trending

trending

The battle against financial crime in the US is shifting rapidly as scams emerge as the single most damaging category of fraud for banks.

New research suggests scams accounted for 27 per cent of US financial institutions’ fraud losses in 2024, more than doubling from just 12 per cent the previous year.

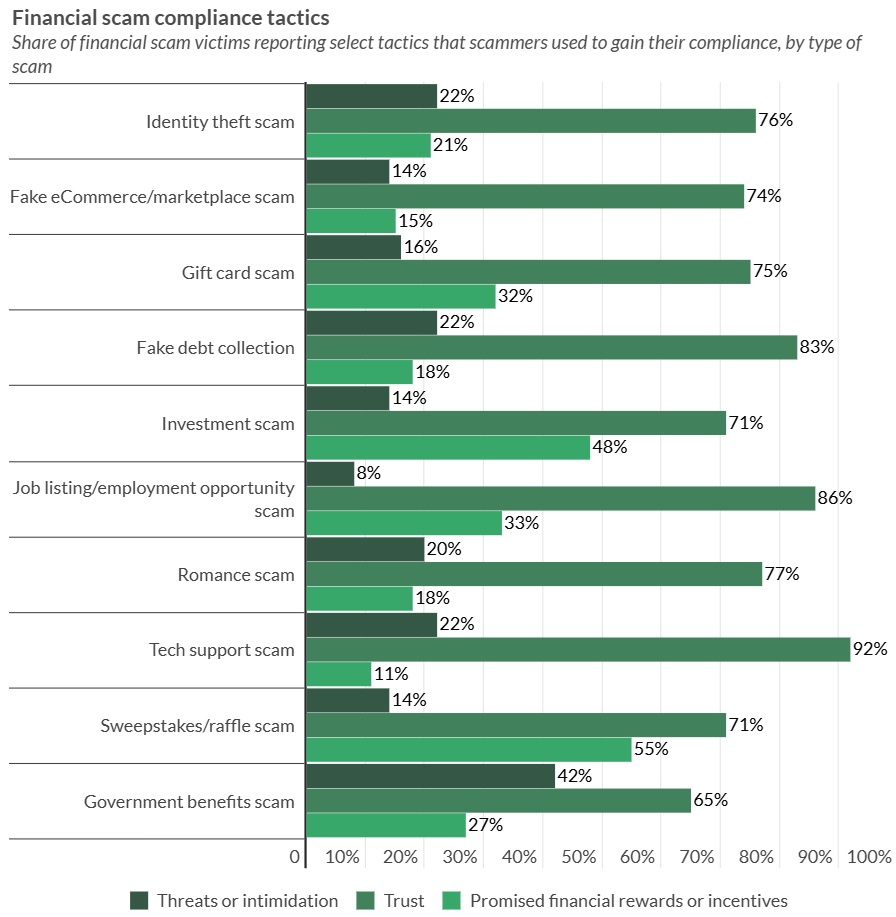

A study by PYMNTS Intelligence, based on responses from more than 10,000 consumers, highlights how criminals have borrowed directly from the tactics of digital marketers.

Rather than scatter-gun approaches, fraudsters are segmenting their targets by age, income and behaviour, then crafting outreach strategies designed to feel routine to the victim.

The result is both significant financial harm and a gradual erosion of trust in banking channels, digital commerce and payments.

Channel Familiarity Breeds Risk

The survey underscores how effective this personalisation has become.

Among Gen Z consumers, 21 per cent of scams began on social media, reflecting platforms where younger users spend much of their time.

For baby boomers and older adults, email (23 per cent) and phone calls (21 per cent) were the most common entry points – precisely the communication methods those demographics perceive as trustworthy.

The choice of first contact also mirrors the scam type.

Almost half of e-commerce fraud attempts (42 per cent) began via online platforms, while debt collection scams were most often initiated by telephone (39 per cent), imitating legitimate industry practice.

Tailored Deception by Life Stage

The research points to distinct patterns across life stages.

The research points to distinct patterns across life stages.

Early career consumers are disproportionately targeted by employment scams: nearly 8 per cent of Gen Z victims reported losses to fraudulent job listings, making them three times more vulnerable than older groups.

Conversely, seniors were more than three times as likely as Gen Z to be duped by fake e-commerce offers, while sweepstakes scams skewed heavily toward older, financially insecure consumers.

High-income households are more commonly drawn into fraudulent investment schemes, while lower-income households face a higher incidence of benefit-related fraud.

In every case, scammers adapt their scripts to exploit financial motivations and anxieties unique to the target group.

Dynamic Fraud Needs Dynamic Defence

The findings underline that fraud prevention can no longer rely solely on static rules or generic consumer alerts.

Banks are being urged to adopt advanced analytics and behavioural monitoring that detect out-of-pattern behaviour in real time. Consumer education also needs to evolve, with scenario-based training shown to be more effective than broad warnings.

As scammers optimise their messages with the precision of growth marketers, banks must meet customers in equally personalised ways.

The strategic priority is not simply to block new tricks, but to build adaptive systems that can identify and intercept scams before they reach customers.

Comments