trending

trending

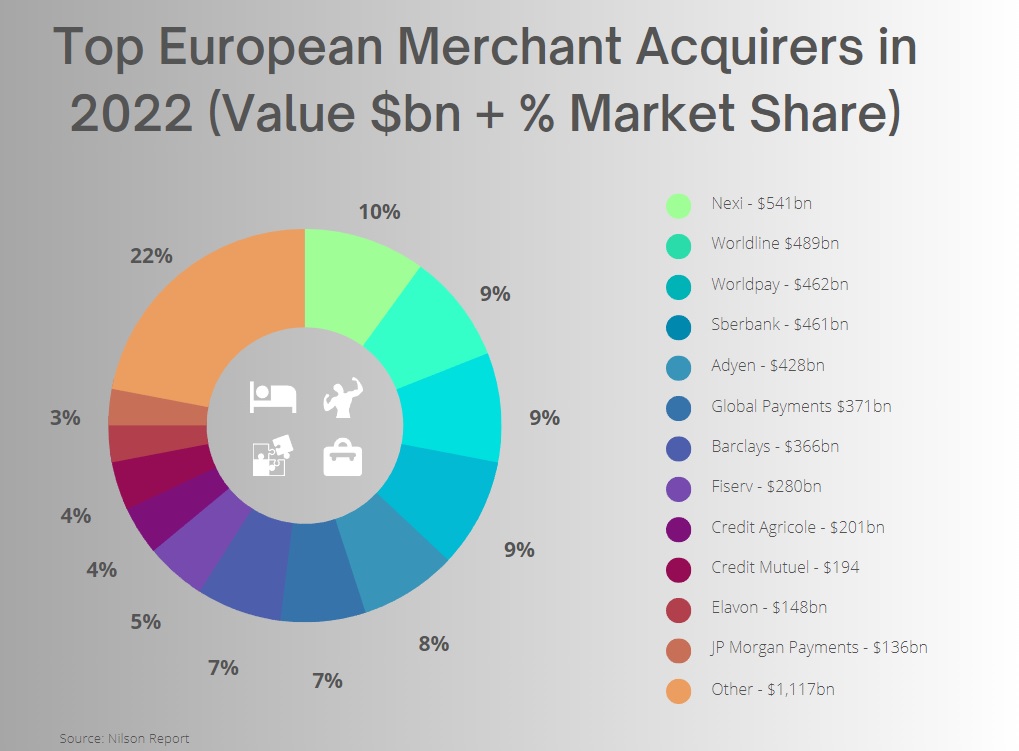

Jeffries recently made a deep-dive analysis of the Nilson Report’s annual Top Merchant Acquiring ranking to compare top players, annual changes and track evolution of payments companies vs. banks.

Post several intensive years of consolidation, Nexi and Worldline ranked again at the top, while Adyen, 5th, surpassed Barclays, at 7th, and Worldline’s future JV partner Credit Agricole came in 9th.

Nexi remains top European Merchant Acquirer

Nexi remains the largest European merchant acquirer with $541 billion TPV (-20% y/y).

Worldline came in 2nd ($489 billion/+10%), which was equally balanced between in-store and online channels. Worldline is the largest in-store acquirer.

Adyen grew 60% y/y to $428 billion surpassing Barclays to become 5th largest acquirer in Europe driven by nearly threefold increase in in-store, which ranks now 9th, while Adyen‘s European e-commerce acquiring at $284 billion (1st in Europe) is now 35% larger than #2 Worldpay.

Total Merchant Acquiring Value reached $5.2bn in 2022

In aggregate, the top 50 European Merchant Acquirers grew 6% y/y to $5.2 trillion, below 3-year CAGR of 12% and long-term growth of 9%pa. Total Value was driven by a 15% volume increase, offset by a $2 decline in average basket size.

In-store outpaced e-commerce for first time ever

As the post pandemic normalisation continues in 2022, in-store TPV (+7%) outstripping e-commerce growth (+3%) for first time since the data was tracked (2014).

In-store reached $3.7 trillion vs. e-commerce of $1.5 billion, or 29% of total. Despite a rebound in travel/hospitality average basket size across both channels declined by $2 to $27 and $48, respectively.

Payments companies outgrew Banks

Payments companies grew 9% y/y to $2.7 trillion making up now 52% of total, but well below 3-year CAGR of 23%, but close to long-term growth of 11% pa.

Banks grew 3% y/y to $2.5 trillion in-line with their 3-year CAGR of +3%, but well below long-term growth of 7% pa.

Conclusion for European Payments

After years of active consolidation, Worldline and Nexi have solidified their position at the top of the European Merchant Acquiring market, however, Adyen’s organic rise likely continuous, albeit likely on a slower pace as underlying e-commerce growth has slowed, while switching in in-store typically slower ramps.

Despite higher market concentration, we believe the market will remain competitive given latest/pending owner changes: US Shift4’s acquisition of Finaro, Israeli Rapyd’s takeover of Valitor and FIS’ spinoff of Worldpay.

Conclusion for European Banks

Barclays and Credit Agricole are now the only two European banks in the top 10 merchant acquirers by value.

On Barclays, we note that it holds one of the top 3 market share positions in European web-based payments, despite a decline in transaction value growth (Barclays looks underweight share on in-store).

Various media sources have suggested that Barclays may be looking to somehow monetise its payments business and one area it could look specifically is at the UK acquiring arena.

Comments