trending

trending

The way British consumers choose to pay has always been a mirror of wider economic, cultural and technological trends.

From chip-and-PIN’s steady rise in the early 2000s to the mobile wallet boom of the late 2010s, every shift has reflected changing attitudes towards convenience, trust and security.

Now, in 2025, a new survey of 2,000 UK shoppers provides a detailed snapshot of payment habits both in-store and online — and reveals that assumptions about a “cashless society” may have been premature.

Contactless remains king of the high street

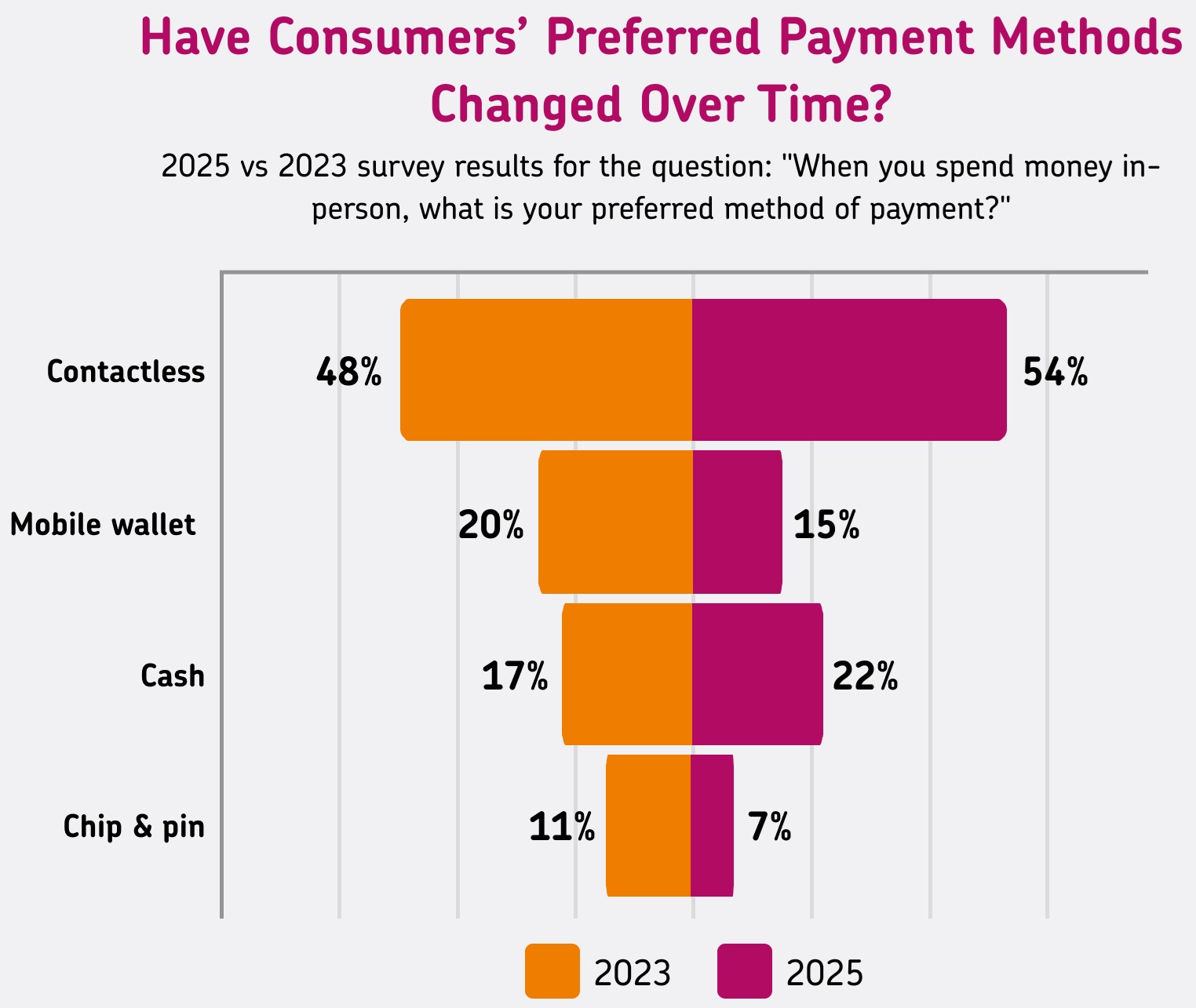

More than half of UK shoppers (54%) now say contactless is their preferred in-store payment method — a 14% increase since 2023.

More than half of UK shoppers (54%) now say contactless is their preferred in-store payment method — a 14% increase since 2023.

For many, the attraction lies in the sheer speed of tapping to pay.

Nearly nine in ten respondents (87%) cited convenience as the principal reason for choosing contactless, while 44% valued faster transaction times and 31% highlighted its near-universal acceptance.

Demographics reinforce the dominance of contactless. It is the top choice across all age groups, though younger adults are less wedded to it than their parents or grandparents.

Only 42% of 25–34s listed contactless as their favourite, compared to 62% of over-55s. Gender also plays a role: 57% of women prefer contactless, compared with 52% of men.

Cash confounds expectations

One of the survey’s most striking findings is the resurgence of cash.

While card payments have become synonymous with modern retail, the humble note and coin have regained traction.

Cash preference in-store has risen by 26% since 2023, making it the second most popular method behind contactless and overtaking mobile wallets.

More than half of consumers (56%) still carry cash daily, with only 3% saying they never use it.

Among over-55s, two-thirds (66%) always have cash on hand, but even half of 18–24s keep notes and coins at least some of the time.

Shoppers cite convenience (61%) and budgeting (41%) as the main reasons for sticking with cash, while more than a third (37%) believe it is faster in certain circumstances.

Notably, nearly a third (29%) see cash as the most secure option — a finding that challenges the prevailing narrative of digital’s dominance.

For small businesses, this comeback matters. Although digital solutions attract attention, ignoring cash could alienate a significant customer base.

As Rona Warne of Global Payments notes, younger shoppers in particular still associate cash with security — meaning merchants must work harder to communicate the safety of card and digital transactions.

The declining appeal of mobile wallets in-store

If cash has benefitted from a rebound, mobile wallets have experienced the opposite.

Once hailed as the natural successor to cards, their popularity for in-store payments has dropped by a quarter (26%) since 2023.

Just 15% of shoppers now select mobile wallets as their preferred way to pay in person.

The decline may reflect ongoing concerns around acceptance and reliability.

While mobile wallets remain popular among 18–24s, who use them more than any other age group, the technology has yet to displace contactless cards among the broader public.

Online: cards remain dominant

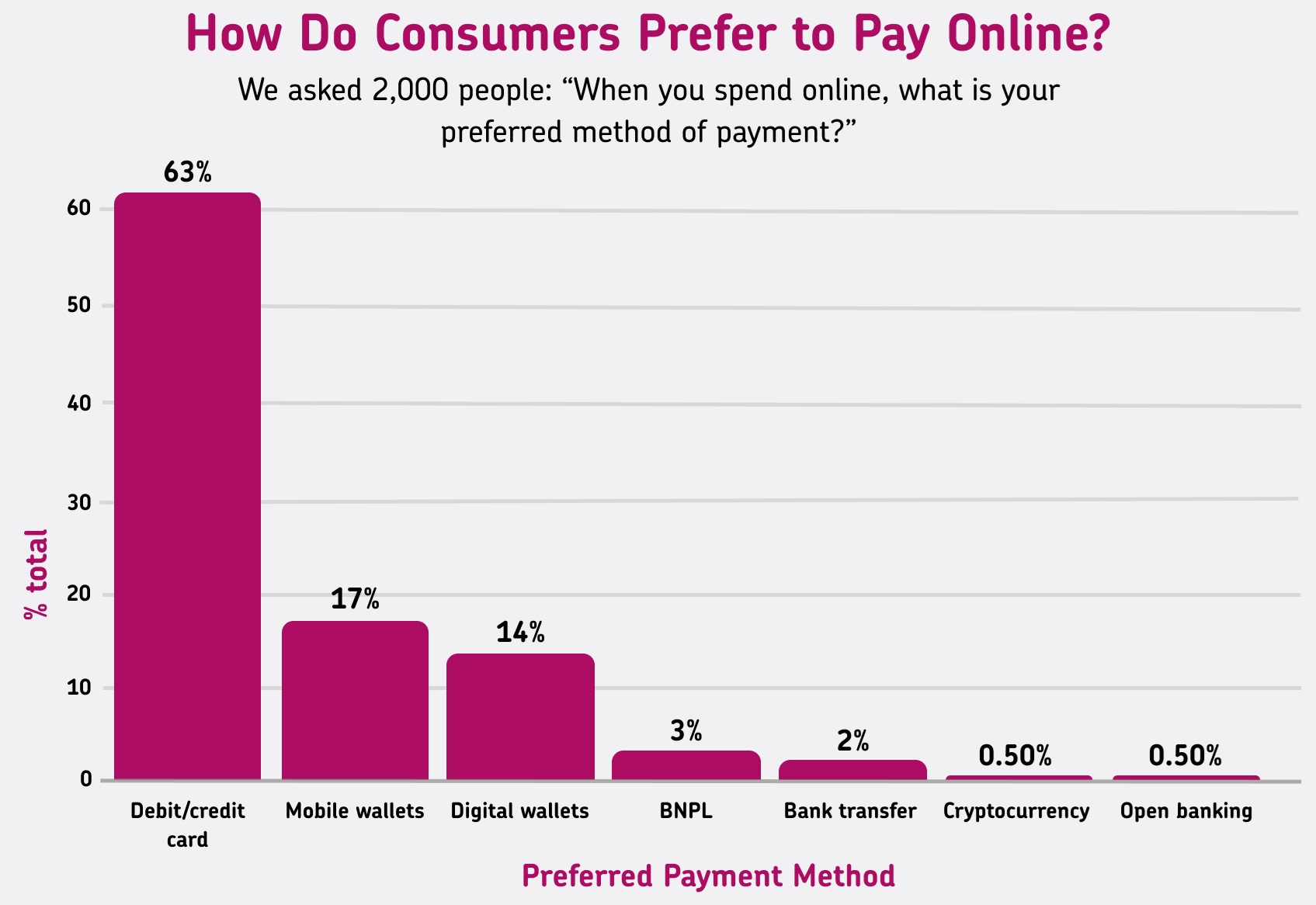

When shopping online, debit and credit cards are still the clear front-runner, with 63% of UK consumers selecting them as their default option.

When shopping online, debit and credit cards are still the clear front-runner, with 63% of UK consumers selecting them as their default option.

For older shoppers, cards are virtually unchallenged: 77% of over-55s prefer them. Cards’ appeal rests largely on familiarity and acceptance, with 69% of respondents saying they stick with them because they work everywhere.

But younger generations are rewriting the script. Among 18–24s, mobile wallets have overtaken cards online: 42% favour wallets compared with 39% for debit and credit.

Digital wallets such as PayPal also remain popular, particularly among shoppers aged 25–44. Buy Now Pay Later (BNPL), by contrast, has failed to break through in a significant way, with just 3% of all respondents preferring it.

Gender divides are less pronounced online but still visible. Men lean more heavily towards cards (67% versus 58% for women), while women are more inclined towards mobile (19% vs 14%) and digital wallets (15% vs 13%).

Women are also twice as likely as men to prefer BNPL (4% vs 2%).

The slow rise of Open Banking

Open Banking has been heralded as a transformative technology, but consumer attitudes remain cautious.

Just over half (52%) of respondents said they feel comfortable making payments via Open Banking, while nearly a quarter (23%) are opposed.

Security concerns dominate resistance: 38% worry about hacking or data breaches, and 29% are uncomfortable sharing banking details with third parties.

Yet among those open to the method, trust in security is the leading factor (46%), followed by simplicity and speed (31%).

Unsurprisingly, younger shoppers are more receptive. Only 16% of 18–24s expressed discomfort, compared with one-third (33%) of over-55s.

For businesses, this highlights both opportunity and challenge: Open Banking adoption is growing, but building consumer confidence will take time and education.

Payments in 2025: a balancing act for businesses

The 2025 snapshot of UK consumer payments habits underlines a core reality: there is no single solution that satisfies everyone.

Convenience is the dominant driver across all methods, but different demographics interpret it differently.

Older shoppers continue to rely on cards and cash, younger consumers embrace mobile wallets, and the middle ground expects flexibility.

For small businesses, the message is clear. Limiting payment acceptance risks alienating customers and losing sales.

Shoppers are increasingly intolerant of inflexibility: more than half (52%) now say they find cash-only stores inconvenient, up from 33% just two years ago.

Offering a mix of cards, contactless, mobile wallets, and even cash is no longer just good practice — it is a competitive necessity.

As Warne notes, reassurance also matters. Displaying trusted logos, maintaining secure systems and ensuring reliability are as critical as offering the latest technology.

In short, payments in 2025 are not about predicting the death of one method over another but about recognising coexistence.

Consumers want speed and convenience above all, but they also want choice.

Businesses that respond to this reality will be best placed to thrive on the UK’s evolving high street and in its growing online marketplace.

Comments