trending

trending

As innovations go, Artificial Intelligence (AI) in payments has seen more hype than most. James Wood sorts the bits and bytes to ask where the value of AI in payments really lies – and what’s really possible.

In the early 1960s, futurologists – as people who make predictions would come to be known – said we’d be living on the moon and surviving off super-efficient vitamin pills by now.

So much for that: as that great sage Yogi Berra once said, “I never make predictions – especially about the future.”

Not that such witticisms have stopped pundits from predicting a central role for Artificial Intelligence (AI) in payments.

Allied Market Research, among many, say that AI in payments was worth $8.31 billion last year, and peg it for growth of more than 22% each year to reach a whopping $60 billion by 2031.

“As more value is exchanged online, automation via AI becomes a must.”

In part, growth in payments AI has been driven by the wider digitalisation of the sector; Plugger.ai say digital payments will account for 6% of world economic output ($7 trillion) by 2025.

Put a different way, with money moving so fast and so much value being exchanged through digital channels, automating processes is a necessity for further growth.

To that extent, there’s little debate about the value some forms of AI can bring.

Examples include the automation of areas such as invoicing, accounts receivable and data entry – functions that have traditionally been time and labour intensive.

There’s also a strong argument for AI when it comes to functions such as dispute resolution that remain slow, complex and stressful for customers.

So far, so good: but as Adrian Pillay, VP of Sales at Provenir AI puts it, “AI is a buzzword that can mean one of ten different things. It can be an expensive investment if businesses don’t figure out how it’s going to deliver value as expected.”

True indeed – and as those investments pile up, it seems some companies are asking questions about what they are getting back for their money.

Big money in – but what’s coming out?

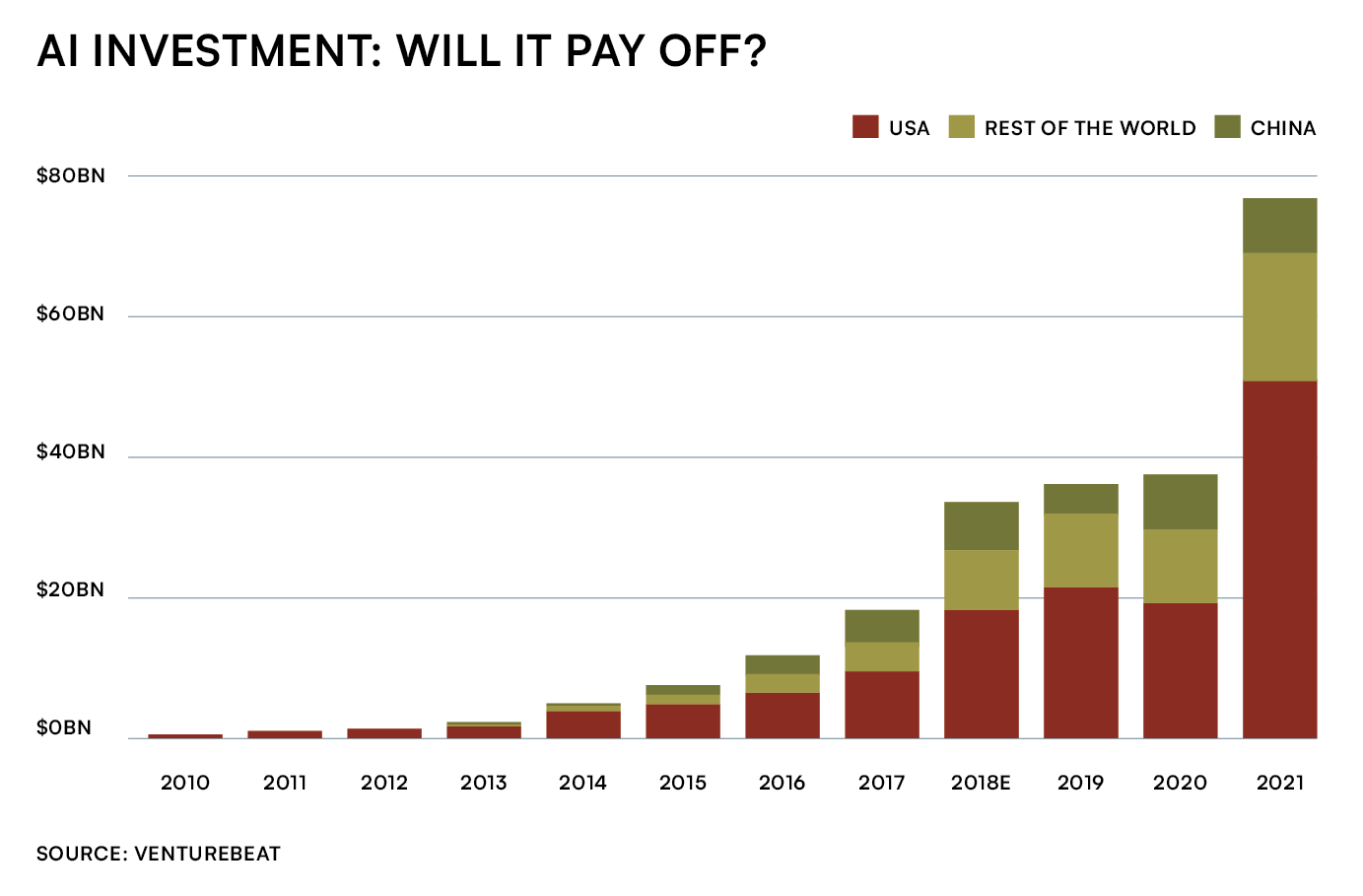

Last year, according to VentureBeat, global investment in AI more than doubled to hit $80 billion.

In payments, banks are investing two-thirds of all funds, and this sector’s bet on AI is going to get bigger by 25% in the next two years alone. But what return are firms seeing on their cash?

Despite huge sums, much hype and many promises made, AI has yet to provide a firm shield against payments fraud, for instance.

Indeed, Deloitte and others argue that the proliferation of AI is introducing its own transaction risks – after all, criminals can use AI too.

Examples of where criminals might use algos in fraud include deep faking customer IDs to access accounts, spoofing chatbots to con shoppers into providing customer information, and issuing fake invoices to an automated invoice payment system.

It’s a problem as old as the Roman Empire – “quis custodiet custodes?”, or, “who guards the guardians?”

In the case of AI, it seems that handing over control of your fraud management to machines might create extra work or, at the very least, require highly-skilled human interventions to prevent serious errors.

As Jonathan Vaux, Head of Propositions and Partnerships at Thredd, puts it: “Transaction risk can never be abolished. Implementations of AI need to be used in parallel with increased app security and other measures.

That said, AI has significant potential in areas such as automating case management in fraud, and in identifying and handling exceptions in areas such as escalated authentications.”

To these functions we could add others such as daily account reconciliation for merchants, reporting and more.

In the reporting space, small business accounting has been revolutionised by apps like Xero and QuickBooks which use APIs to link with bank accounts and provide tax information, real-time invoice management and other useful tools.

The limits of logic – and data

Another major problem with the effectiveness of AI is that it can only ever be as good as the data it’s working from.

A couple of years ago, Signifyd published a study saying that half of Europe’s SMEs still use partly or fully manual processes, meaning getting any data on such transactions would be difficult.

No doubt that situation has improved, but up-to-the minute figures from UK analytics provider Doorda suggest four in ten data scientists have struggled with the data they’re given to work with – and nine in ten have to look for alternative sources to get an accurate picture of their market.

Figures like these suggest there’s a long way to go before AI becomes truly effective.

And even where it is effective, it may be best used for guesstimates and repetitive processes, rather than forensic research.

As AI expert Gary Marcus puts it, “AI is at its best when all we need are rough-ready results, where stakes are low and perfect results optional.”

In other words, a future some envisage in which customers are protected from fraud and their needs anticipated by all-knowing machines may be very far off, if not unlikely to ever materialise.

And if it does, there are already suggestions from some quarters that AI regularly repeats the biases of its creators: those familiar with the notorious slur inflicted on some minority groups by a facial recognition software package will understand this problem.

“Too many businesses are pitching AI as if it’s batteries included, which may lead to over-promising.”

While some engineers in the US are wondering aloud whether AI has already reached its limits, it’s more likely that – in payments at least – we will continue to see useful applications in back-office functions such as invoice reconciliation and accounts receivable.

There’s also no doubt that AI can help when it comes to reducing the number of transactions that need escalated authentication, and in dispute resolution, which remains a woefully slow and paper-based business.

Most of all, though, AI is suffering from being over-hyped by many – maybe we’re all too much in the thrall of 1970s science fiction books and films.

Perhaps the last word on AI should go to Microsoft’s own AI guru Dave Mayers, who says, “too many businesses now are pitching AI almost as though it’s batteries included [which may] potentially lead to over-investment in things that over-promise.

Then when they under-deliver, it has a deflationary effect on people’s attitudes toward the space.”

Comments