trending

trending

As we write about Elon Musk’s plans for X and the future of Open Banking in Europe, news reaches Payments Cards & Mobile of an alternative to either the social media giants or platformed financial services.

And this alternative could come from those very players most under threat from tech giants – traditional high-street banks.

“Banks are up to four times more trusted than tech firms when it comes to payments.”

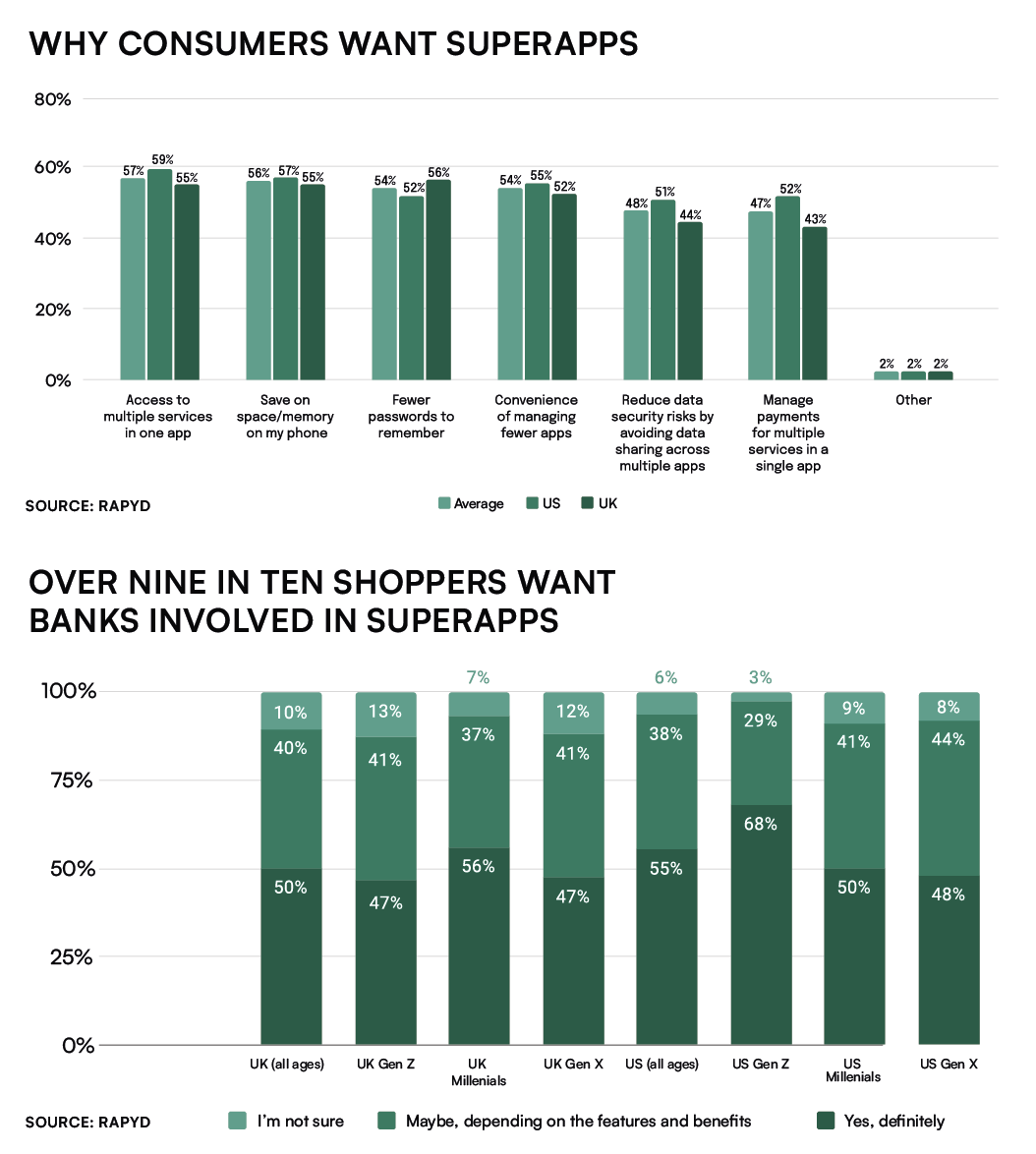

New rese arch from Rapyd into consumer preferences in the UK and US suggests almost nine in ten consumers would welcome the opportunity to organise their financial lives through a Super App which offered a full range of financial services in one location.

arch from Rapyd into consumer preferences in the UK and US suggests almost nine in ten consumers would welcome the opportunity to organise their financial lives through a Super App which offered a full range of financial services in one location.

Given the success of Super Apps in China and elsewhere, this is hardly surprising: what’s more interesting is where they see this kind of app coming from.

Consumers would welcome a Super App for the ability to access multiple services in one place and cut down on the number of passwords required.

They also recognise the importance of reducing data security risk through fewer apps, and the capacity to execute multiple functions in one place.

While bank clients see tech companies such as Apple and Amazon leading the development of Super Apps – tellingly, both Meta and Twitter are far off the pace in consumer’s minds – more than nine in ten would feel more comfortable if their high-street bank were a partner in the app.

Jeremy Baber, CEO of Lanistar, told Payments Cards & Mobile in an interview that, “Europe is behind in the SuperApp race. We have seen some household names begin to explore the possibility of diversifying their apps, such as Uber, Klarna and Lydia, but have much further to go to reach Super App status.”

Rapyd’s research says UK consumers are three to four times more likely to trust their bank when compared to a social media or technology company, and that their key concerns are data security, privacy and reliability of the app’s services.

While these concerns are shared by US consumers, younger age groups are much less likely to trust their banks, with only Gen X’ers (43-54) and Millennials placing significant faith in their bank to deliver.

Payments Cards & Mobile View

Given stuttering progress towards Open Banking in Europe and its stagnation in the US, plus the regulatory headwinds faced by tech companies, Rapyd’s research offers an interesting perspective on where the future might lie – a wider range of financial services delivered by banks through their apps.

So far, banks have been disappointingly slow to introduce new app-based services, but the arrival of account-to-account payments, credit scoring and request-to-pay systems could herald a new as they fight back against the tech giants.

Their “ace in the hole” in this fight is the trust they continue to hold at a level most tech companies can only dream of.

Comments