trending

trending

Momentum around central bank digital currency development is building steadily, according to a Digital Monetary Institute (DMI) survey.

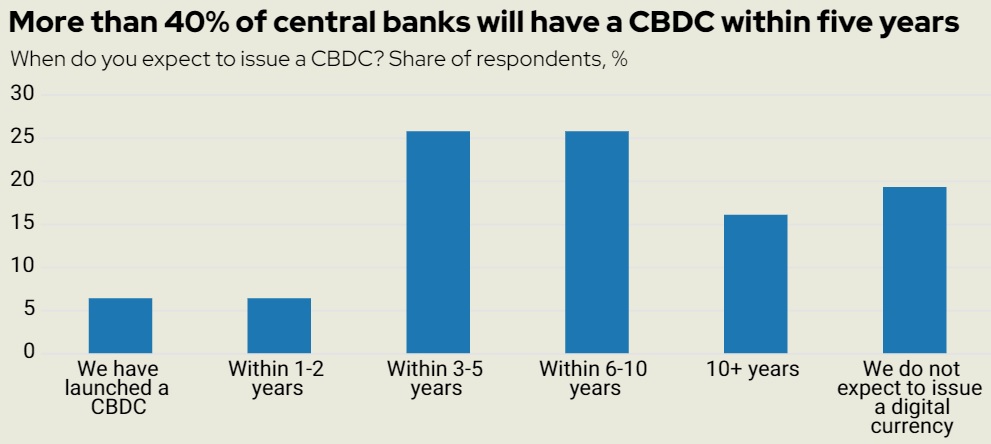

Of the central banks that responded to a new survey, 41% expect to have launched a CBDC within five years. In last year’s survey, this figure was 36%.

The proportion of central banks who do not expect to launch a digital currency has fallen from 35% in 2022 to 19% this year.

Adoption is the single biggest concern for central banks looking to launch a CBDC.

That concern is much more pronounced in developed markets, with some 67% of respondents picking it as their main concern, compared to 37% of emerging market respondents.

However, only 18% of central banks said they are working with marketing and promotional advisers, with another 3% saying that they intend to do so in the future.

Central banks know they need help with some aspects of CBDC design. Many have already looked for help in areas like privacy and user experience.

But for other topics, including interoperability, offline payments and cross-border connectivity, more are still intending to enlist third-party assistance. Offline payments, in particular, is proving to be the most challenging aspect of CBDC design to deliver.

The official sector has made it a priority to improve the cross-border payments market.

Transaction costs and processing costs are tied as central banks’ primary focus for improvement in our survey. Interoperability and regulatory compliance are next on their lists to address.

While 47% of central banks favour interlinking fast payment systems, 31% believe that connecting CBDCs offers the most promising means of improving cross-border payments.

This is an interesting result, given that only 3% said improving cross-border payments efficiency was the main motivation for pursuing CBDCs.

This suggests that, while they see the promise in interlinking CBDCs, they need a domestic rationale to justify issuing one since it relies on international collaboration.

Collaboration between central banks to connect CBDC networks is underway in some areas, but the projects have not yet won the confidence of the majority of central banks surveyed.

Common platform projects like mBridge and hub-and-spoke projects like Icebreaker are advancing but, for the moment, compatibility is the model that central banks favour for interconnecting CBDCs.

These multi-currency CBDC projects are an example of a broader trend towards a regional focus in payments.

These regional systems need only a few countries with trading relationships to build consensus on standards and can offer valuable operational efficiency savings for participants.

While the dollar is on one side of 90% of global foreign exchange transactions and its status as the world’s reserve currency is not under threat any time soon, 17% of central banks surveyed said that they were actively trying to reduce their reliance on the currency.

While some $11 trillion was transacted in stablecoins in 2022, the survey indicates that central banks are not yet convinced, with no central banks selecting stablecoins or cryptocurrencies as a promising means of improving cross-border payments.

Despite some momentum in private sector payments, 66% of central bank respondents also said they are unsure that blockchain will play a role in the future of payments.

Appetite for CBDCs is strong

Appetite for CBDCs is strong among respondents to the survey. While only 7% have a CBDC already, a further 7% expect to have one within the next two years.

A further 27% will launch a CBDC in three to five years, meaning more than 40% expect to have an operational digital currency by 2028.

Within a decade, close to 70% of respondents will have a CBDC. Only 17% of respondents currently rule out a future digital currency, and a number of these respondents are continuing to research the feasibility of introducing one.

While there may be some positive bias in the central banks that took part in the survey, these findings suggest that central banks are confident they can overcome many of the challenges that creating a CBDC entails.

Positive sentiment towards the concept of CBDCs is growing. Some 30% of respondents said they have become more inclined to issue a CBDC over the past 12 months.

This suggests that the exploratory work and feasibility studies that many respondents said were in progress are producing promising results.

Comments