trending

trending

As digital channels grow in importance, a new buzzword rears its head: phygital payments – a blend of the physical and digital – but is phygital really a thing, or just more marketing hype?

Those of us who’ve been around a while are used to how hype cycles work.

In the last five years alone we’ve had the metaverse, blockchain, crypto and most recently generative AI – all hyped by the media and marketing companies as the Next Big Thing.

Fintechs have been founded on the basis of some of these technologies – and maybe that’s one reason for the fintech funding crisis.

Too many big ideas that, in the end, failed to deliver on the metrics that matter such as revenue and profit.

Reality: supporting the internet since 1999

That said, it’s important not to become cynical.

Anyone tempted towards cynicism should remember the words of British newspaper executive Richard Desmond in 1999, who claimed the internet was a fad and that newspaper sales would not be affected.

Easy to see how that turned out.

Likewise in payments – after listening to Wall Street tell us they always knew crypto was a scam, it now appears to be making something of a comeback.

Likewise in payments – after listening to Wall Street tell us they always knew crypto was a scam, it now appears to be making something of a comeback.

Blockchain has some useful applications in trading and logistics, and the metaverse … well, maybe the less said the better.

It’s a commonplace that payments was transformed by the pandemic – but in reality, all COVID-19 did was speed up existing trends.

Sure, e-commerce grew by more than 20% per year between 2020 and 2022 – but it had been experiencing double-digit growth for the ten years before that.

Likewise companies such as DoorDash, JustEat and the “click and collect” sector had been growing strongly. All the pandemic did was to speed up the transformation.

Trends towards internet and mobile banking that had been around for years likewise were given a shot in the arm by lockdown.

All of which is not to say that people were entirely comfortable with these practices – they simply had no other choice.

“Post-pandemic, spending on cards has returned, while e-commerce growth and digital wallet use have calmed down.”

As the world recovers from the pandemic, one notices some interesting trends – such as the fact that e-commerce growth in developed markets has slowed rapidly to between three and seven percent, and that spending on cards outside Asia has shot up, while the shift towards digital wallets has slowed.

At the height of lockdown, Visa released survey data suggesting seven in ten US shoppers still preferred using cards when shopping online – while India’s most prestigious new payment product is a metal card that customers control via an app.

Across Europe, the number of bank branches has been falling for many years – yet last year, KPMG said the number of customers visiting each bank branch grew by 25%.

Reading the runes: clients want both

Making sense of these trends isn’t easy if one accepts the long-promulgated story that the world is going digital, we’ll be using our phones for everything and we’ll all end up paying with a well-placed flutter of the eyelid in the direction of our phones.

However, it may be that the future will be rather different to what has been predicted. And in many ways, the future that’s emerging makes a lot of sense from a wide range of viewpoints.

“Banks are beefing up the utility and security of their cards via apps, while new use cases for cards are emerging through “tap to phone” products.”

Let’s take the humble payment card.

Long touted as the world’s next dinosaur and a dead cert to be replaced by digital wallets, in fact it remains popular with Western consumers and – outside Asia and some African markets – still the first port of call when it comes to shifting from physical cash to electronic payments.

In many ways, this makes sense: doing everything via mobile device is all very well, but what happens when that device is lost, stolen or compromised?

In response, banks are beefing up the utility and security of their card products by allowing consumers to control them via app, while new use cases for cards – such as ID confirmation or e-commerce authentication – are beginning to emerge through so-called “tap to phone” products.

In-person shopping: phygital made real

Perhaps the biggest change in consumer behaviour, and where we see the physical and digital coming together most clearly, is when it comes to how people spend money.

These days, shoppers will browse for items using the internet, then purchase in-store. This particularly applies to categories like clothing, jewellery and other high-value items where physical feel is important.

Equally, many consumers will view items in-store then purchase online to avoid queues.

In that regard, the advent of “pay anywhere” POS systems mounted on mobile devices is another example of digital and physical systems coming together – and one which promises to make in-store shopping a faster and more pleasant experience.

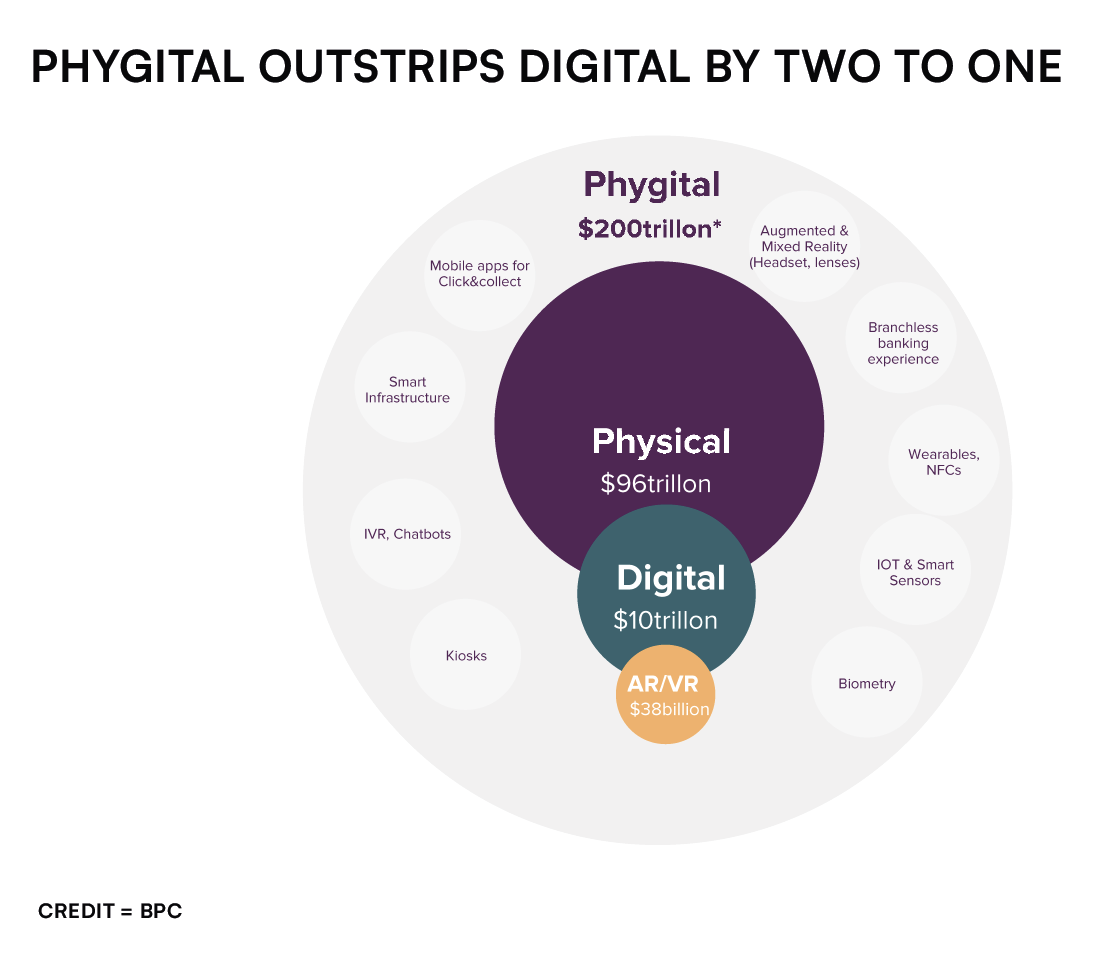

Taken together, it feels as if, for once, the hype around “phygital” payments is deserved. Estimates from digital payment services specialists BPC seem to confirm this.

They estimate that the opportunity for “phygital” payment services dwarfs pure digital payments by a factor of two to one – and see numerous advantages not just for consumers, but for banks and retailers as well.

Comments