trending

trending

A world leading payments environment is vital for a world leading economy and a healthy society. The economy cannot grow without a payments infrastructure to support it.

With this in mind the UK payments market undertook the Future of Payments Review. The review was initiated on July 10th 2023 and since then a small team have consulted with 150 people.

The team has conducted roundtables and listened to views from large and small financial institutions, Fintechs, Big Tech, Telcos, Consumer Groups, Regulators, Retailers, Merchants and Trade Associations.

UK Payments market key findings

Overall the report concludes that the UK payments landscape is in a good position with many positives.

Overall the report concludes that the UK payments landscape is in a good position with many positives.

First and foremost, the payments environment has a long track record of security, reliability, and resilience. The UK has historically been a leader on innovation in areas such as real time payments and Open Banking.

However, without question the strongest piece of feedback received through the review is that the UK’s payments landscape lacks vision and clarity of priorities.

This lack of vision and strategy means that it is hard to have high confidence in achieving a coherent outcome in 5-10 years’ time.

The strongest recommendation is therefore that the Government develops a national payments vision and strategy – particularly considering:

- The criticality of payments to consumers and the economy

- The many billions of pounds being invested

- The highly interdependent nature of the payments arena

This work should have a primary aim of simplifying the landscape over time. A healthy payments ecosystem is essential to a healthy competitive economy.

With a clear vision for the future, payments can help unlock GDP growth through fostering small business growth, frictionless trade, and Fintech innovation.

“The UK consumer benefits from a world-leading payments experience today – but it could be even better.”

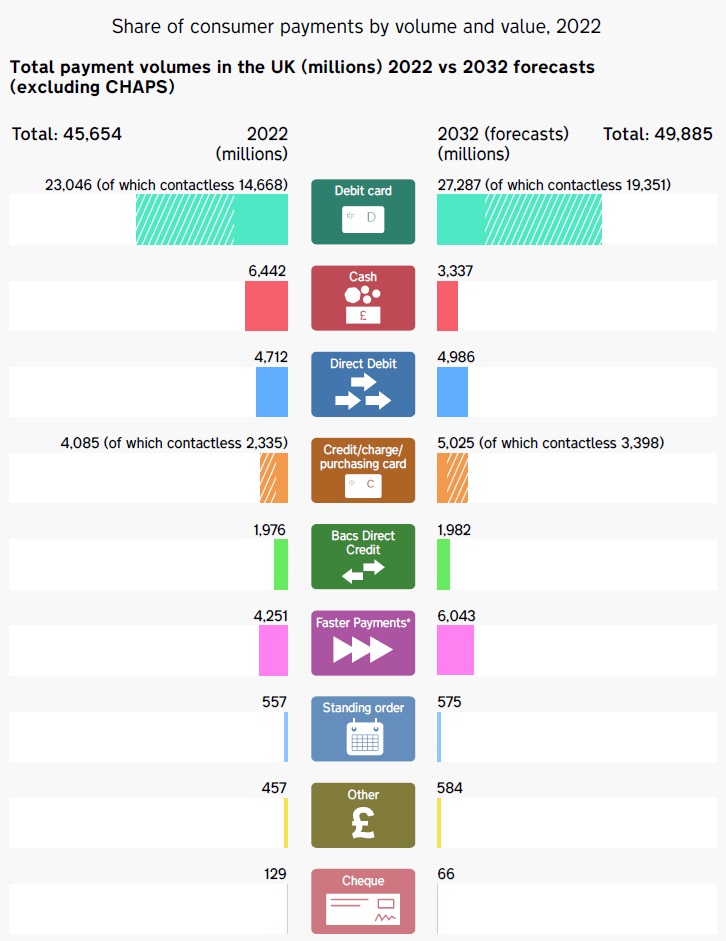

Turning to the specific payments journeys the review considered; the picture is mixed.

On the positive, the UK has a relatively mature banking, cards and digital wallets environment, and a well-developed regulatory environment.

Taken together this means that from a consumer point of view, the UK holds a leading position for the purchase experience of goods and services – both in-person and online.

There are some recommendations regarding Strong Customer Authentication (SCA) requirements that can make things even smoother for consumers at the point of purchase.

There is also support for the work to preserve access to cash, and concerns that digital exclusion could be adding to the financial exclusion problem. These issues need to be closely monitored.

On the negative, there are two significant issues in the retail space that need to be addressed.

First, the consumer-to-consumer bank transfer process is clunky (relative to international comparators) with the need to enter account numbers and sort codes. This needs to be improved in the coming years.

Second, many merchants and retailers are frustrated by the costs of taking card payments, and the lack of viable alternatives.

Open Banking

Firms and Fintechs are starting to innovate and use Open Banking capabilities to improve the bank transfer experience for consumers.

Open Banking could help improve the consumer-to-consumer process and (in time) provide an alternative to the card schemes for retailers.

However, there is currently no consumer dispute resolution process for Open Banking transactions, and the review notes that this will be a barrier to adoption if not addressed.

Likewise, the current commercial arrangements do not create the conditions for Open Banking to thrive in a healthy way, with costs and benefits misaligned.

If these issues can be addressed, there is optimism about the scope for innovation and the UK can use Open Banking to capture a world leading position in these areas.

“Even ahead of a National Payments Vision and Strategy, there are some actions that can be taken to declutter the environment and accelerate progress.”

The UK has a well-developed payments environment, but it is also very complex with multiple industry and regulatory bodies.

The review makes some suggestions on how to improve alignment and prioritisation with the intention of freeing up more space for innovation, advocating that on the high-profile issue of frauds and scams, there is increased focus on preventing the crime in the first instance.

A technology inflection point?

Finally, throughout it is observed how technology in general, and Big Tech in particular, are redefining not just payments but financial services in the process.

In 1994 Bill Gates predicted that technology firms will ‘bypass’ banks. The extremely rapid adoption of digital wallets (e.g. Apple and Google Pay) may indicate that we are at an inflection point.

This presents as much opportunity as threat and encourage an open and collaborative dialogue in the best interests of consumers, businesses, and the wider economy.

In summary, the UK has the opportunity to create a world leading payments environment long into the future. But to do this it needs to cut through the complexity and work towards a new shared vision consistently over the long term.

Comments