trending

trending

Banks are facing mounting pressure to modernise their merchant services as a new wave of Paytech firms threatens to lure away small and mid-sized businesses with faster, cheaper and more reliable solutions.

According to Capgemini’s World Payments Report 2026, as many as 40% of merchants are considering shifting to Paytech providers, signalling an inflection point in the battle for merchant relationships.

The findings point to a growing dissatisfaction with banks’ current offerings.

Only 15% of small merchants and 22% of mid-sized merchants report being satisfied with their payment providers. At the heart of this discontent lies the friction embedded in onboarding, payment reliability and fraud prevention.

For example, merchant onboarding with banks can take up to seven days and cost nearly $500, compared with less than 60 minutes and a cost closer to $200 for many PayTech alternatives.

The contrast is stark.

Paytechs have been designed from the ground up for a digital-first environment, enabling them to meet demands for speed, transparency and integration.

By comparison, banks have long prioritised card issuing over merchant acquisition, leaving the sector under-invested. The result is that merchants endure up to nine hours of annual downtime due to unreliable systems, with losses from fraud running at about 2% of revenue.

Paytechs Pull Ahead in Innovation

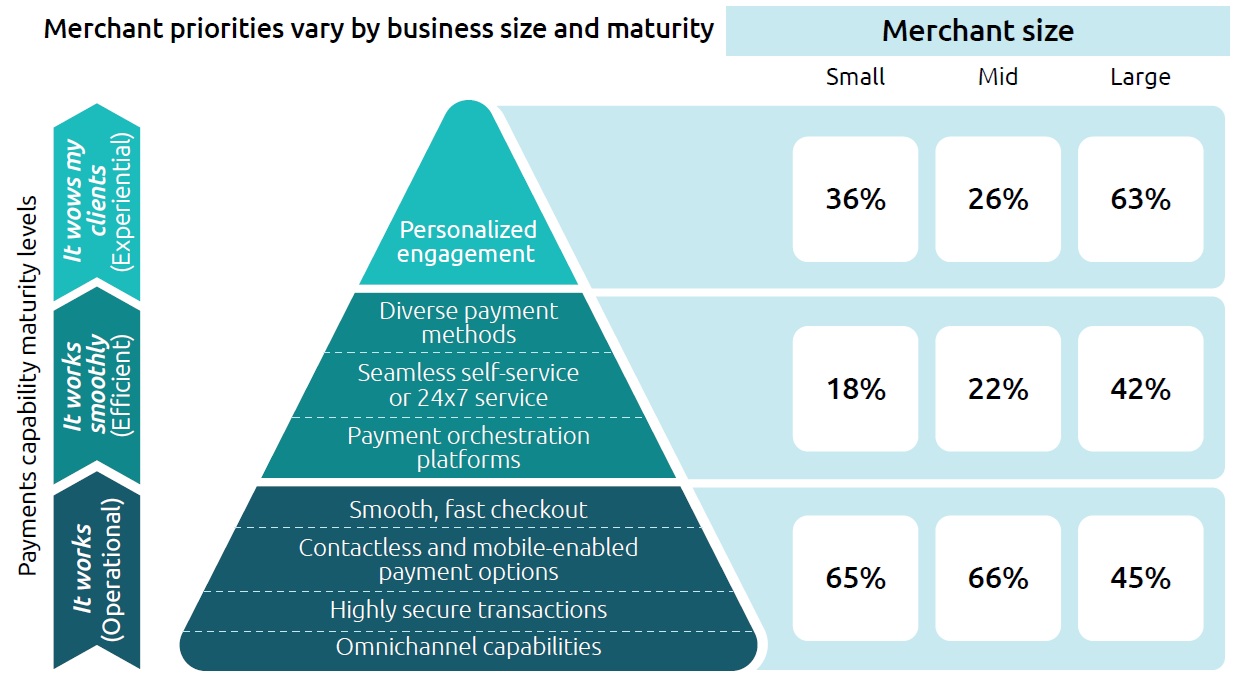

One of the clearest divides is in technology adoption.

The report shows that 70% of Paytechs have deployed payment orchestration tools — enabling intelligent routing of transactions — compared with just 47% of banks.

Similarly, 60% of Paytechs are using Generative AI in their operations, far ahead of the 41% of banks that have embraced it.

Paytechs are also shaping market expectations by engaging early with regulatory innovations.

Nearly half are preparing for central bank digital currencies (CBDCs) and stablecoins, while 59% are prioritising digital identity frameworks.

Banks, in contrast, lag behind at 23% and 38% respectively. This growing disparity highlights why merchants see Paytechs as more agile, responsive and aligned with the future of commerce.

The Shift in the Global Payments Mix

The urgency for banks is underscored by structural changes in global payments.

Non-cash transactions have quadrupled over the past decade and are projected to exceed 3.5 trillion annually by 2029.

Instant payments and digital wallets are driving this surge, rising from 13% of global transactions in 2020 to 25% in 2024.

In the same period, the share of card payments is expected to decline from 65% to 52%.

Regional dynamics amplify the challenge.

Asia-Pacific is the clear growth engine, accounting for nearly 800 billion digital transactions in 2024, with annual growth forecast at 21% in 2025.

North America, by contrast, remains more card-heavy and is growing at just 7% annually. Europe sits between these extremes, but faces the same merchant pressures as PayTech adoption accelerates.

Can Banks Win Back Merchants?

Despite their shortcomings, banks retain important advantages. Merchants still trust banks’ stability, long-term presence and broad suite of financial products.

Two-thirds of merchants say they prefer traditional providers for core financial services, even if satisfaction levels are low.

The opportunity lies in leveraging these strengths to deliver the same convenience and innovation as Paytech rivals.

Merchants are clear: they want seamless onboarding, embedded services tailored to their industry, and integration into broader ecosystems such as food delivery or retail loyalty platforms.

Eight in ten say they would switch back to a bank if it could offer Paytech-level services at a competitive cost.

The message from Capgemini’s report is unequivocal: banks must act decisively.

Failure to modernise risks losing relevance in the merchant ecosystem altogether.

But those institutions that embrace Generative AI, payment orchestration and value-added digital services could not only halt the exodus, but also position themselves as indispensable partners in the next era of global commerce.

Comments