trending

trending

As Europe races toward the December 2026 deadline for the implementation of the European Digital Identity Wallet (EUDIW) under eIDAS2, banks across the continent are confronting a rare inflection point.

The Mobey Forum’s recent report, Mapping the Business Case – Banks and the European Digital Identity Wallet, makes a compelling case that this is not just a compliance exercise, but a strategic opportunity to redefine the role of banks in digital society.

For financial institutions, the EUDIW represents more than a secure container for personal data.

It is a cornerstone for a new trust architecture – one that could transform how identity, credentials, and consent are managed across borders.

Banks that act decisively now could embed themselves more deeply into customers’ digital lives, while those that hesitate risk being side lined by more agile players, including Big Tech.

Divergent Opportunities in Divergent Markets

The report highlights that the strategic calculus for banks depends heavily on local market conditions.

The report highlights that the strategic calculus for banks depends heavily on local market conditions.

In countries with low digital identity penetration, particularly in Southern and Eastern Europe, banks are uniquely placed to lead adoption.

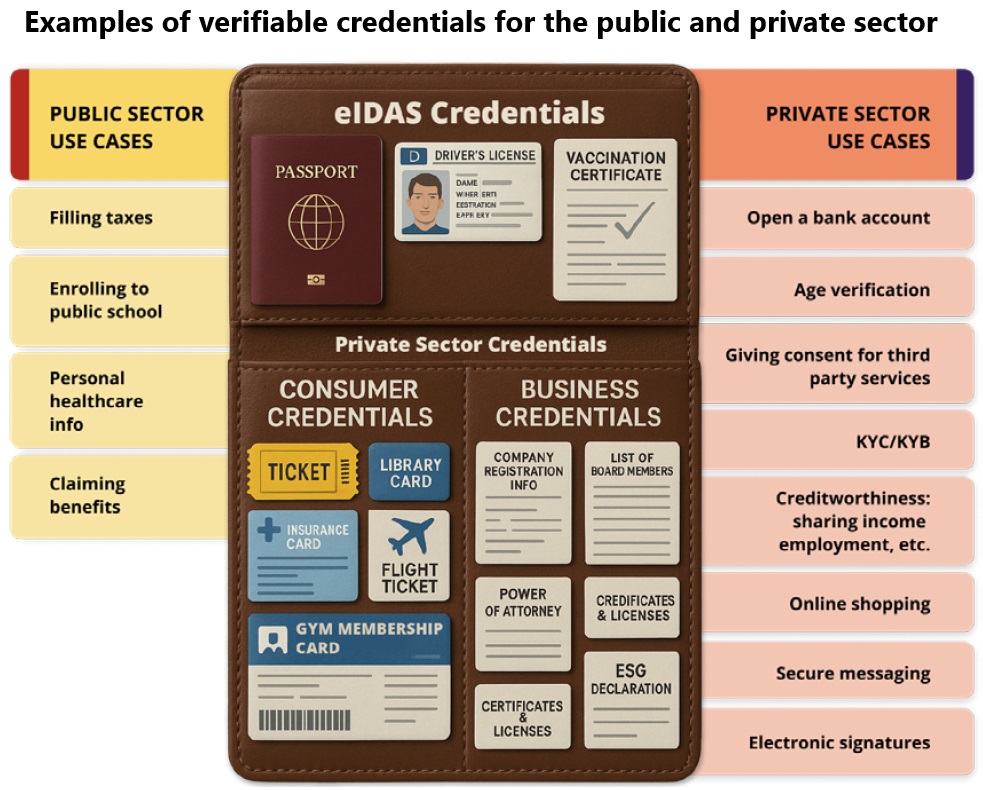

By issuing credentials—such as proof of income, KYC data, or creditworthiness—banks can monetise existing verified data, streamline customer onboarding, and open new revenue streams.

Initiatives like Bizum in Spain, a bank-owned wallet with over 29 million users, illustrate the potential to leapfrog traditional government-led models and deliver user-centric identity solutions.

In more digitally mature markets such as the Nordics and Estonia, the low-hanging fruit has already been harvested.

Here, banks must look beyond basic efficiencies and explore advanced applications: cross-border onboarding, reusable compliance credentials, and verifiable digital proofs for corporate entities.

Rather than replicating existing infrastructure, these banks are urged to explore new trust-based services and experiment with how digital credentials can replace cumbersome legacy processes.

Roles Banks Can Play

The Mobey Forum identifies four potential roles for banks within the EUDIW ecosystem:

-

Wallet Issuer – The most transformative but resource-intensive role. Banks could own the digital interface through which users manage their identities. However, national regulations and the requirement for Qualified Trust Service Provider (QTSP) certification limit this option’s accessibility.

-

Credential Issuer – Leveraging verified customer data to issue digital attestations, banks could underpin ecosystems of trust while generating revenue and enhancing customer stickiness.

-

Relying Party – The baseline regulatory requirement. By accepting and processing EUDIW credentials, banks can reduce fraud, automate onboarding, and improve customer authentication.

-

Access Provider – A pragmatic alternative that allows banks to embed EUDIW features into their apps without issuing credentials themselves, thus maintaining relevance without regulatory burden.

This flexibility allows banks to tailor their approach based on capability, ambition, and market conditions. Yet the report is clear: merely doing the minimum will not suffice in the long term.

A Shift in Strategic Mindset

Critically, the business case for EUDIW cannot be measured solely by immediate return on investment.

Like the early days of internet banking, its full value will accrue over time.

The EUDIW enables banks to participate in an entirely new ecosystem of high-assurance digital interactions – think e-signatures, verified document sharing, or secure messaging.

Banks that lean in early will be better positioned to shape emerging standards and customer expectations.

They will also be able to pre-empt competition from non-bank actors, who may lack the same trust capital but are often quicker to innovate.

Yet challenges remain.

Becoming a QTSP involves significant compliance costs and operational complexity.

Moreover, in markets like Austria, where government-led wallets are highly advanced, the space for banks to offer alternative solutions is limited.

Political and cultural resistance to digital identity also hampers adoption in some member states.

Preparing for the Digital Identity Economy

The broader strategic question is not whether banks should engage with the EUDIW – it’s how.

Institutions must now assess their digital maturity, regulatory posture, and long-term ambitions.

Embedding identity services into banking apps, partnering with certified issuers, or leading innovation in digital credentials all offer pathways forward.

As Elina Mattila of the Mobey Forum rightly states, “Banks should think beyond today’s processes and imagine new value propositions for the digital future.”

The arrival of the EUDIW is not merely a regulatory hurdle but a historic opportunity to reimagine banking at the intersection of identity, trust, and data.

Comments