trending

trending

Despite a long-standing focus on driving financial inclusion and increasing the banked population, Payments Cards & Mobile Managing Editor James Wood argues African governments need to do more to enable fintechs and banks, especially when it comes to lending.

Failure to do so could see telcom companies usurp the role of banks to the detriment of Africa’s economic potential.

For more than a decade, governments, aid agencies and supra-national bodies have preached the necessity of growing Africa’s banked population as a means of improving economic conditions.

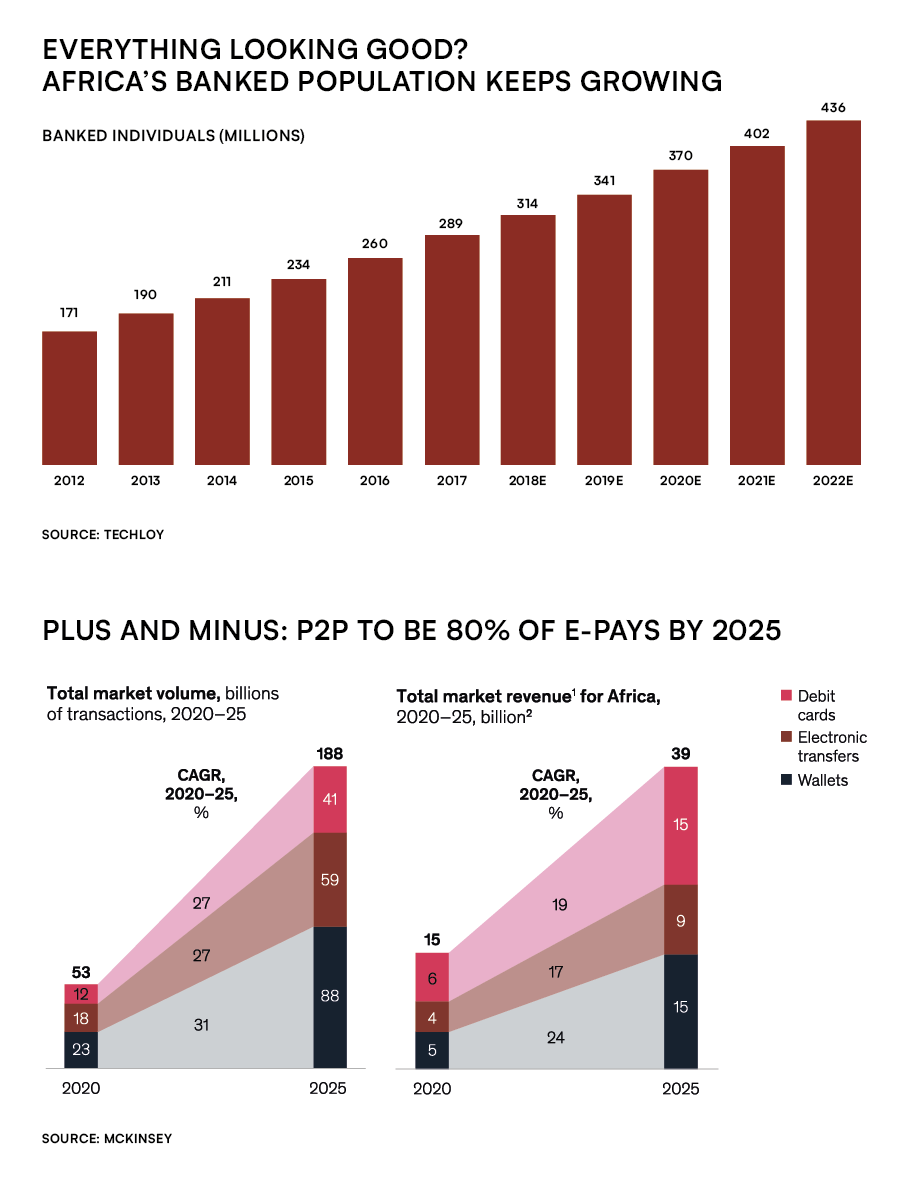

Superficially, you might say they’ve enjoyed roaring success: if just 23% of Africa’s adult population had a bank account in 2011, McKinsey report around 60% were banked by August last year.

However, bank accounts are one thing.

Getting people to use them is another – and with 90% of African transactions still using cash, it seems using payments to deliver the digital economy is a larger, more distant challenge.

Last year, the Bill and Melinda Gates Foundation announced funding for a working group of African academics, bankers and tech specialists to devise pathways towards a future digital economy.

As so often happens, though, events overtake the best-laid plans – and the explosion of mobile money offerings in Africa over the last decade in place of traditional banking may be one of the best examples of this happening anywhere in the world.

Peer-to-peer: the unheralded saviour?

There’s an apocryphal tale from the 80s of a management consultant predicting that, by the year 2000, there could be as many as 3 million cellphones in the US.

The real number, of course, was around 300 million. Likewise, few could have imagined a decade ago the stratospheric rise of peer-to-peer (P2P) payments in Africa via mobile phones through networks such as Kenya’s much-heralded mPESA, Orange Money and MTN MoMo.

Today, 750 million people in Africa – 70% of the adult population – own a mobile device, around 10% more than have a bank account.

What’s more, mobile money transactions continue to soar: the most recent data shows mobile money transactions jumped 39% to $701.4 billion in 2021 from $495 billion in 2020, growing almost twice as fast last year as in 2019-2020.

“P2P transaction growth is off the charts – but this brings systemic risk in a number of areas.”

So is it a case of job done with regards financial inclusion, case closed?

Far from it. In many ways, the rise of P2P in Africa has put banks’ position in the economic model at risk.

Far from it. In many ways, the rise of P2P in Africa has put banks’ position in the economic model at risk.

What’s worse, the regulatory regime applied to telcos is decidedly less stringent compared to that imposed on banks.

Finally, P2P transactions might work for individuals, but they don’t address other problems in the African economic model, including access to credit for small and micro-businesses, and the inclusion of these businesses in the digital economy.

African banks should beware, since players like mPESA are moving into the small business sector and looking to provide nano-lending.

However, these attempts are limited to a large extent by patchy or incomplete access to small businesses’ accounts and transaction data.

Meanwhile, many banks have been woefully slow to digitalise their service models, a fact that doesn’t improve their ability to access strong data for credit scoring.

The challenge, then, is how to build credit models in a market that doesn’t produce much reliable data at present.

And this challenge isn’t just for banks: regulators and governments should also be concerned, since access to credit will remain severely limited until lenders can act with more confidence – and that, in turn, will continue to limit economic growth.

Fintech: room to grow required

Adrian Pillay, Vice President of Sales at AI decisioning technology provider Provenir, says new fintechs are emerging across Africa to plug the gap between P2P and microbusiness services offered by telcos on the one hand, and the banking sector on the other.

“Fintechs in Africa are playing a massive role in expanding access to credit”, he says. “At a time when the divide between the banked and unbanked is bigger than elsewhere in the world, regulators should be supporting fintechs that can provide low-cost, effective credit-decisioning engines.”

“Fintech funding rose 40% in 2022 to reach almost half of all business investment in Africa.”

The facts bear out Pillay’s report of rapid growth in fintech.

McKinsey’s 2022 African Banking Report found nearly half the 5,200-odd tech start-ups in Africa focused on financial technology, while financial researchers Disrupt Africa say fintechs secured $1.45 billion in funding for 2022, up 40% from the previous year and close to half of all the funding given to businesses across the continent.

Pillay says regulators should support the fintech sector as a means of closing the gap between existing sources of funding and the needs of growing African businesses.

For instance, African banks should be looking at adding low cost, value-added credit decision engines in the cloud, a development he says could be transformational: “With better credit decisioning, it’s possible to improve the quality of outcomes in both the personal and business credit markets.

Banks and other players could move from simple yes/no decisions to looking at the provision of certain levels of credit or credit limits. That kind of service would be a huge differentiator for the players who get it right.”

Payments Cards & Mobile Opinion:

All too often, financial inclusion in Africa is a totem-pole for international aid agencies, donors and governments. But real financial inclusion means more than having a bank account or using a digital wallets.

It means systemic change through carefully-considered regulation, and the right support in the right places to support digitalisation. We’ve seen Africa develop from a pure cash economy ten years ago to the fastest-growing continent when it comes to certain kinds of electronic transaction.

Now it’s time to put modern data science techniques to work and develop the kind of credit scoring facilities that can light a fire under real, transformative growth for Africa’s economies.

Comments