trending

trending

As banks struggle to make a profit and the ESG trend fades quicker than a fake sun-tan, James Wood asks whether sustainability still matters in payments.

Despite all the negative publicity banks get, there’s an argument we should have more sympathy for them.

For more than a decade since the Great Financial Crash of 2007, according to McKinsey and Co, bank profitability has either flatlined or declined.

Meanwhile, competition from Big Tech players such as Google and Apple, or insurgent start-ups like Klarna, has shot up.

And all this at a time when banks say – perhaps with more than a grain of truth – that they are subject to far more regulatory scrutiny than those firms looking to steal their market share.

“The tough times in retail banking are far from finished.”

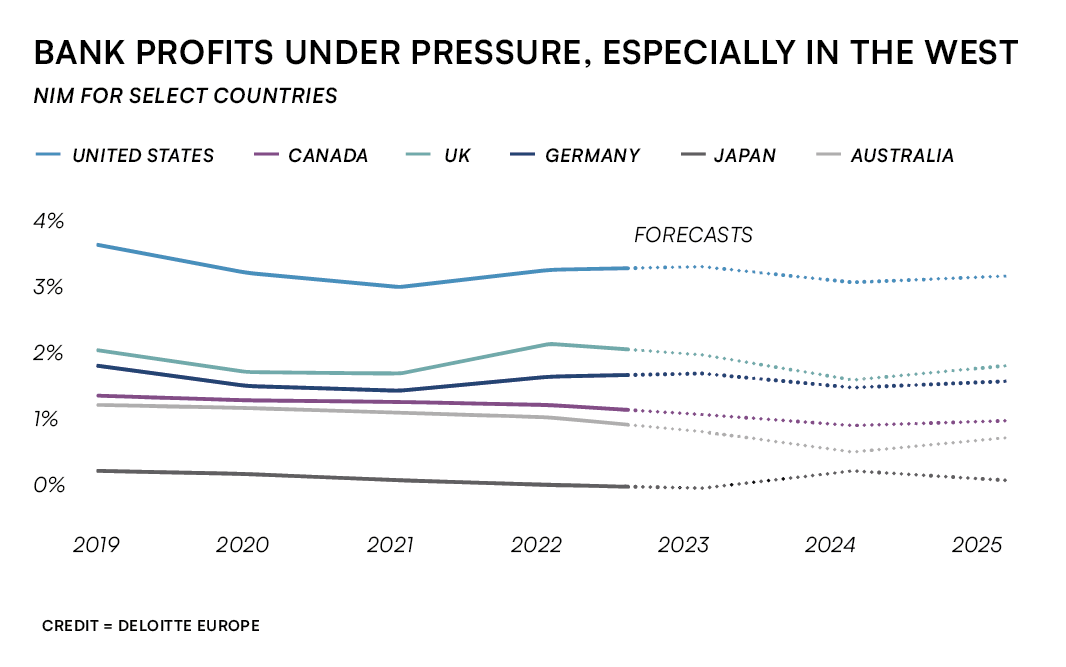

There’s little sign of any comfort to come, either, with Deloitte – among others – predicting an outlook of slow and moderating growth over the next few years.

Deloitte say bank net interest margins in major economies – the money banks make from lending money after costs – is set to decline.

While it’s not all bad news, as Deloitte sees fee income for banks world-wide increasing, there’s no doubt the tough times in retail banking are far from over.

The party’s over …

Back in what now look like the good old days of the naughties, banks were keen to parade their virtue and explain how they were cutting their carbon footprint, reducing waste and energy usage, and contributing to society.

Thus the Environmental, Social and Governance (ESG) movement was born, a movement that culminated for some observers in the bizarre spectacle of the CEO of a tobacco company stating they wanted to see a smoke-free world, or in UK banks allegedly making decisions about consumers’ rights to hold accounts based on their political beliefs.

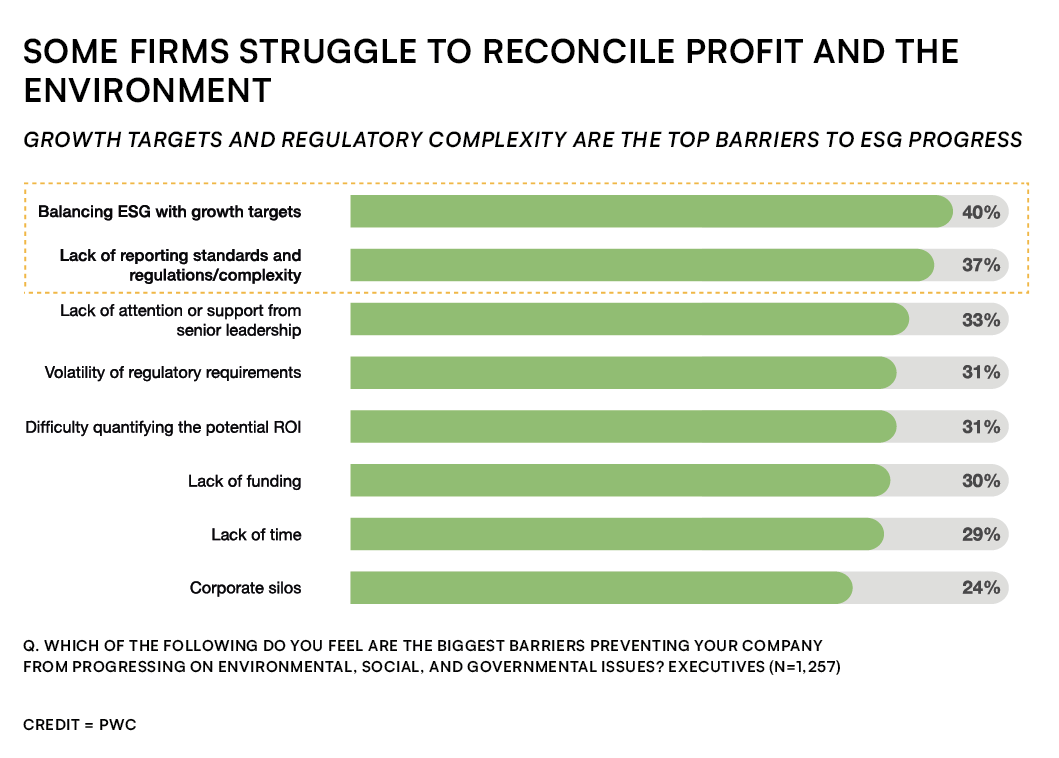

“While more than 75% of consumers say environmental concerns are vital, 40% of firms struggle to reconcile the drive for profit with sustainability.”

It would be an understatement to say there’s now some scepticism around the ESG movement, chiefly from media commentators who believe it’s gone too far – and from companies who say they’re struggling to reconcile their commitment to ESG goals with greater profitability.

According to last year’s ESG Consumer Intelligence study from PwC, more than three-quarters of consumers (76%) expect companies to take action on ESG goals.

At the same time – and while recognising the importance of the environment – 40% of global business leaders say they’re struggling to reconcile demands for greater sustainability with the search for improved profitability.

As the graph above shows, regulation in its various forms – both as a shifting target, and as an ever-increasing burden – is as much of a barrier to sustainability success for companies as the perceived cost of focusing on sustainability.

Although Western governments appear to have relaxed their focus on the decarbonisation agenda in favour of greater economic growth, pressure on companies to act remains intense.

… or has it only just started?

All of that said, the biggest argument in favour of a continued or indeed increased focus on sustainability is consumer demand.

A wide range of studies show that sustainability is a great thing for customer loyalty: a recent study from the Harvard Business Review revealed 65% of consumers are actively seeking out brands driven by the sustainability agenda, while in October 2020 Nielsen Research claimed 81% of the world’s consumers expect companies to take action to save the planet.

The paradox of sustainability in payments is that while consumers say they want sustainable payments, they tend to prefer payment methods that have not, historically speaking, aligned with the Earth’s interests.

For instance, seven in ten consumers still prefer to pay with plastic cards or cash and there are ten billion plastic cards out there at present, most of which were made from virgin plastics and include resource-intensive computerised chips.

Simple, concrete steps for sustainable profit

Plastic cards represent a huge opportunity to improve sustainability.

Making use of sustainable raw materials – such as ocean recovered plastic, recycled PVC, recycled PETg and PLA or even sustainable wooden cards is a first and important step to improving your environmental profile.

Hans Sjölund, Head of Sales & Business Development, Cards at leading financial software and card systems provider Tietoevry Banking, says: “We continue to see growing demand for sustainable card products from our client banks. At present, around 75% of our total card production uses sustainable materials, and we expect this figure to continue to grow in the years ahead.”

Other methods that help to improve sustainability and drive better profits include reducing the use of paper in customer communications, especially for account management, card activation and dispute resolution, while the use of sustainable energy in card production and operations management is also important.

Looking ahead, determining how your card products are disposed of and in particular how the rare-earth metals used in chip production are recycled is likely to become a significant marker of sustainability in the future, given the cost of extracting and treating these metals.

Perhaps the final word on sustainability for now should be a note of caution. As we explain in our article on “phygital” payments in this issue, the physical side of payment experiences is not going to go away and no bank should assume that their customers will be paying solely with digital devices or via app.

Investing in sustainable card and payment solutions can involve technology but, as we’re seeing in so many areas of human life at the moment, technology is not in and of itself the answer to the problem of sustainability.

Comments