trending

trending

Ever since the time of Shakespeare’s Merchant of Venice, the question of how to trust that people in other countries would pay you in full and on time has kept merchants and consumers awake.

However, a raft of regulatory and technological improvements in recent years mean both businesses and consumers can expect faster, safer and cheaper cross-border transactions.

However, a raft of regulatory and technological improvements in recent years mean both businesses and consumers can expect faster, safer and cheaper cross-border transactions.

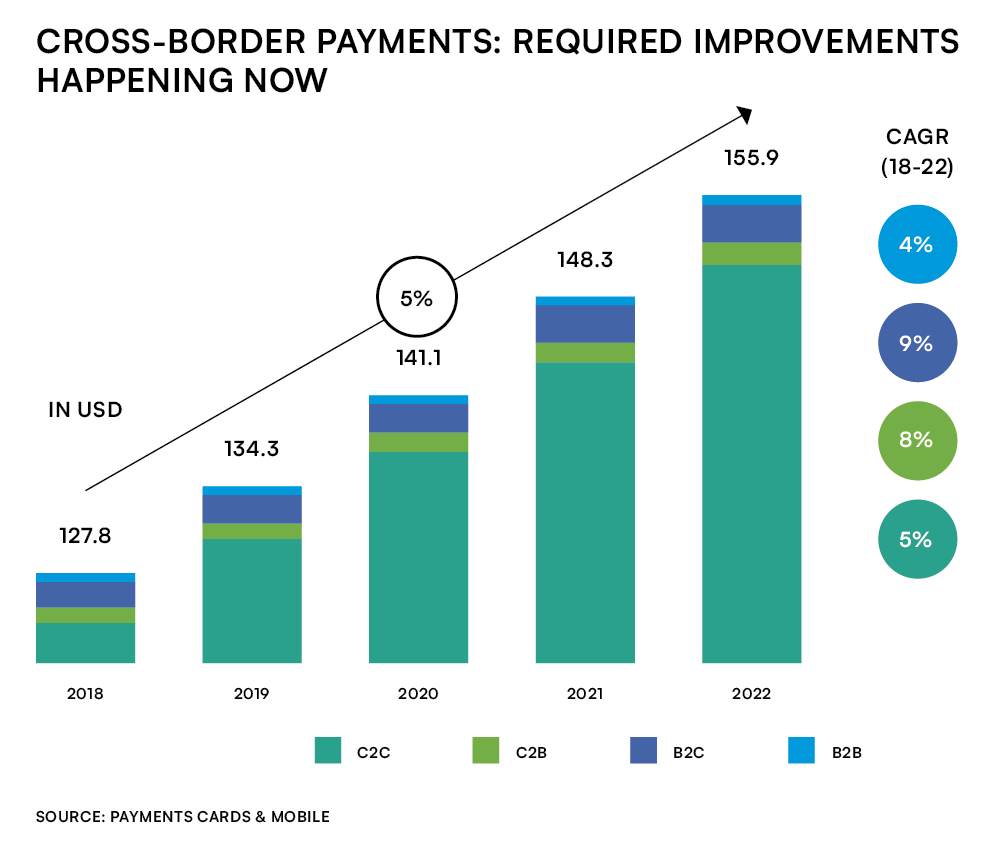

Certainly, demand for cross-border payments continues to rise, especially since more and more consumers are shopping online and businesses seek out higher quality suppliers willing to provide goods at lower cost.

As Payments Cards & Mobile has reported previously, cross-border payments reached $156 trillion last year, with business-to-business (B2B) payments making up more than 95% of the market by volume, but growing only half as fast as consumer payments across the board.

Historically, cross-border payments have been higher risk, higher cost and (much) slower to settle, with transactions taking up to five days to clear – a nerve-wracking experience, as anyone who has transferred large sums of money internationally will tell you.

This year, however, some regulatory changes are afoot that promise to make transactions faster and safer – if not necessarily any cheaper.

In the European Union, a mandate requiring banks to enable the instant settlement of cross-border transactions in Euros was introduced in October 2022 to be phased in over a 36-month period.

Although only around 13% of cross-border transactions in Euro are currently settled instantly, it’s expected that all cross-border B2B payments in Euro will be subject to instant settlement by Q1 2026.

Likewise, the global Financial Stability Board (FSB) has set a target for 75% of all international payments to be settled within an hour by 2027 – and global payments network SWIFT has just published findings announcing that almost 90% of transactions processed over its network reach recipient banks and are settled within an hour.

Problems remain in cross-border payments, of course – including the performance of regulators in some markets, and in particular a lack of transparency about transaction routing in others, or indeed the painfully slow process of transacting in and out of less popular currency pairs.

Overall, however, recent developments at least mean consumers and businesses can expect to see their money arrive much more quickly than before – even if the cost of transacting internationally remains very high compared to domestic transactions.

One promise made by digital commerce is the ability to pay for anything, anywhere, at any time over any kind of device: making cross-border transactions cheaper would go a long way to fulfilling that promise.

Comments