trending

trending

After a challenging economic slowdown throughout 2022, global FinTech entered 2023 on cautious footing as economists and investors warned that ongoing macroeconomic tumults including lingering inflation, hawkish monetary policies, supply chain problems, and a potential recession would continue to dampen discretionary spending and dealmaking.

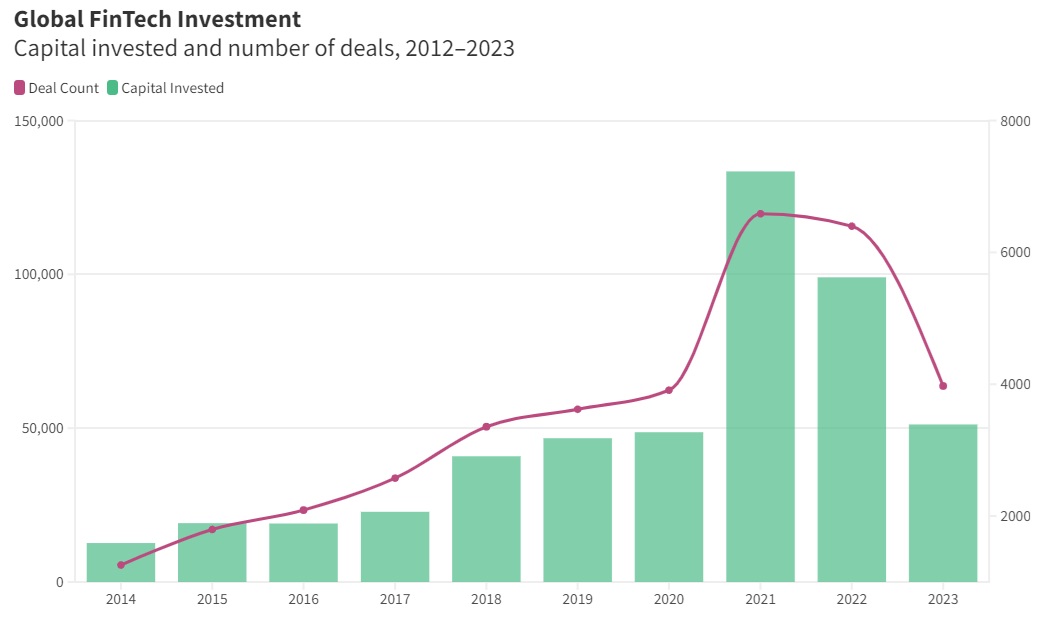

Global fintech investment dropped by a steep 48% in 2023 compared to 2022, with $51.2 billion dollars invested into the sector across 3,973 deals from Seed through Series I, according to data from Innovate Finance.

The venture market has entered the thick of a challenging, non-linear post-COVID recovery

Globally, early stage fintech investment remains strong, with seed rounds securing over $4 billion in 2023 despite headwinds, while later stage mega-deals ($100 million and above) are easing, suggesting lower growth-stage valuations and possibly a reluctance to issue new capital in this market environment.

The average deal size fell to $12.9 million from $15.5 million in 2022, although it is still higher than the average of $10.3 million recorded from 2012 – 2020.

Notably, FinTech has once again demonstrated its global reach and the pace of change internationally.

For the first time, Asian countries in the Top 10 delivered more investment than European countries in the Top 10.

The US is still leading the global ranking in 1st place, followed by the UK in 2nd place and with India in 3rd place. Moreover, the Top 5 largest deals of 2023 took place across the US, UK, India and UAE.

The US took the lion’s share of deals with $24.2 billion invested across 1,530 deals, a 44% decrease from 2022.

This included Stripe’s $6.9 billion deal in H1 2023, without which the US would have fallen 60% year-on-year.

The UK reported $5.1 billion across 409 deals (a 65% drop from 2022) yet well outpacing third place India which brought in $2.5 billion across 187 deals, also down 63% on 2022.

Despite a significant slowdown in venture capital investment in the vast majority of the globe, there are some indicators of recovery that position key markets for a stronger 2024 from the second half of the year onward.

In its report, Innovate Finance dives into a granular analysis of the current health of FinTech and examines the emerging trends in investment and innovation.

“The industry must also bear in mind that “most of the “tourist” capital has left the market leaving an opportunity on the supply side for those with conviction to invest,” says Jay Wilson, Partner at Albion VC.

“In the near term this may lead to currently funded companies with weaker investor syndicates and uncertainty about ongoing support from the existing capital base.”

Global Overview

Global investment in FinTech reached $51.2 billion across 3,973 deals in 2023, a steep drop from $99 billion in 2022. Deal count also declined 38%, whilst the average deal size remains strong at $12.9 million, an indicator of investor confidence in the FinTech industry.

Furthermore, while the total of global investment in FinTech represents a decline from the previous two years, it is 10% higher than the last pre-covid year of 2019 (investment in UK FinTech in 2023 was 11% higher than in 2019).

Q2 and Q3 2023 reported circa $10 billion each of investment, the lowest since early 2020, although Q4 2023 saw a quarter-on-quarter increase of c.13%, the first notable increase since Q3 2021 (excluding the impact of the Stripe deal in Q1 2023).

But what does the data say about both founder and investor behaviour?

“Macro uncertainty meant that any company that has the option to defer fundraising,” says Tim Levene, CEO of Augmentum, “through runway extension either by cutting costs, rising bridge funding, or both – chose that route.

The stabilisation of interest rates in Q3 and Q4 marked the first sign of a shift in market sentiment towards a more positive outlook.

Rates are expected to remain elevated through 2024 and it will undoubtedly be a challenging year on many fronts, but with confidence starting to return to public and private markets we look forward to a return in investment activity.”

While macroeconomic uncertainty persists, pockets of seed stage resilience hint at ongoing innovation amid adversity, with 17% of total funding, higher than pre-Covid levels.

Though allocation of funding is more selective, sustained activity into promising ventures might indicate a self-correction of markets towards realistic longer-term growth.

Comments