trending

trending

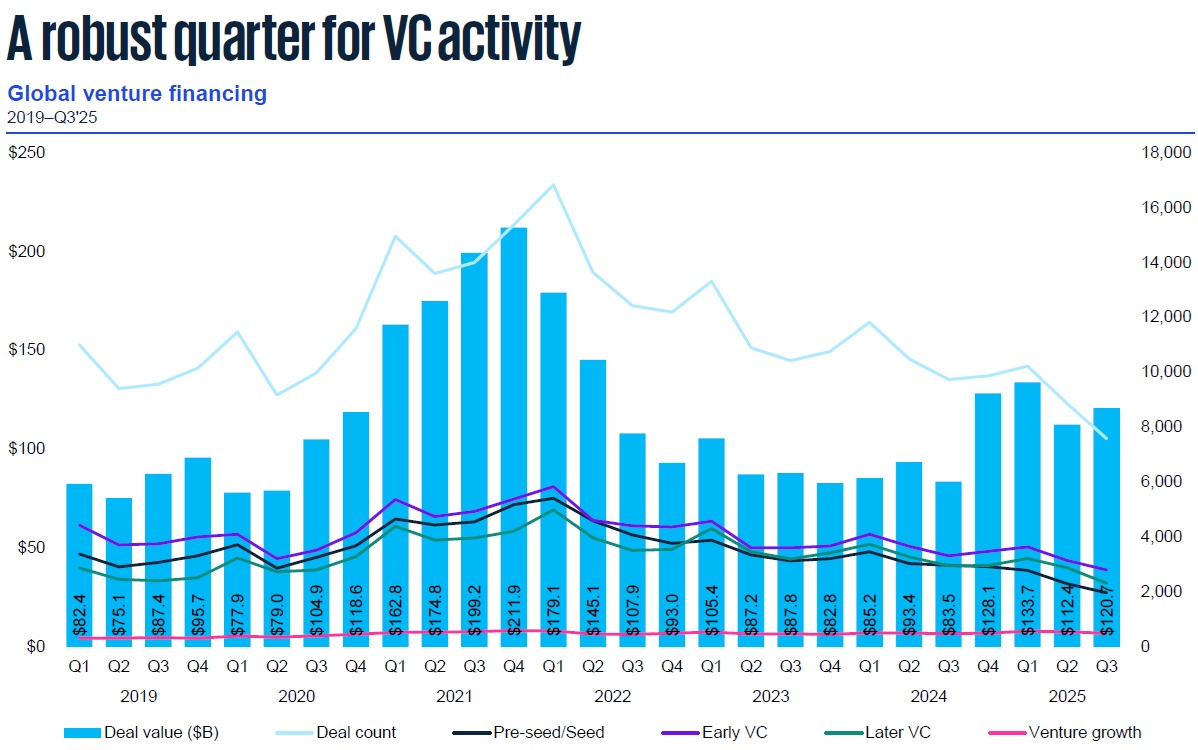

Global VC investment surged to $120 billion in Q3 2025, marking the fourth consecutive quarter of robust funding activity and signalling a sustained revival in investor confidence.

The rise, up from $112 billion in the previous quarter, reflects a decisive rebound in market optimism, underpinned by the explosive growth of artificial intelligence (AI) and a long-awaited reopening of exit markets.

AI Powers a New Wave of Venture Activity

AI remained the driving force behind global VC investment throughout Q3, accounting for many of the largest funding rounds worldwide.

From Anthropic AI’s $13 billion raise and xAI’s U$10 billion in the US to Mistral’s and Nscale’s US$1.5 billion rounds in Europe, investors continued to pour unprecedented sums into companies developing foundational models and next-generation AI platforms.

The AI boom is no longer confined to model training and infrastructure.

Venture investors are now targeting AI-powered applications, spanning sectors from defencetech and healthtech to quantum computing and energy efficiency.

As Conor Moore, Global Head of KPMG Private Enterprise, noted, “If startups aren’t embracing AI in some way, shape, or form, it’s very difficult for them to attract attention.”

This momentum extends beyond the major markets.

In Asia, Australia-based Firmus secured A$330 million ($220 million), while China’s MiniMax AI raised $300 million and South Korea’s Rebellions closed a $244 million round.

The AI ecosystem has become the gravitational centre of global venture investment—drawing capital not only into core AI companies but also into enabling industries such as data centres, semiconductors, and energy infrastructure.

Regional Breakdown: The Americas Lead, Europe Rises, Asia Lags

The Americas dominated global VC investment, attracting $85.1 billion across 3,474 deals—more than 70% of total global funding.

The US accounted for the lion’s share, at $80.9 billion, driven by a handful of mega-deals in the AI space. Canada and Brazil also performed well, with Cohere’s $600 million round and a 12-quarter high of $1.1 billion in Brazil, primarily focused on fintech.

Europe maintained its upward trajectory, recording $17.4 billion across 1,625 deals, overtaking Asia to become the second-largest regional VC market.

The UK and France led the continent’s activity, with fintech and quantum computing among the top sectors. Notable raises included Rapyd Financial Network ($500 million) and Finland-based IQM ($320 million).

Asia, by contrast, continued to experience subdued deal flow, with $16.8 billion invested across 2,310 deals.

Persistent geopolitical tensions and slower economic growth kept investors cautious. Still, large rounds in China, India, and Australia offered signs of underlying resilience.

Exit Markets Reopen and Investor Sentiment Strengthens

One of the most significant developments of the quarter was the revival of IPO markets, especially in the US and parts of Asia. Global exit value surged to $149.9 billion, a 15-quarter high and the strongest showing since late 2021.

The US accounted for nearly half this figure, while Asia’s exits rose sharply to $38 billion. Europe also saw robust improvement, reaching $27.8 billion.

Renewed exit activity has restored liquidity to the ecosystem, providing long-awaited relief to investors and signalling that capital recycling is returning after several dormant years.

This in turn has buoyed confidence, even as global fundraising remains weak—totalling just $80.7 billion so far this year, putting 2025 on track to underperform 2024’s eight-year low.

Outlook: AI and Robotics to Drive Q4 Stability

Looking ahead to Q4 2025, analysts expect global VC activity to remain steady, fuelled by continued enthusiasm for AI and growing investor interest in robotics and defensetech.

In emerging markets, fintech remains the leading sector of focus, with particular strength in Latin America, Africa, and Southeast Asia.

The reopening of IPO markets is expected to support stronger exits into 2026, barring any prolonged US government shutdowns.

With optimism returning and liquidity slowly improving, the global VC market appears to be entering a more stable, constructive phase—driven by the technologies shaping the next generation of innovation.

As Moore observed, “The future is looking brighter for the VC market than it has in quite a while.”

Comments