trending

trending

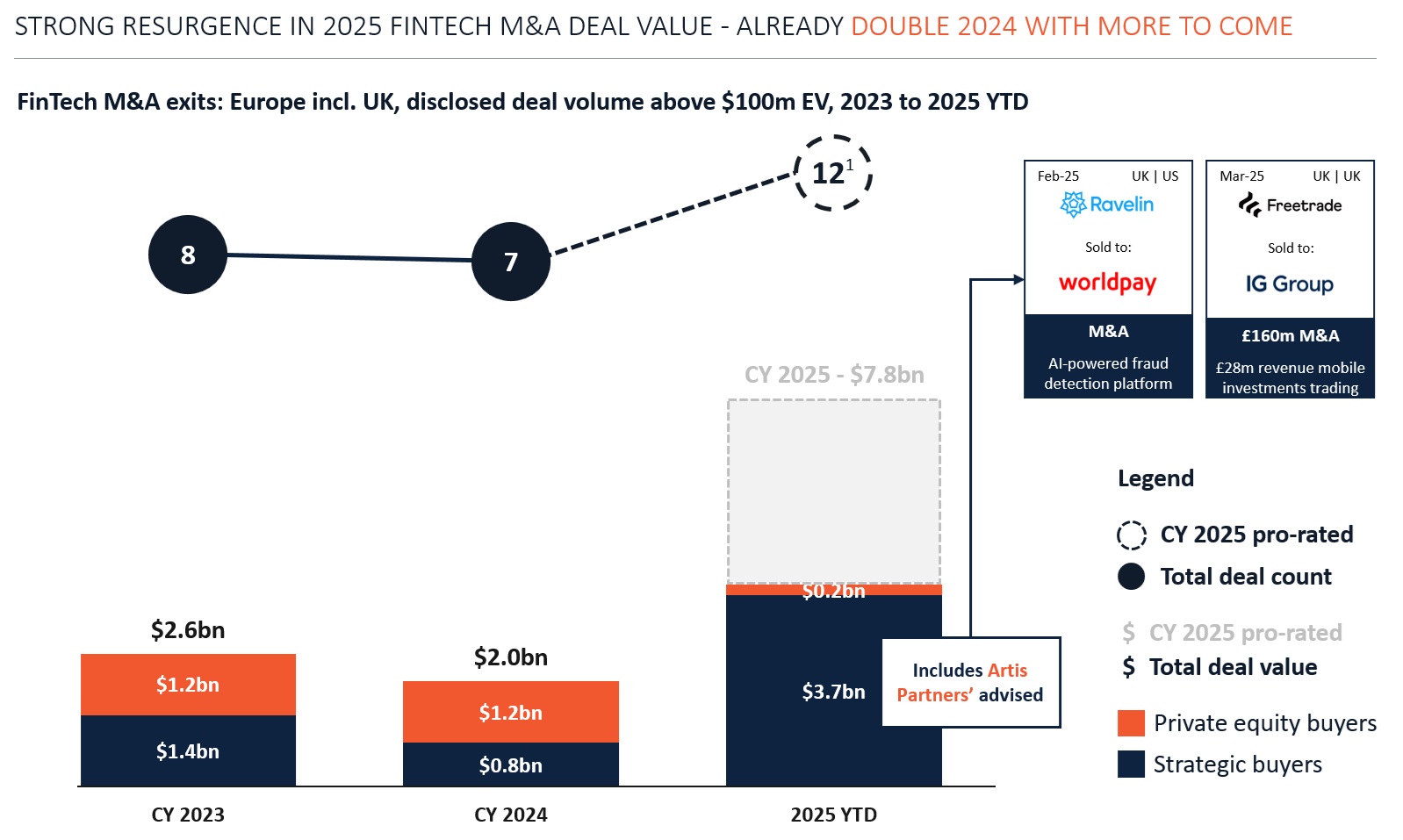

European fintech M&A is surging in 2025, with disclosed deal value for $100 million-plus transactions reaching $3.9 billion in H1 2025, almost double the total recorded for all of 2024.

The data, released by investment bank Artis Partners based on PitchBook figures, signals an accelerating consolidation wave set to redefine Europe’s financial technology landscape.

“This marks the inflection point we predicted,” commented Victor Basta, Managing Partner at Artis Partners.

“Fintech M&A is being driven by buyers targeting the maturing middle tier: profitable, commercially proven companies no longer positioned for breakout IPOs but holding strong strategic value.”

Targeted Acquisitions

Rather than focusing on unicorns such as Klarna or Revolut, or early-stage fintechs yet to scale, acquirers are targeting firms generating up to £50–100 million in annual revenue, growing steadily at 20–50% per annum, and often profitable or near break-even.

The economic logic is clear: as growth becomes more capital-intensive, particularly in consumer-facing segments with rising customer acquisition costs, fintechs are hitting a ‘natural ceiling’ – creating prime opportunities for strategic buyers.

Recent deals exemplify this trend.

IG Group acquired investment app Freetrade for £160 million, while Worldpay purchased fraud detection platform Ravelin.

Overall, strategic buyers accounted for approximately 95% of total deal value across the six disclosed fintech M&A deals over $100 million in H1 2025.

“These exits are driven by clear strategic logic on both sides,” Basta explained.

“For acquirers, integrating proven fintech platforms strengthens their ecosystem, while for founders and investors, M&A offers a path to scale and liquidity in a market where larger funding rounds have become more difficult to raise, particularly with capital now concentrated heavily on AI startups.”

Europe’s Fintech Sector

Indeed, Europe’s fintech sector is entering a period of structural realignment.

After a decade of explosive growth and extensive VC backing, the market is maturing, and successful exits are becoming crucial for fund performance.

Basta predicts that up to a third of Europe’s mid-tier fintechs could be acquired over the next three years, reshaping payments, regtech, trading, and consumer finance around a smaller number of scaled platform providers with potential to exceed $1 billion in value.

“This is not just a sector trend – it is a key inflection point for the European venture capital ecosystem that nurtured these fintechs,” said Basta.

“The next chapter is not about the next unicorn. It is about the next wave of strategic exits that will define the ecosystem for years to come.”

With M&A momentum set to continue into H2 2025, European fintech appears poised for an era of rapid consolidation, strategic recalibration, and the emergence of a new generation of dominant payments and financial infrastructure providers.

Comments