trending

trending

The UK’s Payment Systems Regulator (PSR) has published its first APP fraud and scams performance report.

Authorised push payment (APP) fraud happens when a fraudster tricks someone into sending a payment to an account outside of their control.

There are more incidents of APP fraud than any other crime type in the UK, with APP fraud accounting for 40% of fraud losses in 2022.

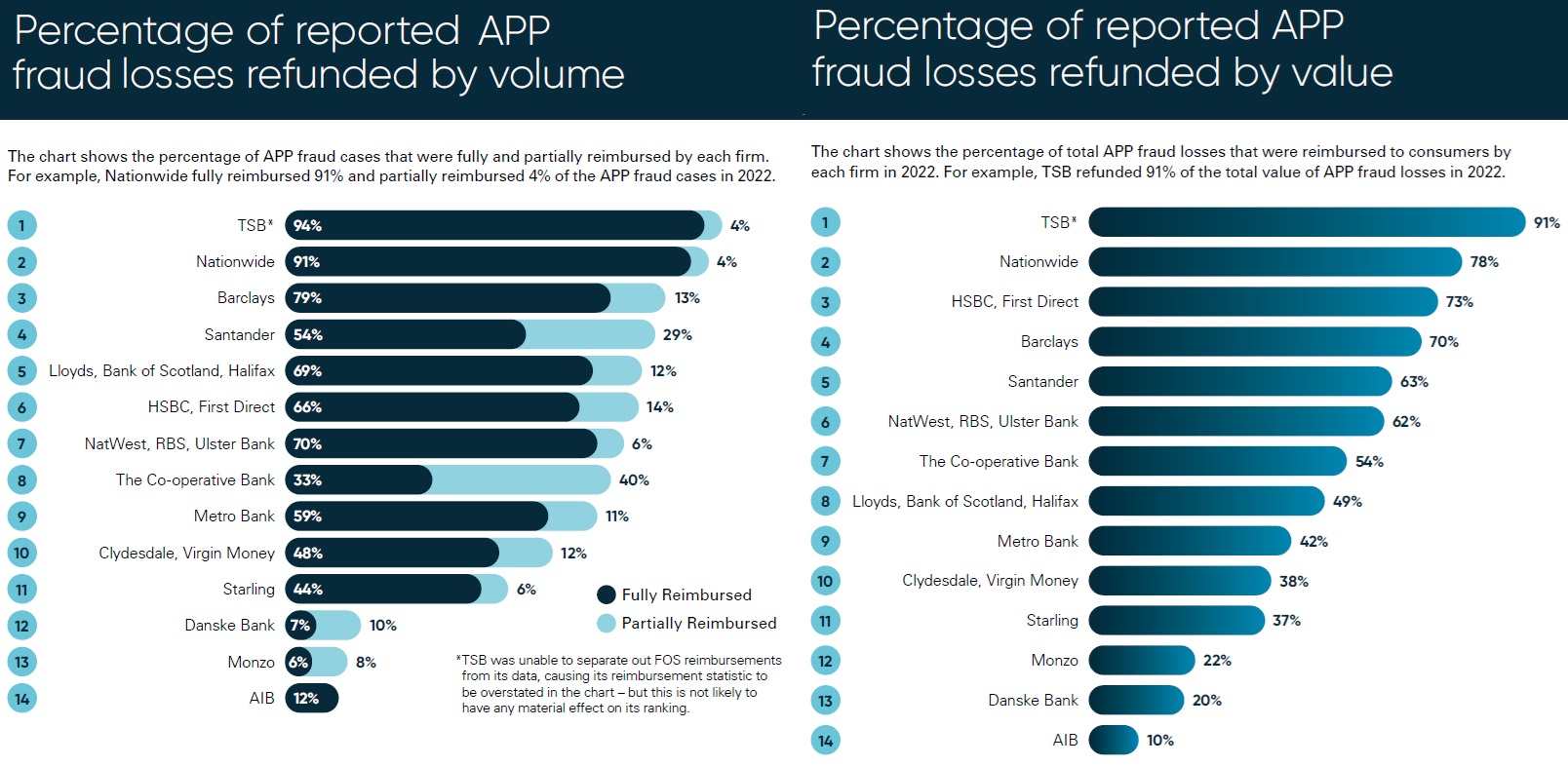

The report shows 2022 data indicating how well the 14 largest banking groups in the UK have performed with:

- The reimbursement of victims

- The level of APP fraud sent

- The level of APP fraud received

This is the most comprehensive data published to date, covering 95% of Faster Payments in the UK by value and volume.

However, because there are many other payment firms in addition to the 14 largest, the report also shows the data for nine other smaller firms that were identified as being in the top 20 highest receivers of fraud.

These firms represent a disproportionately high level of fraud received for their size.

The aim of the report is to incentivise the entire payments ecosystem to make greater strides in preventing fraud and improving outcomes for victims.

The data considers APP fraud where the reported victim is a consumer or a small business or charity with an annual income of less than £1 million.

All cases included in the data were closed in 2022 and occurred across Faster Payments in the UK, which allows customers to send money electronically in real time.

There is more that individual payment service providers (PSPs) and the industry as a whole can do, and the PSR would like to see significant improvements presented in the data in subsequent reports.

APP Fraud in charts

Looking at just two of the data sets, currently PSPs are not required to reimburse victims of APP fraud.

However, in the last three years we have seen considerable progress in improving reimbursement for victims. The Contingent Reimbursement Model (CRM) code is a voluntary code launched in 2019 to establish good industry practice in preventing APP fraud and respond to its growth.

As part of the Code, member PSPs reimburse victims of APP fraud. Since its introduction, we have seen positive outcomes for consumers with higher rates of reimbursement. However, it has not driven consistent outcomes, with reimbursement rates differing significantly across members. AIB, Danske Bank, Monzo and TSB are the only four directed PSPs not in the CRM code.

The PSR notes it has seen examples of industry innovation, notably from TSB and Nationwide who had the highest reimbursement levels of the major UK banks in 2022:

- Since 2019 TSB has offered a fraud refund guarantee. In most cases where a customer reports an APP fraud to TSB, they automatically reimburse the customer.

- Since 2021, Nationwide has provided a scam checker service. Customers can talk to Nationwide about a payment. If the service reviews a transaction that turns out to be fraudulent, Nationwide fully reimburses the customer unless the service advised them not to make the payment.

The rates of reimbursement for many firms are encouraging and it presents a positive cultural shift across the payments sector. We see different strategies and approaches by PSPs to reimbursement which could account for some having higher reimbursement rates than other PSPs.

It could also account for differences in rates of cases accepted as being eligible for reimbursement and the level of responsibility borne by customers themselves (resulting in more partial payments).

Comments