trending

trending

The landscape of fintech in Indonesia is booming, driven by increasing digital penetration and positive investor engagement across this high-growth nation of nearly 300 million citizens.

This is a market with huge fintech potential, with large underserved and underbanked populations, low access to finance in MSMEs, and an open and encouraging government dialogue about leveraging fintech capabilities to bridge the financing gap.

In order to understand this landscape, Boston Consulting Group (BCG) gathered the voices of key stakeholders, including in-depth interviews with 20 industry leaders, backed by comprehensive surveys of customers and small- and medium-sized enterprises (SMEs) to build a clear picture of the current ecosystem, and its expected evolution.

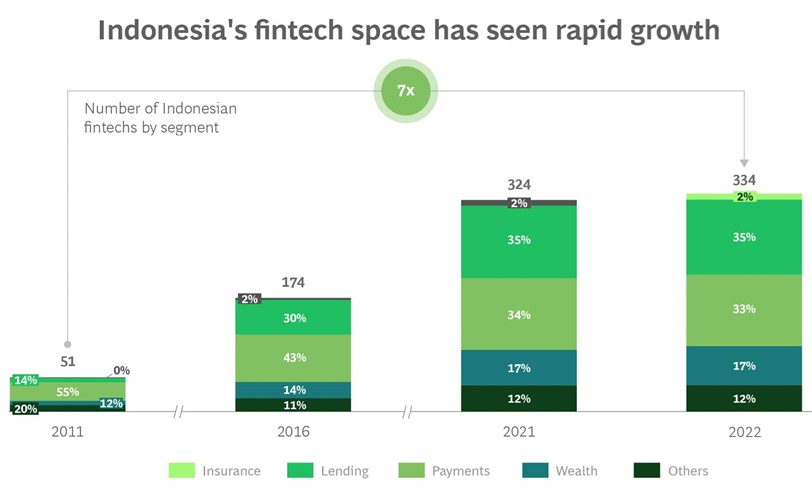

The number of fintech players in Indonesia increased six-fold over the last decade, rising from just 51 active players in 2011 to 334 in 2022.

While the first wave of growth was dominated by the payment segment, the vibrant modern ecosystem is a diverse landscape driven by lending, payments, and wealth.

Wealthtechs, fintech-focused software as a service, and insurance activities now represent a new, emerging driving force, with a number of fresh entrants operating in these segments, showing Indonesia’s fintech ecosystem is maturing beyond payments to include increasingly sophisticated products and services.

Customers begin to engage

Customer engagement with fintech offerings continues to surge.

In particular, the payment segment boasts over 60 million active users and is expected to grow at a rate of 26% annually between 2020 and 2025.

Meanwhile, in the lending space, there are more than 30 million active peer-to-peer (P2P) borrower accounts.

Additionally, the wealth segment is thriving with over 9 million retail investors.

Fintech SaaS is also experiencing a surge in adoption, with 6 million SMEs now using SaaS platforms. This marks a remarkable 26-fold expansion over the previous three years.

Transaction values also continue to grow, with more than $20 billion of e-wallet transactions in the period 2017–2021, a remarkable 123% CAGR.

Over $17 billion in loans were disbursed between 2017–2022, while a net asset value of over $20 billion in wealthtech and digital trading took place in 2021.

Investor sentiment

Investor sentiment remains encouragingly bullish for Indonesia’s fintech journey.

Equity funding into fintech soared to $1.5 billion in 2021.

While a significant portion of funding went towards payments and lending players, 2021 also represented a breakout year for wealthtech players, who received over $500 million in funding.

While the year 2022 saw a slight decline in the overall funding value—with global macro-economic concerns affecting investor sentiment—Indonesia still attracted funding of almost $1.4 billion, demonstrating the resilience of the ecosystem.

Investment into fintech in Indonesia in the period from 2020–2022 reached $3.2 billion, 4.6X the funding seen in the period from 2017–2019, demonstrating strong investor commitment.

While a large share of the funding has flowed to more mature companies, 60% of the deal volume has flowed to early-stage companies indicating a strong desire to invest in emerging innovation.

Investment trends also echo the diversification of Indonesia’s fintech market, with lending and payments no longer being the primary areas of interest.

While lending and payments remain important, there is increasing investment into wealthtech, insurtech, and fintech SaaS.

Fintech in Indonesia is a rapidly expanding space, with emerging players existing alongside more established products and operators.

Comments