trending

trending

Digital money is moving through one of its most decisive transitions since the dawn of online banking.

Stablecoins may have captured the early imagination—fuelled by crypto markets, cross-border commerce, and the search for dollar liquidity—but a different type of digital asset is now emerging from the banking sector’s shadow.

Tokenised deposits, or “bank tokens”, could become the dominant institutional format of on-chain money by the end of the decade.

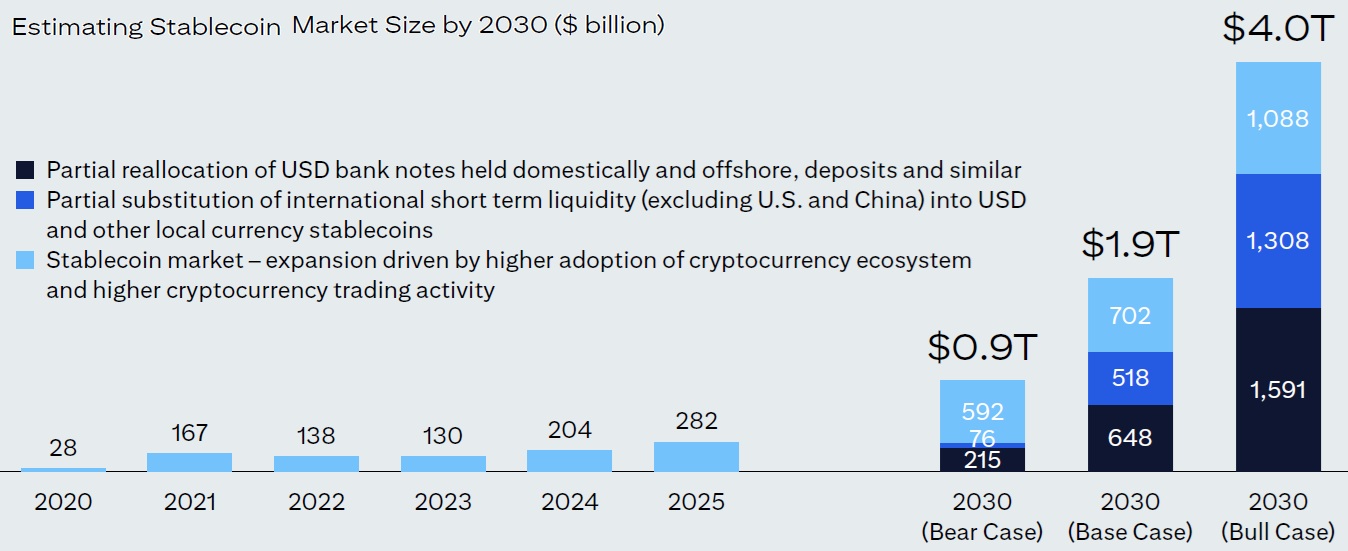

According to Citi Institute’s latest research, tokenised deposits could support $100–140 trillion in annual transaction flows by 2030—volumes that rival, and in some cases exceed, those projected for stablecoins.

While stablecoins may still reach up to $4 trillion in circulation under bullish assumptions, their velocity-driven transaction volumes are predicted to peak near $200 trillion.

Bank tokens are therefore not a niche experiment; they are a structural evolution of money itself.

Why the Future May Favour Bank-Based Digital Money

The argument begins with trust.

Stablecoins promise speed and global reach, but their foundations rest on the credibility of private issuers.

Reserve quality, redemption windows, and the composition of backing assets have all been flashpoints. Even today, heightened regulatory scrutiny reflects lingering concerns over transparency and risk management.

Bank tokens operate at a different end of the trust spectrum.

They represent insured deposits issued by regulated banks, embedded in long-standing capital, liquidity, and supervisory frameworks.

For corporate treasurers—whose priorities are counterparty safety, accounting clarity, and operational continuity—these features provide reassurance that stablecoins cannot easily replicate.

Crucially, tokenised deposits also circumvent many of the frictions created by existing crypto rails.

They do not require separate on- and off-ramps, nor do they force enterprises to reconcile on-chain activity with off-chain bank balances.

Instead, bank tokens fit directly into established treasury and ERP systems, allowing businesses to automate settlement, liquidity management, and cash positioning within familiar infrastructures.

Privacy and Compliance: Built into the Architecture

Corporates rarely want their trading terms, supplier payments, or payroll activity visible on public blockchains. Stablecoins, operating on open networks, face an inherent tension between transparency and confidentiality.

Bank tokens, typically implemented on private or permissioned networks, resolve that tension by design. They enable programmable automation with embedded compliance, while keeping sensitive data shielded from public view.

Regulators, meanwhile, retain controlled auditability—an equilibrium that holds strong appeal for institutions subject to stringent reporting and risk-governance requirements.

Scale, Interoperability and the Network Effect

Banks already move trillions daily. If just five percent of large-value payment flows migrate to tokenised rails, the resulting volumes would eclipse the current stablecoin market.

More importantly, banks are designing these systems to be interoperable: multi-bank, multi-asset, cross-border. Clients do not want digital silos—they want an on-chain ecosystem that mirrors the universality of existing payments infrastructure.

The implications are profound.

Tokenised deposits could power everything from automated trade finance to real-time treasury sweeps and settlement of tokenised securities, while stablecoins continue to serve crypto markets, cross-border e-commerce, and emerging-market users seeking dollar stability.

A Plural Future for On-Chain Money

The next decade is unlikely to crown a single winner.

Citi’s analysis frames a world in which stablecoins and bank tokens are complementary rather than competitive.

Stablecoins will thrive where openness and global reach matter most; bank tokens will dominate where regulatory certainty, privacy, and institutional scale are essential.

Together, they are laying the foundations of what Citi calls the “broadband era” of blockchain finance—where speed, programmability, and interoperability become core features of global liquidity networks.

For corporates and financial institutions, the coming shift will not be about replacing banks, but about re-engineering money itself for a programmable, always-on world.

Comments