trending

trending

The once-ubiquitous wallet is fast becoming an accessory of the past. New research from LINK shows that fewer than half of UK adults still consider a wallet or purse an essential part of everyday life.

Among 18–24-year-olds, that figure falls to just 38 per cent, underlining a generational shift that has redefined how Britons manage and spend their money.

Digital Payment Rule

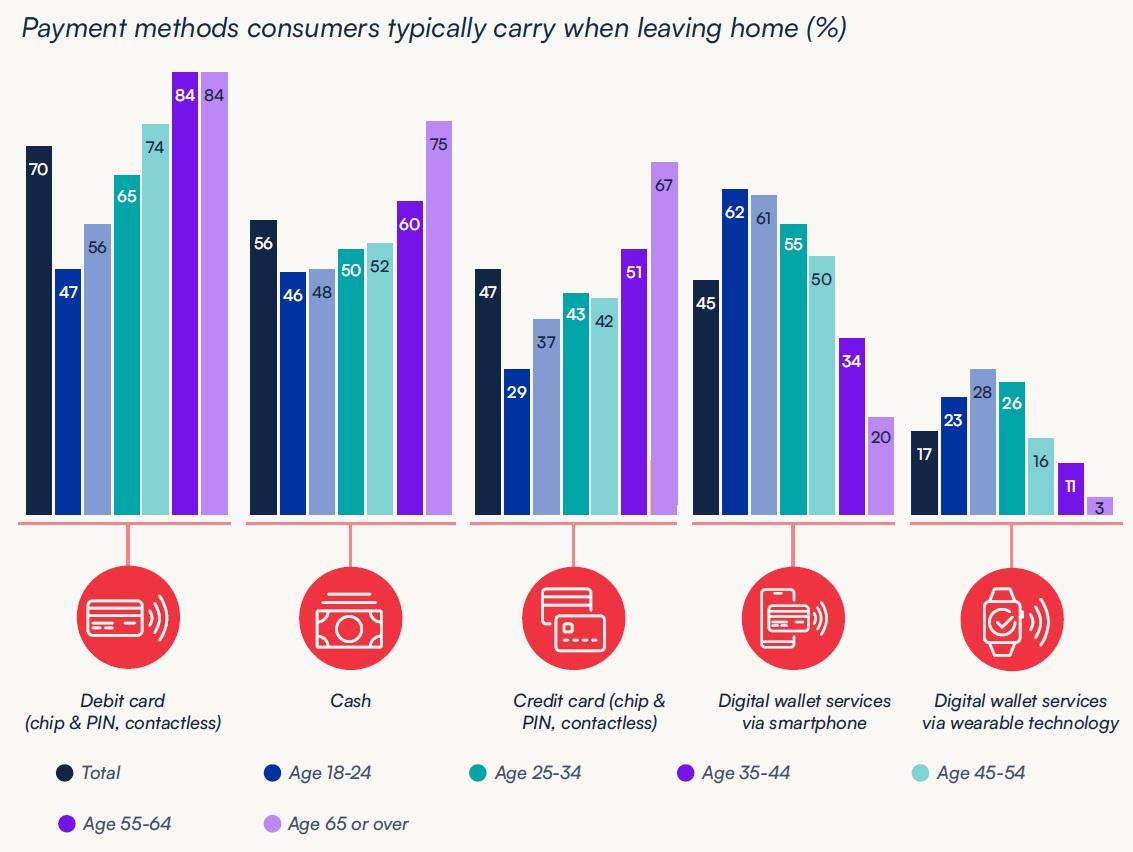

This change has been driven by the rapid uptake of digital payment methods.

Smartphones and smartwatches now serve as de facto wallets, with over half of consumers (51 per cent) carrying a digital wallet when they leave home.

Among younger adults, three in five already view mobile wallets as their “go-to” way of paying, while only a minority rely on debit or credit cards.

The contrast with older generations is striking: over-65s remain far more attached to physical wallets, though even they are increasingly comfortable with contactless cards.

Wider Cultural Forces

The shift reflects wider technological and cultural forces.

The near-universal penetration of smartphones among young people, coupled with rising ownership of wearable devices, has created an environment in which digital payments feel natural and convenient.

The pandemic accelerated this move, with cash often discouraged and card terminals configured for contactless.

For many in Generation Z, adulthood has been shaped by a world in which physical cash plays only a peripheral role.

Dependency Brings Risk

Yet this digital dependency brings risk.

The LINK report highlights that almost two-thirds of UK adults have already experienced some form of payment disruption, and more than a third of those failures stemmed from system outages.

Consumers who rely solely on a single payment method – whether one card or a single digital wallet – are particularly vulnerable.

At the median, Britons carry just £20 in cash when they leave the house, and many keep no cash reserves at home at all. In a prolonged outage, millions would be left without an immediate fallback.

Trust is another challenge.

While 86 per cent of people feel secure when paying by card or bank transfer, only 61 per cent express the same confidence in smart device payments – a figure that falls sharply among older age groups.

This hesitancy underscores the paradox of modern payments: digital wallets may dominate daily usage, but they are not yet universally trusted.

Socio-Economic Factors

Socio-economic factors also influence adoption.

Higher-income households are far more likely to embrace digital wallets, with 70 per cent of those earning £100,000 or more carrying one, compared to just 40 per cent in households earning £10,000–£15,000.

Similar disparities emerge across ethnicity and gender, suggesting that digital inclusion remains uneven.

The implications are clear.

Convenience may now “wear the crown,” but resilience remains paramount. A diversified payments ecosystem – in which cash, cards and digital coexist – is essential to protect consumers from disruption and ensure inclusivity.

Policymakers and industry bodies alike must strike a delicate balance: fostering innovation while safeguarding access to cash and reinforcing confidence in digital infrastructure.

The wallet may be on its way to becoming a relic, but for now, it still plays an important role as a safety net.

In the evolving landscape of UK payments, the challenge is not to resist digital progress, but to ensure it does not leave consumers exposed when systems fail.

Comments