of travel is clear: a more digital, mobile and real-time system, layered with consumer choice.

The challenge for policymakers and providers is to ensure resilience, inclusivity and competition, so that innovation benefits every segment of society.

To find more on the UK markets payments and statistics CLICK HERE

Comments