trending

trending

As Open Banking services approach take-off in some European markets and the US fires up its regulatory engine, we ask: how can banks make money out of Open Banking?

It’s not hard to understand the case for Open Banking if you’re a consumer – or a fintech.

From these points of view, Open Banking is a winner: consumers get access to a wider range of services through one portal – not always a bank – while fintechs that have long complained how hard it is to access consumer accounts finally get what they want.

That said, it’s more difficult to see what’s in Open Banking for, well, banks.

PSD2 in the European Union and the Competition and Markets Authority (CMA) order in the UK mandated Open Banking five years ago.

Understandably, perhaps, banks were not willing to open up access to their customer channels and data of their own accord and had to be “encouraged” by regulatory mandate to do so.

Sparks fly – but no fire yet

Since the launch of Open Banking in 2018, both bank and consumer reaction has been mixed.

The most successful markets in Europe have been the Nordics, Baltics and the UK. The success of Open Banking in the Nordics and Baltics, it could be argued, is hardly surprising given their relatively small, tech-savvy populations and nimble regulators – just 3% of all transactions in Norway these days use cash, for instance.

While the UK should be proud of its leadership in Open Banking, even the Brits have hardly rushed to take up Open Banking services.

The latest data from Open Banking Limited (formerly the Open Banking Implementation Entity, OBIE) suggests some 7 million UK consumers, or around 11% of the population, is currently using some kind of Open Banking service – up from 9% a year ago.

That’s progress: but hardly progress at the level seen in some South-East Asian markets where telecom and social media platforms have led the charge to Open Banking, rather than banks themselves.

“Some European markets do not have even one domestic Open Banking service on offer at present.”

Elsewhere in Europe, progress has been more mixed.

Private client research undertaken by Payments Cards & Mobile reveals some European markets have yet to adopt a single open API standard (such as the UK’s Open Banking Standard, or the Berlin Group’s NextGenPSD2 standard) and, in the worst cases, do not have even one domestic Open Banking service provider currently operating.

Concerns are sometimes expressed in European banking fora that Open Banking means bringing more intense competition on the banks themselves – often from competitors who do not face banks’ regulatory burdens.

In fact, recent research for Business Insider showed that banks in the UK alone could lose up to £6.5 billion of revenue to Open Banking services provided by fintechs and others by the end of 2024.

Given such figures, it’s not hard to understand bank reticence about the Open Banking revolution.

“Recent research shows UK banks could lose up to £6.5 billion through Open Banking by the end of 2024.”

What banks get from Open Banking

While some bankers may feel they are giving up their customer relationships and surrendering their data to competitors, the fact is that they hold a number of aces – especially in the highly regulated markets of Europe and North America.

Their status as regulated entities means they have developed infrastructures in compliance, regulation and KYC services that are time-consuming, expensive and complicated for fintechs to develop.

From a bank perspective, this gives them two opportunities – partnerships and selling their services as a bank to others.

When it comes to partnerships (mainly with fintechs) there are two goals: firstly, increase revenue and profitability by charging fees for use of the fintech’s services by bank customers.

Examples of such partnerships at work include Royal Bank of Canada’s use of NOMI’s personal finance tools for its customers, or the now widely-used credit scoring tools many British and American banks embed in their customer portals thanks to partnerships with Experian, TransUnion and more.

“When any platform can offer online financial services products, the survival of retail banks is no longer a given.”

The more important goal, though, is strategic: to retain the bank’s user interface at the centre of a consumer’s financial life.

As the examples of WeChat and AliPay in China show, once it becomes possible for other companies to offer financial services via the internet, the survival of retail banks is no longer a given.

From a social media chat service that offered peer-to-peer transactions, WeChat now provides everything from microfinancing for SMEs through credit cards and personal loans.

Show them who’s BaaS

However, Open Banking isn’t all bad news for banks.

That precious status as a regulated entity enables banks in the developed world to offer a wide range of services others are not permitted to sell – from credit products to accounts.

What’s more, card and payment platforms are by no means free to develop and maintain, meaning banks have a powerful set of services they can package and sell.

These facts have led banks to begin selling service packages to third parties – including fintechs and challenger banks – in areas such as transaction processing, credit cards and more.

Examples include Apple Bank powered by Goldman Sachs, and the Amazon Card powered by Synchrony.

The most recent announcements from some UK banks that they would bring their transaction processing back in house is another example of this.

The most recent announcements from some UK banks that they would bring their transaction processing back in house is another example of this.

Previously seen as a cost to be outsourced, banks have spotted an opportunity to offer transaction processing as a service to third parties.

Some banks have gone far beyond this and now offer Banking as a Service, or BaaS, packages.

In this scenario, third parties such as France’s Carrefour or Tesco in the UK partner with regulated banks like BNP and the Royal Bank of Scotland to deliver a full range of banking services.

At a time of thin margins and growing competition, BaaS makes sense for all parties: a wider range of services delivered by a regulated entity for the brand, and more revenue and profit for the banks.

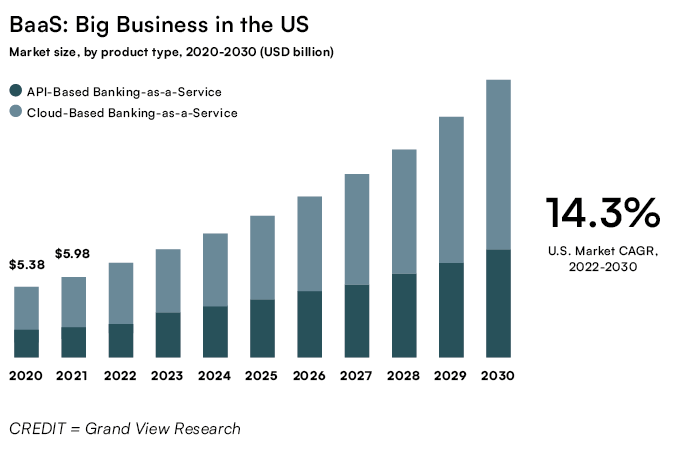

What’s more – back to that thin margin problem banks have – it’s big business, too.

Grand View Research predict that BaaS will grow by more than 14% each year out to 2030, and that 40% of that market will see banking services provided via open API, aka Open Banking.

Get out and sell

There are opportunities for banks in Open Banking – and not just through partnership or packaging their services and selling them to other companies.

Nick Chandi, CEO of Forward AI, a company that provides access to accounting services via open APIs, says banks have an opportunity to undercut other market players through Open Banking services.

One of the big areas where Chandi sees this happening is in account-to-account (A2A) payments, which use open APIs to enable consumers and businesses to pay each other directly through accounts without using payment cards, digital wallets or other stores of value.

“Banks should be looking to compete on the basis of the high transaction volumes they can generate thanks to holding customer relationships”, he says.

“If you take India as one example, card transaction interchange rates range between 1 and 1.5%. Banks can offer consumer A2A transactions to merchants at a rate that’s attractive compared to the card networks.”

In summary, banks should be embracing Open Banking instead of running away from it.

Unfortunately, current evidence suggests not enough retail banks – in Europe at least – have understood the scale of the opportunity they face, however much of a threat it may seem at first sight.

Comments