trending

trending

In the midst of continued financial strain across US households and many other major markets, a new study sheds light on the value consumers place on convenience services – and the trade-offs they are willing to make to buy themselves time.

The report, How Do Consumers Weigh Convenience Services Against Financial Pressure? It’s About Buying Time, based on a survey of nearly 2,900 US consumers in January 2025, reveals that affordability remains the principal barrier to wider adoption of convenience services, far outstripping concerns over service quality.

While these services – ranging from grocery and restaurant delivery to home maintenance and personal care – are positioned as time-savers, they come with an unavoidable financial cost that is becoming harder to justify in an uncertain economic environment.

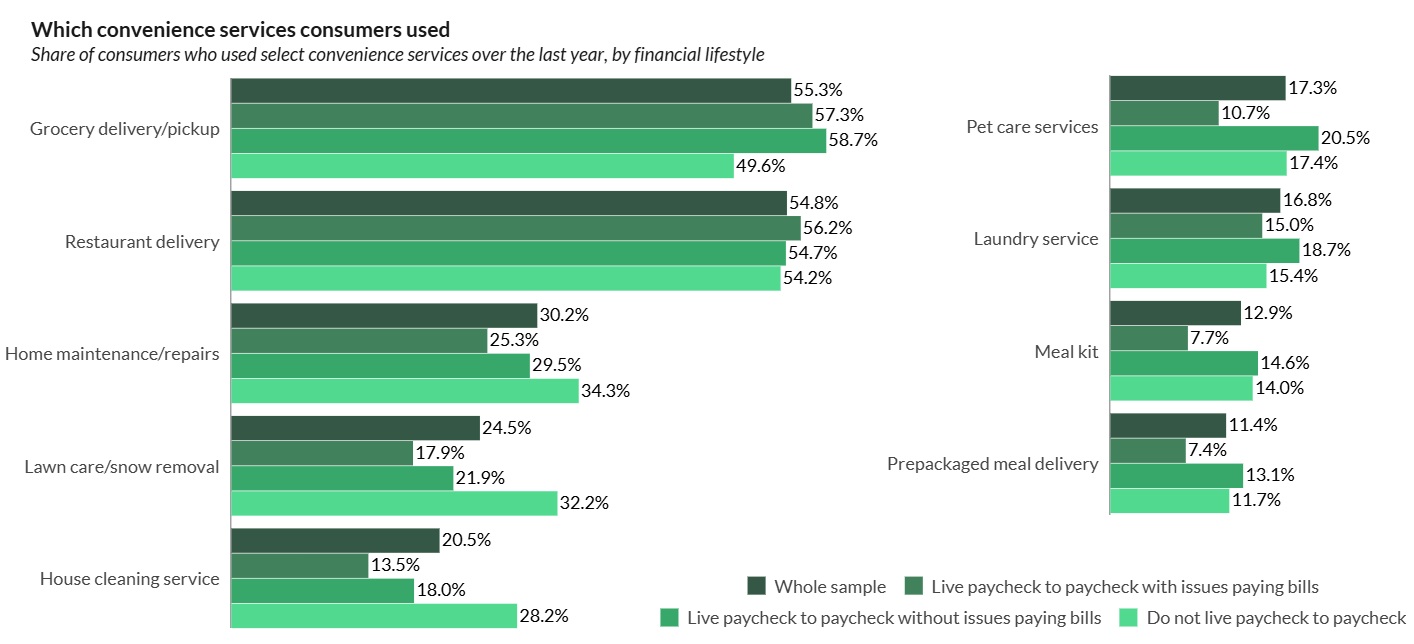

Convenience Services

The research found that urban consumers are the most frequent users of convenience services, with 79% having used them in the past year and spending an average of $234 monthly.

In contrast, only 51% of rural consumers reported using these services, spending $186 per month on average.

Income is also a determinant: 75% of high-income consumers use convenience services, compared with just 59% of low-income consumers.

Interestingly, extensive spending on such services appears to contribute to why some higher-income consumers continue to live paycheck to paycheck.

They are effectively prioritising time savings over financial liquidity.

As of January, 67% of US consumers were living paycheck to paycheck, up from 65% in December, underlining the pervasive nature of financial constraints in shaping discretionary spending decisions.

Value of Convenience

Affordability clearly dominates consumer concerns, with 51% of respondents citing lower prices as the key factor that would drive greater use of convenience services – more than double the proportion who prioritise improved service quality.

This indicates that consumers recognise the value of convenience but often find the financial trade-off prohibitive.

Moreover, the data reveals that consumers not living paycheck to paycheck are significantly more likely to use home maintenance (34%), lawn care (32%), and house cleaning (28%) services than those with bill-paying difficulties, whose usage stands at 25%, 18%, and 14% respectively.

This demonstrates how financial stability facilitates the adoption of higher-cost, non-essential convenience services.

For merchants and service providers, the findings present a clear strategic implication: pricing innovation, rather than service enhancement, is key to driving uptake.

Subscription models, targeted discounts, and flexible payment options could prove far more effective than incremental improvements in service quality.

Ultimately, the study underscores that while convenience services are valued for their time-saving benefits, cost remains the defining factor in adoption.

Providers seeking growth in this sector must align pricing strategies with consumers’ financial realities to unlock broader market penetration.

Comments