trending

trending

Cross-border payments, once a byword for inefficiency and opacity, are undergoing a structural transformation.

The convergence of regulatory momentum, technological innovation, and geopolitical necessity is creating a watershed moment for global money movement.

From the G20’s roadmap and ISO 20022 migration to central bank experiments and stablecoin adoption, the building blocks of a faster, cheaper, and more transparent global payments system are being laid down at scale.

The G20 Roadmap: Setting the Strategic Compass

In November 2020, the G20 – a coalition of the world’s largest economies – launched a roadmap to enhance international retail, wholesale, and remittance transactions. By 2021, the Financial Stability Board (FSB) had articulated concrete targets across four pillars: cost, speed, access, and transparency. These targets, aimed for completion by 2027, are not legally binding, but their influence is unmistakable.

To deliver against these objectives, financial institutions (FIs) are being encouraged to upgrade legacy infrastructure, adopt ISO 20022 standards, and ensure seamless interoperability across jurisdictions. As geopolitical tensions fragment global supply chains and expose the vulnerabilities of legacy systems, the case for reform has never been more urgent.

“Institutions cannot hope to satisfy the G20’s targets without modernising the systems underpinning cross-border payments,” says one senior executive from a global bank. “This includes removing silos with APIs, automating reconciliations, and settling disputes digitally.”

ISO 20022: A New Global Payments Language

The centrepiece of infrastructure reform is ISO 20022 – a harmonised data messaging standard that promises greater richness, structure, and granularity. The deadline for migrating cross-border payments to ISO 20022 CBPR+ is November 2025. After this point, MT messages – the legacy SWIFT format – may no longer be processed.

Transitioning to ISO 20022 is more than a compliance task; it represents a foundational step towards achieving real-time payments, full data transparency, and operational resilience.

As SWIFT’s Shirish Wadivkar explains: “It’s not only a great example of how the ISO 20022 standard can help our industry deliver better user experiences, but also a case in point for how SWIFT is committed to interoperating an increasingly complex financial ecosystem.”

Case in point: SWIFT’s new Case Management solution, which uses ISO 20022 data and unique end-to-end transaction references (UETR), has shown the potential to reduce investigation times by up to 80% and cut costs by more than $600 million annually.

Nexus: A Multilateral Leap Forward

While ISO 20022 establishes a common language, the Bank for International Settlements (BIS) has been spearheading efforts to interconnect payment systems themselves. Project Nexus – a collaboration between the BIS and the central banks of Indonesia, Malaysia, the Philippines, Singapore, and Thailand – is a bold attempt to link real-time domestic payment systems via a single connection.

A technical network operator is now being sought to run Nexus, which will be governed by Nexus Global Payments (NGP), a Singapore-based entity formed by the participating central banks. Live implementation is imminent.

As a model, Nexus demonstrates that interoperability doesn’t necessarily require every country to build bilateral links. Instead, a single multilateral network – aligned on ISO 20022 and supported by purpose-built APIs – can act as a hub, connecting jurisdictions in a scalable fashion.

The Stablecoin Surge

But even as policymakers focus on regulated payment rails, the private sector is accelerating cross-border innovation through blockchain and digital assets – particularly stablecoins. These fiat-pegged cryptocurrencies, like USDT (Tether) and USDC (Circle), offer near-instant settlement, dramatically lower costs, and greater transparency.

FV Bank, a regulated US financial institution, recently began supporting direct USDT deposits to simplify international transfers.

“This innovation positions us at the forefront of regulated financial institutions offering stablecoin on-ramps and off-ramps,” said CEO Miles Paschini. “We’ve also seamlessly integrated blockchain analytics tools to pre-screen and detect transactions linked to AML activity.”

The stablecoin value proposition is compelling: no pre-funded accounts, 24/7 availability, and up to 80% lower transaction fees.

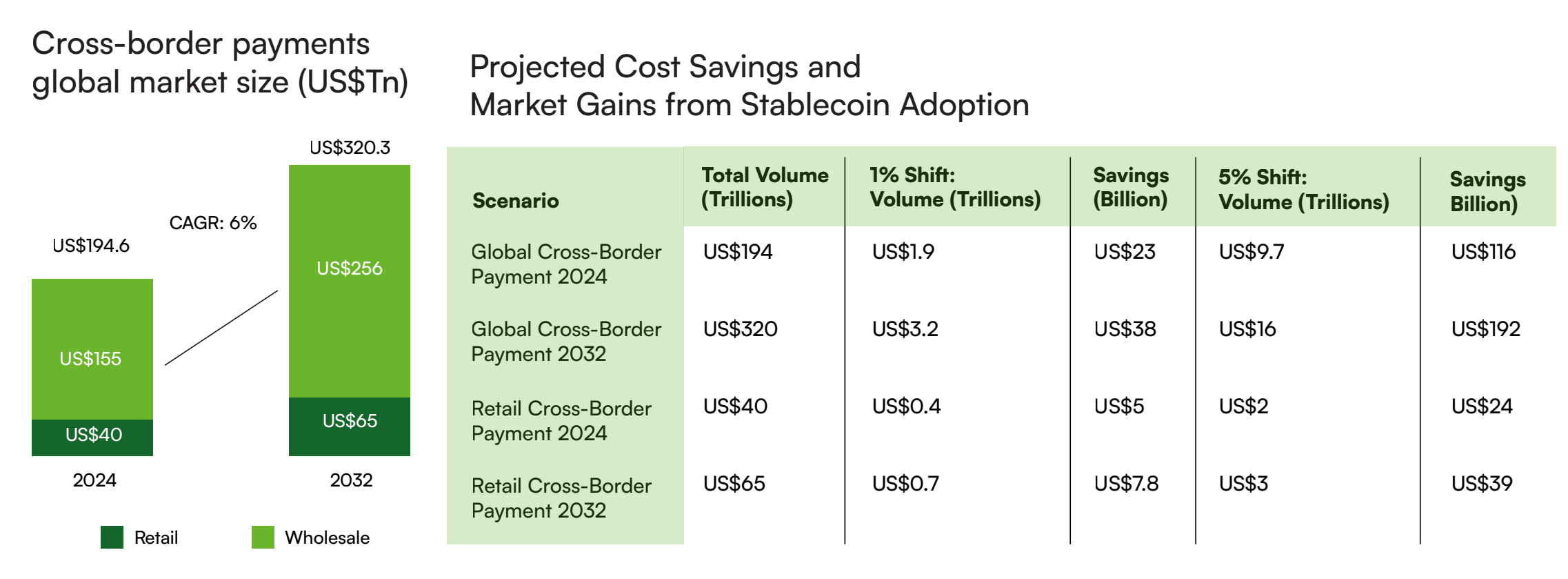

According to industry data, stablecoin transaction volumes hit $625 billion in February 2025, a 21% year-on-year increase. Over the 12 months to February, $6.3 trillion in stablecoins were transacted – equivalent to 15% of global retail cross-border payments.

Regulatory Clarity: The Catalyst for Adoption

For traditional banks, the largest barrier to stablecoin adoption has not been technological – but regulatory. “If they make that legal, we will go into that business,” said Brian Moynihan, CEO of Bank of America, earlier this year. “It’s pretty clear there’s going to be a stablecoin, fully dollar-backed (…) like another foreign currency.”

That regulatory clarity is now materialising. In the EU, the Markets in Crypto-Assets (MiCA) framework has established a baseline for stablecoin issuance and custody. The UK is preparing new rules, and in the US, legislative proposals like the STABLE and GENIUS Acts are under active debate. In Asia, Singapore, Japan, and Hong Kong are leading the way with clear, enforceable standards.

As clarity increases, so will institutional confidence. Gabriele Zuliani, Chief Revenue Officer at Bitso Business, notes: “Once regulatory clarity is achieved, we expect financial institutions to adopt stablecoins more widely, eliminating intermediaries and revolutionising cross-border payments.”

Disruption at Scale

Stablecoin integration is poised to reconfigure cross-border payments in three stages: operational transition, market disruption, and early-adopter advantage.

In the first phase, banks will collaborate with stablecoin issuers and blockchain providers to pilot B2B and retail cross-border flows. Intra-group transfers, invoice payments, and e-commerce settlements are low-hanging fruit, offering instant liquidity and reduced costs.

Then comes market disruption. Banks will need to rethink fee structures, overhaul legacy systems, recruit blockchain talent, and launch programmable payment products. Those slow to adapt risk disintermediation.

Finally, early adopters will secure a competitive edge. They’ll gain liquidity, attract digitally native clients, and unlock new revenue streams – from stablecoin custody to DeFi-linked products.

The potential benefits are staggering. A 5% shift from traditional to stablecoin-powered cross-border payments could save $116 billion in fees annually and unlock $500 billion in trapped capital. Stablecoins may yet become the eurodollars of the digital age.

Towards a New Global Standard

The shift towards faster, cheaper, and more transparent cross-border payments is not theoretical. It is happening now – propelled by regulatory intent, private sector dynamism, and a shared urgency to modernise the financial plumbing of global trade.

Yet, while technology is the enabler, collaboration is the accelerant. FIs must engage with public stakeholders on legal harmonisation, partner with fintechs on technical integration, and educate clients on new services and safeguards.

Ultimately, this is about more than meeting the G20’s targets. It is about redefining what is possible in global finance – from real-time micro-remittances to 24/7 e-commerce settlements, and from reduced friction to repurposed capital.

As Isabel Schmidt of BNY rightly puts it: “We understand how critical real-time transparency is for our clients during payment investigations (…) improving overall client satisfaction and increasing the value we bring as a solution provider.”

With ISO 20022 taking hold, Nexus going live, and stablecoins poised to go mainstream, the transformation of cross-border payments is not on the horizon. It is already underway.

Comments