trending

trending

New research shows that growth opportunities across the payment sector are better than they’ve been in a long time – but traditional “big players”, from banks to processors and retailers, are among the worst-equipped to take advantage, despite holding many of the aces at present.

To remedy the situation, major players need to be spending a lot more on digitalising not just their client experience, but also their back-end systems.

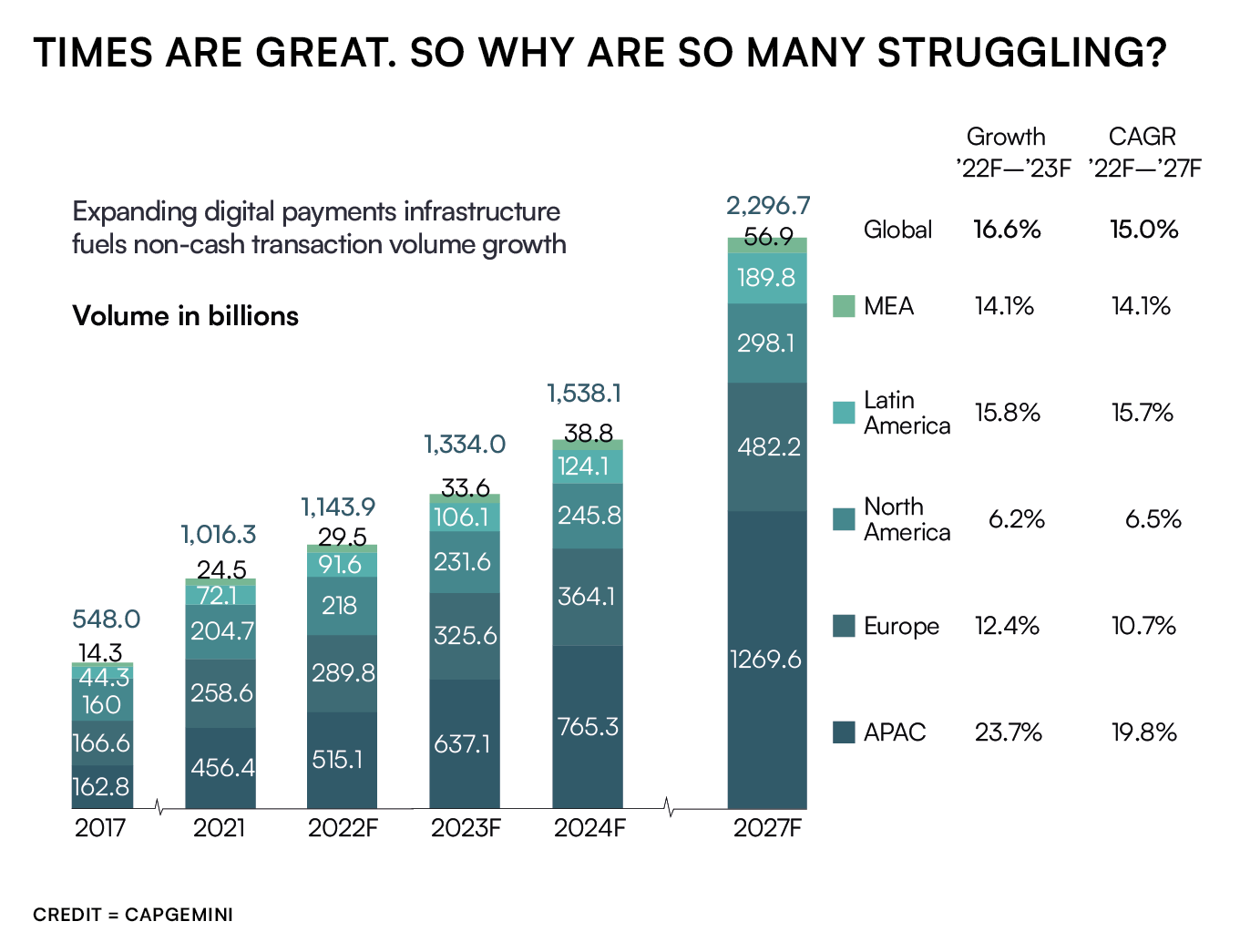

According to the Capgemini Research Institute’s 2023 World Payments Report, non-cash transaction volumes will reach $1.3 trillion globally by the end of 2023.

The report says growth will accelerate to $2.3 trillion by 2027, equivalent to a rate of 15% p.a., as consumers and businesses adopt new digital payment schemes.

CapGemini also expect new payment methods such as instant payments, account-to-account and QR-code payments to constitute around 30% of total volume, with traditional payments (cheques, direct debits, cards and credit transfers) dropping to 70% of non-cash transactions.

“As new payment methods rise, the bulk of growth is going to go to fintechs and digital-first banks.”

On the face of it, any payments professional would be glad to hear this news.

However, the problem for traditional players is that the bulk of this growth will go to insurgents to the payments market, whether that’s big tech firms muscling in, or all-digital upstart banks like N26 and Starling.

According to Jeroen Holscher, Head of Global Payments and Cards Practice at CapGemini, that’s because traditional financial institutions have invested heavily in their user experience (apps and web interfaces) at the same time as they grapple with the soaring costs of maintaining legacy systems – costs which McKinsey say eat up nine dollars in ten of any bank IT budget.

Rather than purely concentrating on digitalising the customer experience, banks should instead be looking harder at how to digitalise their back-office systems.

To date, according to Mr. Holscher, “banks have taken more of a piecemeal approach. That’s OK, but it needs to be done in the context of a wider strategy that includes a plan to decommission and replace legacy technologies.

Banks still have further to go when it comes to digitalising their role as credit institutions, rather than as service providers – specifically in areas such as cash management and corporate services, where there’s still a lot of room for automation to make a difference.”

Comments