trending

trending

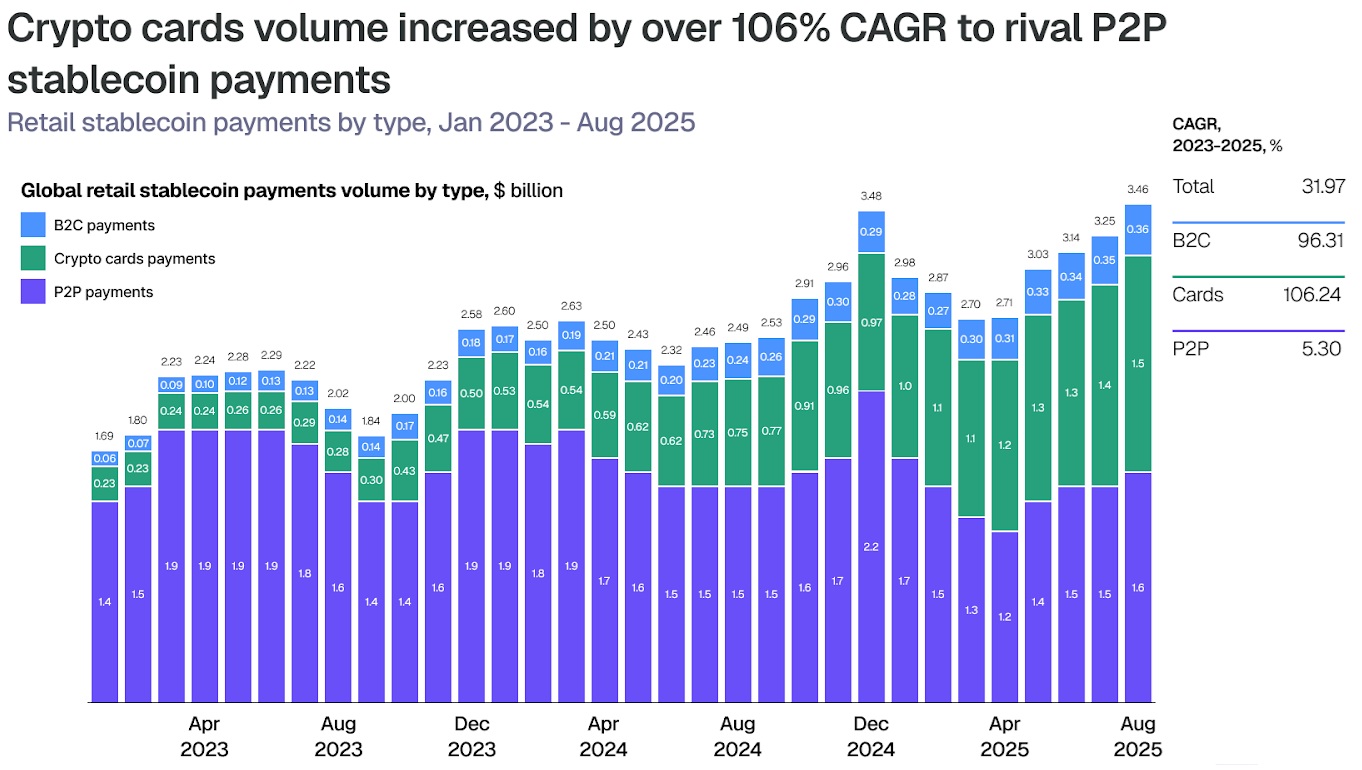

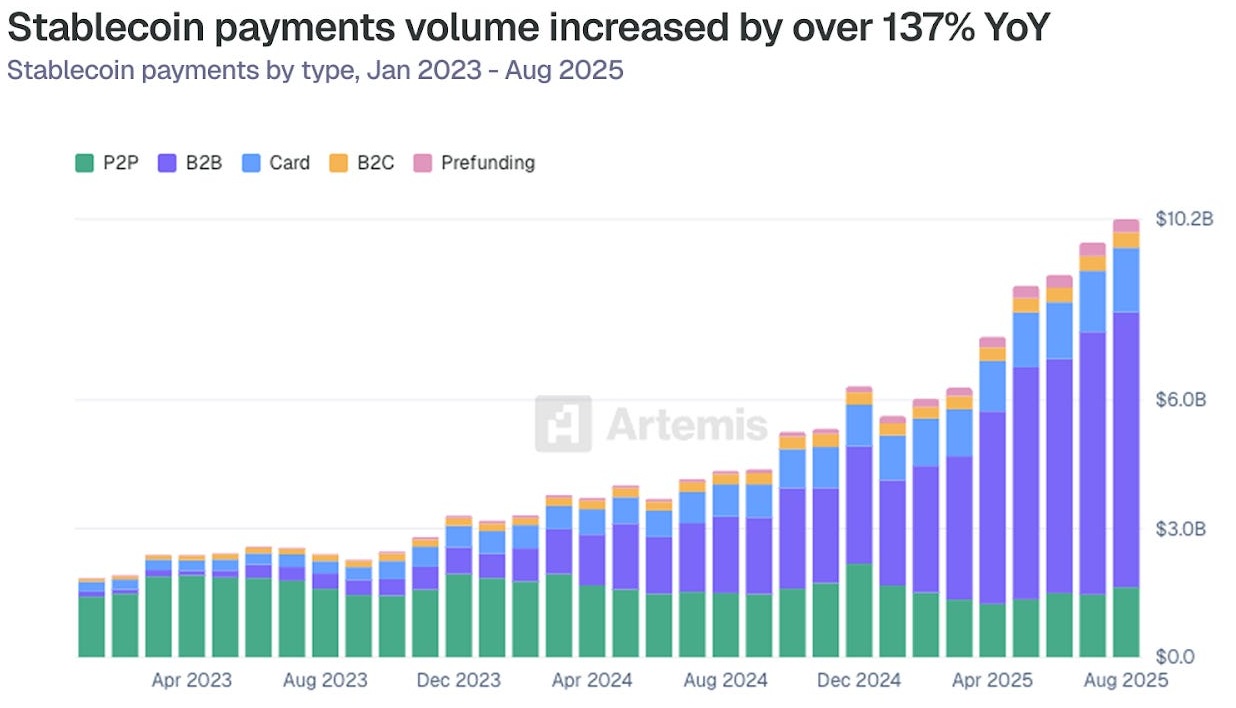

Global stablecoin card payments have reached a notable inflection point. Monthly transaction volumes climbed to around $1.5 billion in August, up from roughly $100 million at the start of 2023, according to data from Artemis.

While still modest compared with traditional card networks, the growth trajectory underscores how stablecoins are increasingly intersecting with mainstream payments infrastructure.

Unlike earlier waves of crypto payments enthusiasm, this momentum is not being driven by merchant adoption of digital currencies at the checkout.

Instead, it reflects a pragmatic synthesis: familiar card acceptance on the front end, combined with blockchain-based settlement and value storage behind the scenes.

Why Stablecoin Cards Are Gaining Traction

Stablecoin-backed cards allow users to hold value in digital dollars or other fiat-pegged tokens and spend them anywhere card networks are accepted.

This proposition resonates most strongly in markets where local financial systems impose clear frictions.

Stablecoin card opportunity concentrates where stablecoins solve tangible problems. India ($338B crypto inflows) and Argentina (46.6% USDC share) stand out as global outliers.

In countries such as Argentina, where inflation and capital controls erode confidence in domestic currencies, stablecoin cards function as a hedge as much as a payment tool.

In contrast, widespread direct merchant acceptance of stablecoins remains unlikely in developed markets.

Cards already solve payments efficiently for Western consumers and retailers, leaving little incentive to overhaul point-of-sale behaviour.

As Artemis notes, successful payment networks typically launch with strong incentives or exclusivity — a forcing function that stablecoin checkout currently lacks.

Settlement, Not Checkout, Is the Prize

The real disruption lies beneath the surface.

Stablecoins offer faster cross-border settlement, programmability and global reach — attributes that matter far more in clearing and treasury operations than at the till.

Stablecoin-backed cards effectively merge these advantages with the ubiquity of existing card rails.

This dynamic is now feeding through to the networks themselves.

Providers of stablecoin-linked cards are emerging as a key driver of demand for Visa’s stablecoin settlement services, which have reportedly reached an annualised run rate of $4.5 billion.

According to Visa executives, much of this volume originates from this new class of card issuer rather than from merchants accepting crypto directly.

Infrastructure Players Move In

Investment is following usage. Rain recently raised $250 million to expand its stablecoin payments platform, citing a 30-fold increase in active cards and a sharp rise in transaction volumes over the past year.

Its pitch is telling: compliant cards that work everywhere Visa is accepted, while quietly leveraging stablecoins for funding, rewards and payouts.

For now, stablecoin cards remain a niche. But their growth suggests a broader lesson for payments innovation: the most durable change often happens invisibly, reshaping settlement and liquidity while leaving the consumer experience largely untouched.

Comments