trending

trending

The global monetary system is undergoing its sharpest reconfiguration in decades.

Push away from cash toward digital currencies

New research from the Venom Foundation argues that physical cash is entering its final phase, with Asia and the Middle East and North Africa (MENA) driving an accelerated shift to state-backed digital currencies and regulated stablecoins.

The study positions the next 36 months as a decisive window during which national payment systems, cross-border settlement rails and even the geopolitical balance around the US dollar are likely to be reshaped.

At the centre of this shift is the sheer breadth of global engagement.

A total of 137 countries—covering 98% of world GDP—are now developing or trialling central bank digital currencies (CBDCs). Several of the most ambitious launches are scheduled between 2025 and 2028, a period the report suggests will mark the effective end of widespread cash usage in major economies.

Asia and MENA Take the Lead

While CBDC work is under way globally, it is Asia and MENA that are setting the pace through a combination of regulatory clarity, infrastructure investment and political will.

China continues to operate the world’s largest CBDC experiment, with the digital yuan having processed nearly $1 trillion in transactions.

India’s digital rupee is expanding rapidly—circulation grew 334% in the past year—supported by the country’s vast UPI real-time payments network.

The UAE will launch its retail Digital Dirham in late 2025, part of a broader digital finance overhaul, and Saudi Arabia has formally joined Project mBridge, the multi-CBDC platform linking Asia and the Gulf.

These countries are strengthening their domestic foundations while simultaneously building new cross-border corridors.

mBridge’s arrival at minimum viable product stage in 2024 marked a turning point: transactions now settle in seconds, bypassing correspondent banks and avoiding the $120 billion in annual costs associated with the current model.

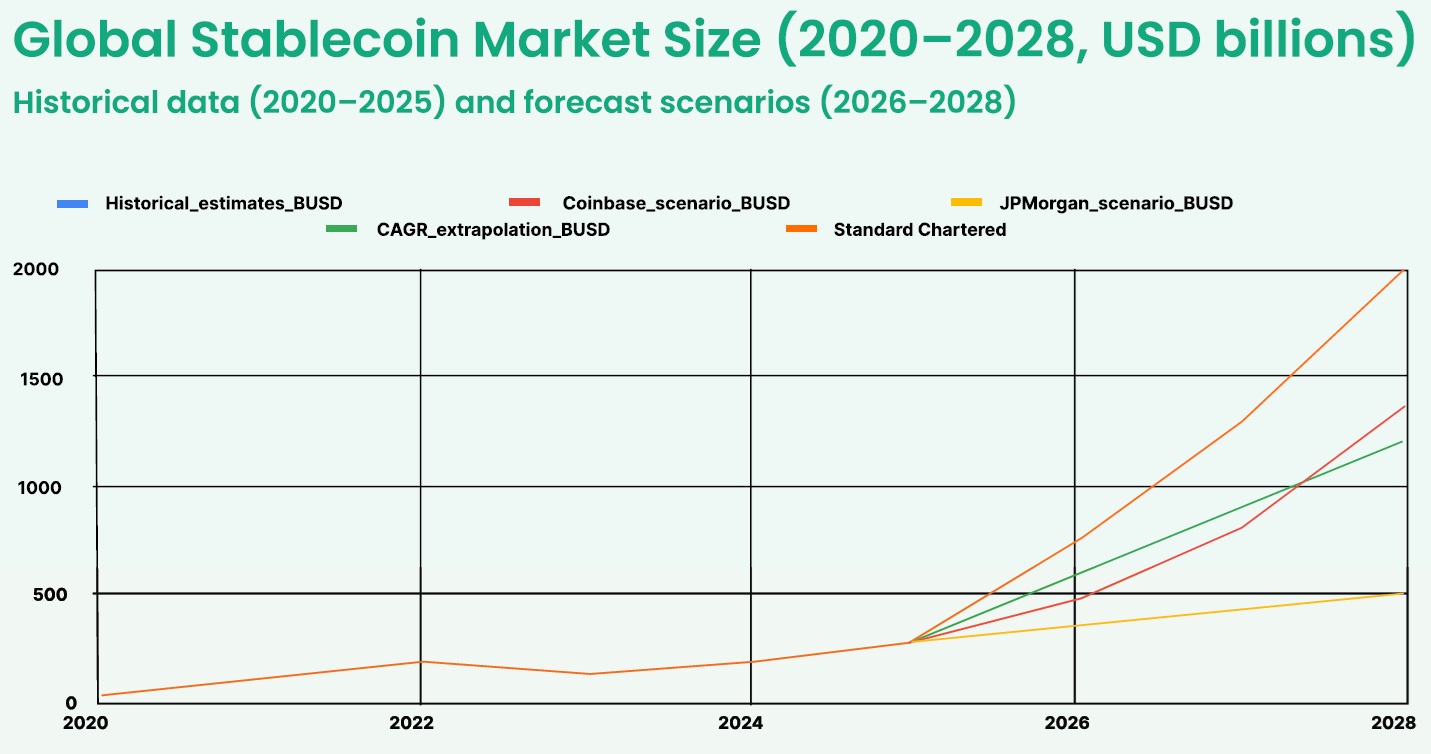

A $2 Trillion Stablecoin Market Emerges

Alongside the rise of CBDCs, stablecoins are transitioning from speculative assets to regulated financial instruments. The market—valued at $246 billion today—is forecast to exceed $2 trillion by 2028.

The maturation of the digital currencies sector owes much to a wave of regulatory frameworks introduced in 2024–2025.

Europe’s MiCA regime, the US’ new GENIUS Act, and stablecoin licensing laws in the UAE, Hong Kong, Japan, Singapore and Thailand have created a clearer operational environment.

These rules are prompting a shift toward fiat-backed, fully reserved tokens while pushing algorithmic models to the margins.

Corporate adoption is now gathering pace. B2B stablecoin payments already exceed $36 billion a year, and treasury teams are increasingly experimenting with stablecoins for cross-border liquidity and supply-chain settlement.

The 2025–2028 Inflection Point

The research highlights a cluster of major national deployments in the next two to three years.

The UAE’s Digital Dirham, Russia’s digital rouble and India’s scaled-up digital rupee will all move to general availability. Thailand and Brazil are expected to follow with retail pilots or commercial launches, while the European Central Bank edges closer to the build phase for a digital euro.

By 2028, the authors forecast that cash will represent only a minority of transactions in most advanced economies, stablecoin circulation will reach the multi-trillion-dollar range, and correspondent banking volumes will shrink by at least 40%.

The implications for banks are significant.

Direct consumer access to CBDCs raises the risk of deposit flight in times of stress, while stablecoin-based settlement threatens established payment processors.

Compliance costs for issuers are also set to rise, with annual obligations expected to exceed $10 million for major operators.

Geopolitical Shifts and the Decline of Dollar Dominance

The study argues that the US dollar’s dominance in cross-border payments is already eroding.

mBridge’s architecture enables settlement in local central-bank money without passing through dollar-based rails, an appealing prospect for countries subject to sanctions or seeking to diversify strategic dependencies.

The Gulf states’ growing involvement signals the potential for commodity flows—particularly oil—to experiment with non-dollar settlement.

At the same time, digital currency alliances are strengthening regional blocs, from ASEAN to the GCC, accelerating economic integration.

What Institutions Need to Do Now

For financial institutions, the message is blunt: digital currency integration is no longer optional.

Banks need to evaluate CBDC compatibility, test settlement on blockchain-based infrastructure, and prepare for a world of programmable money.

Corporates will need to assess whether stablecoins can improve their treasury operations. And regulators face the challenge of developing cross-border standards quickly enough to keep pace with innovation.

The next phase of this monetary revolution will be shaped less by technical experimentation and more by deployment at scale. With Asia and MENA setting the direction, the era of traditional money is entering its final chapter far faster than most anticipated.

Comments