trending

trending

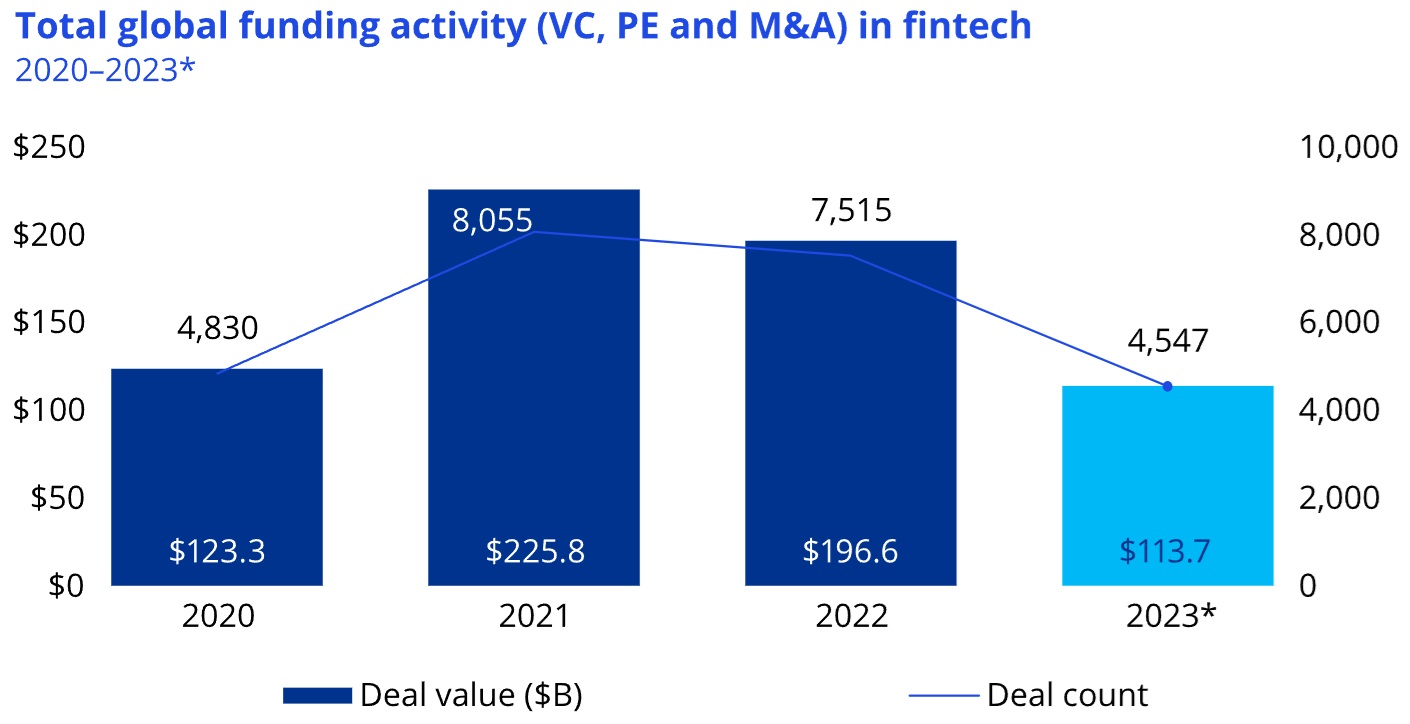

After reaching a record $238.9 billion across 7,321 deals in 2021, total global fintech investment across M&A, PE, and VC fell to $164.1 billion across 6,006 deals in 2022.

While results were substantially lower compared to 2021’s peak highs, 2022 was not a poor year as a whole.

In fact, it was the third best year for fintech investment ever and the second strongest year for deal volume, according to the Pulse of Fintech – a bi-annual report published by KPMG highlighting global fintech investment trends.

2023 was a difficult year

2023 was a difficult year for the fintech market globally, with both total fintech investment ($113.7 billion) and the number of fintech deals (4,547) experiencing their weakest results since 2017.

A storm of global challenges — from the high interest rate environment and stubbornly high inflation in many jurisdictions, to conflicts in the Ukraine and Middle East — combined with concerns about valuations and the barren exit environment, saw fintech investors becoming increasingly cautious with their investments.

The year-over-year decline in fintech investment occurred across all key regions, with APAC experiencing the largest drop — from $51.3 billion in 2022 to just $10.8 billion in 2023.

EMEA saw investment fall from $49.6 billion to $24.5 billion over the same timeframe.

The Americas showed the most resilience, with fintech investment dropping from $95.4 billion in 2022 to $78.3 billion in 2023.

At a jurisdictional level, the US attracted two-thirds of all fintech funding during 2023 ($73.5 billion).

The payments space continued to account for the largest share of fintech funding among the fintech subsectors, despite a drop from $57.9 billion to $20.7 billion between 2022 and 2023.

Of the major fintech subsectors, only proptech and insurtech saw total investment rise year-over-year, with proptech investment rising from $4.1 billion to $13.4 billion, and insurtech investment growing from $5.9 billion to $8.1 billion.

From a technology perspective, despite a drop in funding in 2023, AI remained a clear leader, attracting over $12.1 billion in fintech investment.

Looking at both 2023 as a whole, and at H2 2023 in particular, fintech investor sentiment can be characterized as restrained.

Consider some of the key trends 2023 was a difficult year seen across the fintech sector over the past six months:

- Increased scrutiny of potential fintech deals, including a very strong focus on profitability and avoidance of down rounds.

- Strengthening interest in B2B fintech solutions aimed at enablement rather than on B2C-focused business models.

- Enhanced focus on partnerships and alliances.

- Growing interest in the applicability of AI and generative AI across the fintech sector.

- Continued focus on embedded financial products, particularly payments and lending, as part of transition to opening banking.

Looking ahead to H1 2024, investment in the fintech sector globally is expected to remain relatively soft, although investment will likely begin to pick up as interest rates reduce with common consensus that this will be in Q3/Q4.

AI will likely continue to be a key focus, in addition B2B solutions.

M&A activity is also expected to rise as investors look for opportunities to buy distressed assets.

One area that has bucked the trend in the fintech life stage, is start-up and seed/ pre-seed funding.

While the deal sizes are small as investors spread their risk, the number of deals completed is at an all time high.

Clearly, investors are testing and learning which next wave, fintech business model, will be commercially desirable.

Comments