trending

trending

As Open Banking stumbles and consumers increase their digital footprint, mobile payments could end up dominating the landscape.

James Wood considers opportunities and risks in money on the move.

There are times when the buzz around a technology seems justified. Maybe not with the metaverse, as companies decrease their invest in this concept sharply – and maybe not even with AI, as we cover on pages 18-19.

Mobile payments, on the other hand, have real momentum – and as the capability of banking apps keeps advancing, they may end up a genuine challenger to cards and cash.

A broad church – and getting broader

To start with, mobile payments are a broad category. They can include digital wallets on mobile devices, any e-commerce or telephone payment executed via mobile, soft POS payments, carrier billing and more.

To start with, mobile payments are a broad category. They can include digital wallets on mobile devices, any e-commerce or telephone payment executed via mobile, soft POS payments, carrier billing and more.

As we’ll see, the range of possibilities via mobile is only expanding, making it likely that the already impressive growth rates we’ve seen in recent years could get stronger still.

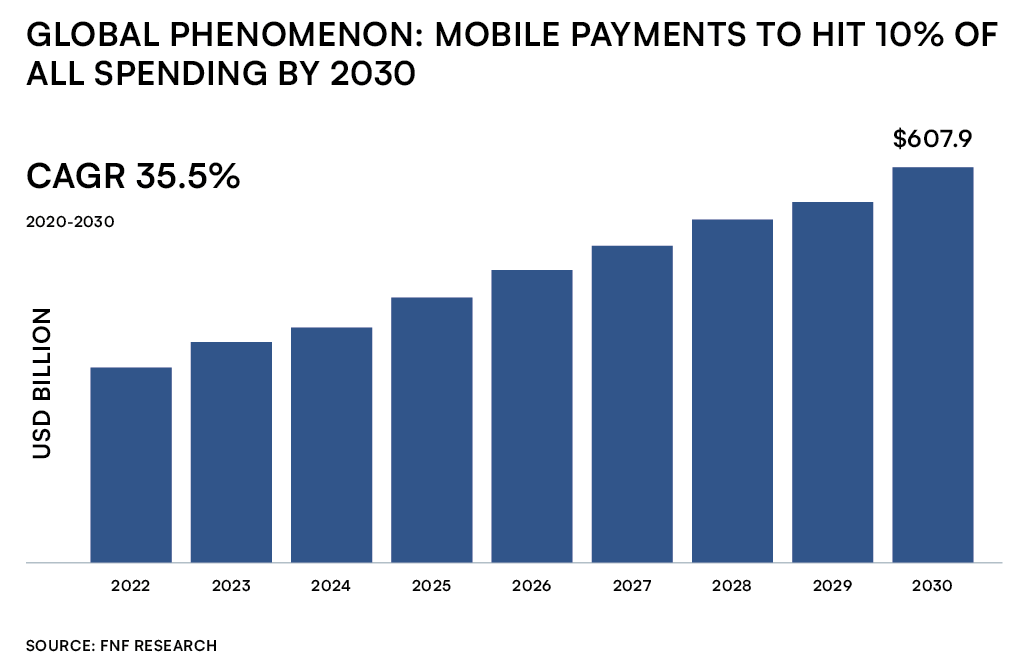

Faster growth would be quite a feat, considering that ECB data says mobile payments tripled between 2019 and 2022, moving from three percent of all payments to 10 percent by volume, and four percent to 11 percent by value.

The UK has not been slow on the uptake, either, with a third of the population now using mobile payments – up 75 percent in three years.

By the end of this decade, it’s likely one dollar in ten spent world-wide will be via mobile device.

Why the world’s going mobile

Just as there is a growing range of payment options via mobile, so there are many reasons for its runaway success.

Most obviously, smartphone penetration frequently exceeds the number of adults in any given market: in developing markets, as we cover in our new feature on Africa, there are more mobile devices than bank accounts.

The pandemic is another reason: people shopped more online, and when they did shop in person, they used digital wallets more frequently to execute contactless transactions.

“Mobile payment providers are creating amazing user experiences”

There are, however, other reasons why mobile is gaining ground so rapidly. Simply put, consumers love the convenience of being able to pay by phone – and the ability to conduct banking and payments via the same device.

As Andrew Boyajian, Head of Variable Recurring Payments at Open Banking payments specialists Tink says, “growth in mobile payments has been spearheaded by a focus by mobile payment providers creating amazing user experiences to drive consumer behaviours.

This includes anything from setting default travel cards that automatically work at transit terminals, or building partnerships with key merchants for more ubiquity and easier checkout flows.

Fraud risk spoils the fun

If it all seems too good to be true, then it usually is. The major risk with mobile payments – and, by corollary, mobile banking – is security.

Too many apps that include payment options are susceptible to being hacked – most commonly, consumers are duped by “phishing” emails that purport to be from a bank or other reputable organisation.

Developer portal build38.com say almost nine in ten US companies expect data breaches and cyber-attacks in the mobile channel to increase in 2024. The problem is that as people run more of their finances through mobile, more value is put at risk.

“Mobile drove 19% growth in fraud losses for US retailers last year.”

For some time now, Payments Cards & Mobile has argued that some form of comprehensive, multi-factor digital ID is the only way to resolve this problem in a world where Deep Faking is becoming increasingly sophisticated.

As Andrew Snyder, Vice President, MAPS at Zimperium puts it, “Mobile payments bring great benefits in ease-of-use and functionality, but malicious attacks are becoming increasingly sophisticated, resulting in fraud, identity theft, and reputational damage.

Research confirms that the amount of vulnerabilities, device exploits, mobile malware, and infected devices is growing at an alarming rate. To sustain the growth and adoption of mobile payments, efforts to secure these solutions will need to grow accordingly.”

“More needs to be done to deliver multi-factor digital ID on-device.”

Kaspersky internet security say that attacks on mobile devices were reduced last year as app security improved – but with between two and six and a half million attacks on mobile devices every month, there’s clearly room for improvement.

Worse news comes in the fact that these attacks are getting more successful, with mobile fraud driving a 19 percent rise in fraud losses for US retailers in 2022, according to SEON.

The clear implication is that multi-factor digital ID stored on-device is critical to further growth in the mobile channel – and the industry’s problem is that such schemes are still some way off either commercial application or widespread use, leaving mobile commerce – at present – at risk of exposure to a rapacious, ingenious criminal fraternity.

Moving down the line

The more consumers perceive risk in a technology, the less likely they are to use it. The attractions of mobile payments are growing, and new methods such as account-to-account payments are only going to increase mobile’s appeal.

But with risk in the mobile channel rising, a crunch point could come with horror stories of huge compromises or breaches and serious losses to consumers. The solution is out there, in the shape of comprehensive digital ID.

The first question is which organisation can bring a comprehensive digital ID solution to market that’s easy to use and widely distributed. The second question is the extent to which consumers are going to be comfortable putting their digital ID on their mobile device, given the perceived risk of compromise.

And finally, there’s the question of civil liberties: consumers today believe, probably correctly, they are being watched and spied on more than ever before. Will they be prepared to digitise their entire identity and put it out there on a mobile device?

Comments