trending

trending

Kraken is making its boldest push yet to position crypto as a viable everyday financial rail, unveiling a series of upgrades to its Krak app that take direct aim at both legacy banks and Europe’s fast-growing neobank sector.

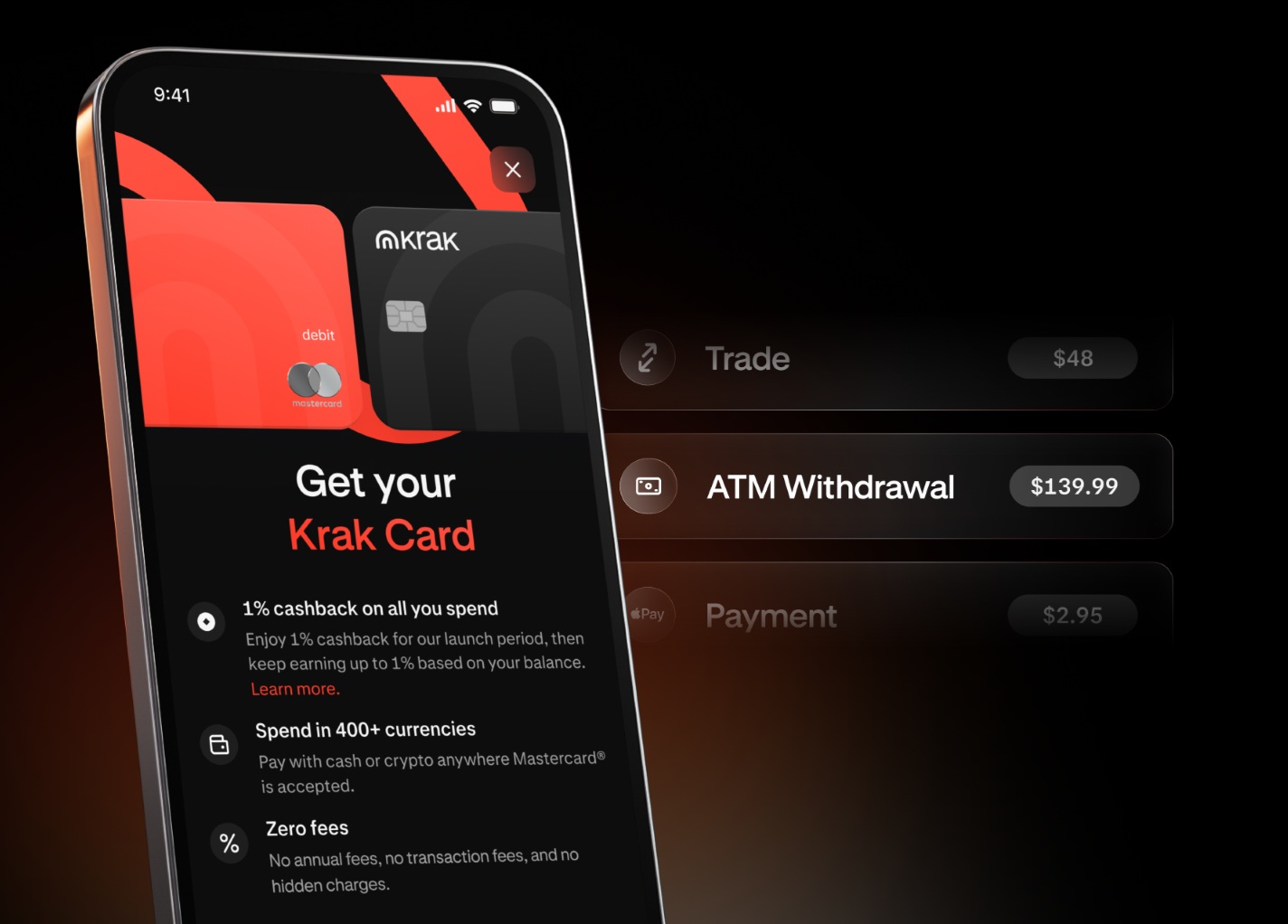

Kraken’s Krak Card

The phased launch of the Krak debit card, paired with new income and wealth-building features, represents an ambitious attempt to turn a crypto wallet into a full primary account for consumers.

At the heart of the expansion is the Krak Card, now rolling out across the UK and EU.

Leaning on Mastercard’s global network, the card allows users to spend from more than 400 crypto and fiat balances held within the Krak app.

Purchases can be covered using multiple assets in real time, with users able to prioritise which holdings are tapped first and ring-fence the ones they prefer not to spend.

The 1% cashback on every transaction — payable in fiat or Bitcoin — positions the product squarely against the rewards mechanics offered by premium neobanks.

Kraken argues the distinction between “money” and “digital assets” is becoming obsolete.

The card’s design reflects that philosophy: a £100 transaction can, for example, be split automatically between £80 in cash and £20 in Ethereum or Solana, with instant conversion at checkout.

For Kraken, the goal is to give customers a single interface for multi-asset spending without FX fees or monthly charges.

DeFi-Powered Yield Moves Into the Spotlight

Alongside the payment features, Kraken is sharpening its pitch to savers.

The forthcoming Vaults product is designed to route assets into audited decentralised lending protocols, aiming to offer returns that materially exceed those available through traditional institutions.

Kraken says eligible assets could earn yields north of 10% APY, a level likely to attract both crypto-native users and yield-hunters frustrated by stagnating bank savings rates.

The firm already offers up to 3.6% on selected holdings, but Vaults marks a step change, pushing DeFi exposure into a more accessible, managed environment.

Users will be able to tailor allocations to reflect their risk tolerance, positioning Krak as a hybrid between an investment app and a digital current account.

Salary Deposits: A Play for Primary Account Status

Perhaps the most consequential feature is the introduction of salary deposits for UK and EU users.

By inviting customers to route wages directly into Krak, Kraken is signalling its intention to compete not just on payments or investment, but on core account relationships.

That move, coupled with instant global transfers and multi-asset spending, could encourage a cohort of users to shift their financial “centre of gravity” away from traditional banks.

A Broader Strategic Bet on Europe

These developments sit atop Kraken’s strengthened regulatory footing in Europe, including its MiCAR licence authorised by the Central Bank of Ireland.

With more than a decade of FCA-regulated operations in the UK, Kraken is leveraging compliance credentials to scale Krak as a standalone consumer brand.

With 450,000 app downloads since June 2025 and further products — including credit and merchant rewards — on the roadmap, Kraken is laying the groundwork for crypto’s most concerted challenge yet to mainstream retail finance.

Comments