trending

trending

In 2025, Sweden stands as a global exemplar of cashless transformation. According to the Payments Yearbooks’ Sweden 2025 profile, the Swedish payments market has undergone near‑complete digitalisation, with consumers and businesses alike embracing convenience, efficiency, and cost‑effectiveness.

Yet this success brings with it new challenges around resilience and inclusivity in uncertain times.

Digital Dominance: Cash Becomes Obsolete

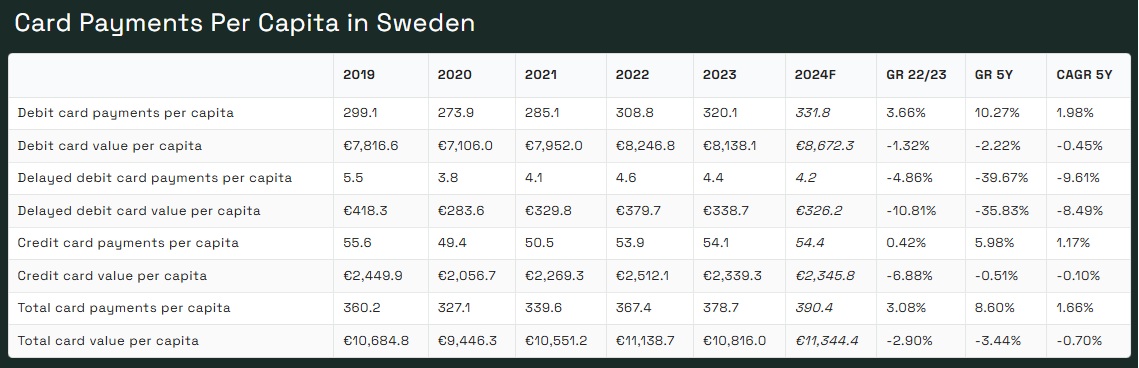

Sweden’s digital transition is evident in its declining reliance on cash.

Over recent years, more than half of small retailers have stopped accepting cash altogether, reflecting a wider national trend away from banknotes.

Nearly all everyday payments are now executed digitally—chiefly via cards, mobile wallets, or instant transfers.

This shift is underpinned by real‑time clearing infrastructure such as Bankgirot’s instant settlement and the RIX‑INST system, linked to the Eurosystem’s TIPS platform.

Swish and the Instant‑Payment Revolution

The mobile app Swish, launched in 2012 by a consortium of Swedish banks in collaboration with Bankgirot and the Riksbank, has grown to approximately 8 million users—nearly 80% of Sweden’s 10.2 million population.

Its success typifies the country’s broader adoption of instant payments for person‑to‑person (P2P), person‑to‑business (P2B), and business‑to‑business (B2B) transactions, as the public anticipates immediate settlement and flexible payment capabilities.

Contactless and Mobile Wallets Gain Ground

In parallel with Swish, contactless card payments and NFC‑enabled mobile wallets have become widespread.

The advent of SoftPOS (software point‑of‑sale) allows smartphones and tablets to accept contactless payments without dedicated terminals, opening instant payment acceptance to small businesses and micro‑merchants.

Open Banking, e‑ID and Biometrics in the Financial Mix

Open Banking has seen substantial progress, with API frameworks gaining traction across financial institutions.

Meanwhile, Sweden’s banks are deploying digital ID (eID) systems integrated with biometric authentication to enhance security and user experience.

AI‑driven fraud detection is also increasingly embedded in banking operations, signalling a holistic approach to digital transformation.

Cryptocurrencies and CBDC: The E‑Krona Question

While still nascent, Sweden is actively exploring cryptocurrencies, stablecoins, and the potential launch of an e‑krona.

The Riksbank has been investigating a central bank digital currency (CBDC) since 2017. The Yearbook profile confirms ongoing pilot initiatives and market readiness for future digital currency deployment.

Decline in Cash Infrastructure

Consistent with reduced cash usage, physical ATM numbers and withdrawal volumes continue to fall. Despite this, point‑of‑sale terminals remain prevalent.

However, card‑based and digital wallet payments now dominate terminal transactions, underscoring a substantive shift in consumer behaviour .

While efficiency has long driven the digital payments agenda, the Riksbank stresses the importance of safety and inclusiveness.

The 2025 report argues that financial infrastructure must remain resilient even in times of crisis, with measures to ensure universal access.

Notably, almost one‑third of small business respondents admitted not knowing their payments costs, prompting calls for greater transparency and regulatory scrutiny.

Forecasts for Continued Digital Growth

The 2025 profiles and forecasts from Payment Yearbooks envisage sustained growth in e‑commerce, contactless and mobile payments, along with increased adoption of Open Banking and biometric ID.

Sweden’s evolution offers a case study in orchestrating a digitally advanced, inclusive, and secure payment ecosystem.

By 2025, Sweden has taken a commanding position in the global shift to digital payments.

Real‑time settlement via Swish and RIX‑INST/TIPS, paired with contactless innovation, biometric ID, and robust regulatory focus, signal not only maturity but ambition—a nation preparing for cryptocurrencies and potentially a digital krona.

Yet as Sweden reaches this digital apex, safeguarding access, transparency, and infrastructure stability will become paramount priorities.

Its model shows how digital payments can drive inclusion and efficiency, but only when balanced with resilience and regulatory rigour.

For payment professionals and policymakers worldwide, Sweden’s journey provides both inspiration and caution: digital payments are transformative, but only if they remain safe, transparent, and truly inclusive.

To access the Sweden Report CLICK HERE

For a Sample Country Report CLICK HERE

Comments