trending

trending

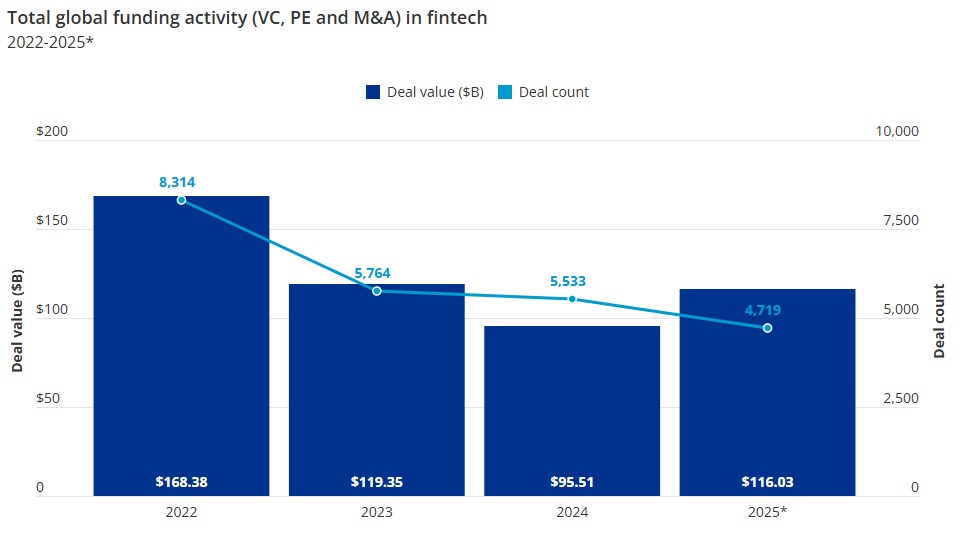

Global fintech investment staged a notable recovery in 2025, marking a decisive break from three consecutive years of contraction. Total funding rose to $116 billion across 4,719 deals, up from $95.5 billion in 2024.

Yet beneath the headline growth lies a more nuanced story: investors are deploying more capital, but into fewer companies. Deal volume fell to its lowest level since 2017, underscoring a market defined less by exuberance and more by discipline.

The rebound was driven primarily by larger ticket transactions, as venture capital and private equity firms concentrated resources on scaled businesses with clearer paths to profitability.

While aggregate investment strengthened, the decline in deal count signals continued selectivity and a sustained aversion to early-stage risk.

Regional Divergence Shapes the Global Picture

The Americas retained their dominance, attracting $66.5 billion in 2025, of which the United States accounted for $56.6 billion.

EMEA followed with $29.2 billion, while Asia-Pacific activity softened, declining to $9.3 billion from $11.7 billion a year earlier.

Interestingly, although the US absorbed the largest share of capital in the second half of the year, two of the three largest transactions occurred elsewhere.

The UK’s Revolut secured a $3 billion venture raise, while Israel-based Sapiens International was taken private in a $2.5 billion deal backed by Advent.

Meanwhile, Intercontinental Exchange committed $2 billion to Polymarket. The dispersion of mega-deals beyond the US highlights the increasingly global nature of late-stage fintech capital.

Second-half investment moderated slightly to $56.3 billion, compared with $59.7 billion in the first half, suggesting a degree of caution as macroeconomic and geopolitical uncertainties persisted.

Digital Assets Regain Institutional Momentum

One of the most striking developments in 2025 was the resurgence of digital asset investment. Funding in the sector nearly doubled year-on-year to $19.1 billion.

Although still below the 2021 peak of $32.2 billion, the renewed momentum reflects growing regulatory clarity and institutional confidence.

In the United States, the passage of the GENIUS Act has provided a clearer framework for stablecoins, while the European Union’s Markets in Crypto-Assets Regulation (MiCA) came fully into force at the end of 2024.

Anticipated UK regulation by 2027 is further reinforcing the sense that digital assets are entering a more structured phase of development.

Stablecoins, asset tokenisation and tokenised money market funds attracted particular interest, alongside large venture rounds and IPO ambitions from maturing crypto-native firms. The focus now is on scale, infrastructure resilience and regulatory alignment.

Payments: Fewer Deals, Larger Stakes

Investment in payments remained broadly stable at $19.2 billion, marginally down from $20.4 billion in 2024. However, deal count dropped sharply to 542 — a nine-year low.

The message is clear: investors are favouring established platforms with demonstrable revenues over speculative early-stage plays.

Revolut’s $3 billion raise dominated the payments landscape in the first half, while India’s PhonePe secured $600 million.

The pattern reflects a broader recalibration within fintech: capital is returning, but it is more strategic, more concentrated and more demanding than in the exuberant cycle that preceded it.

Comments