trending

trending

The latest Pix by the Numbers report covers data through Q3 2023, and shows Pix volume continuing to surge.

The report also offers key insights for US financial institutions (FIs) on the innovative ways to leverage instant payment rails as they focus on driving adoption of RTP and FedNow instant payment rails in the US.

The Latest Data

Matera reviewed data from the Central Bank of Brazil and noted several pivotal points in the shift to instant payments:

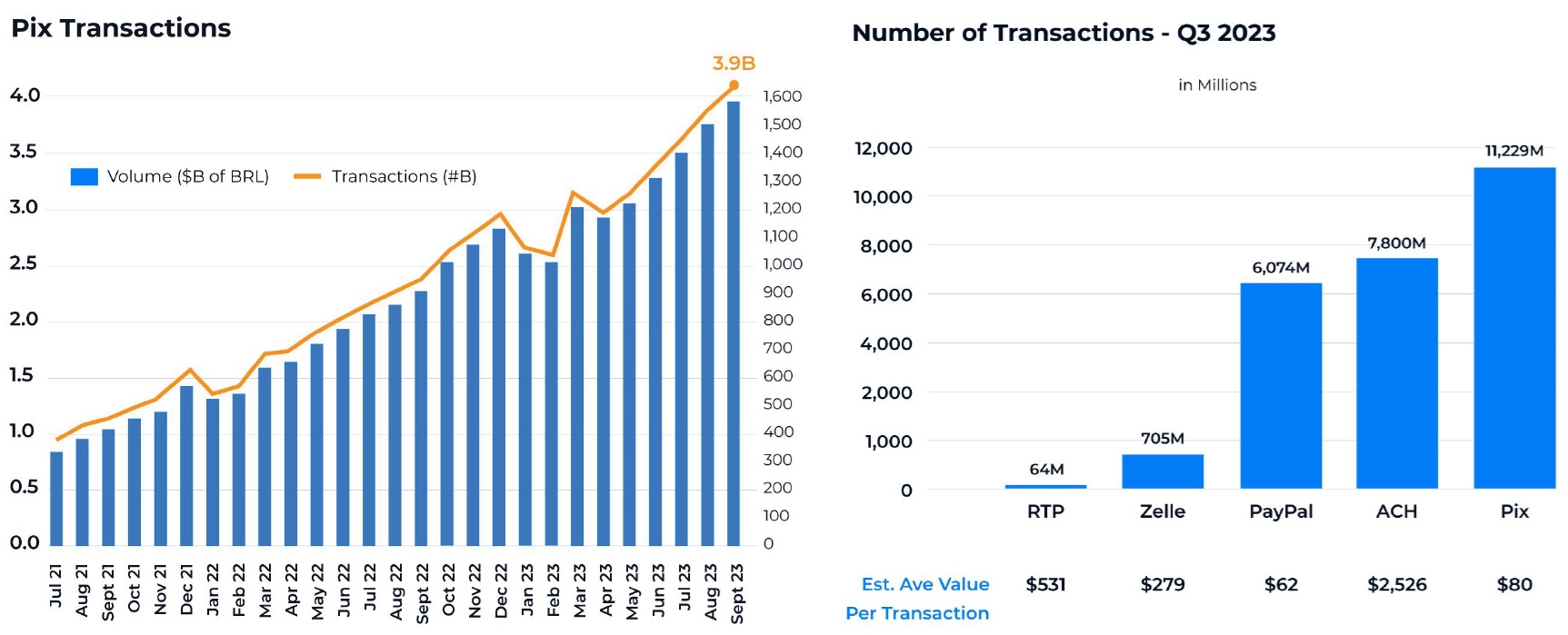

- Pix strong growth continues: Pix transactions in September 2023 totalled 3.9 billion vs. 2.3 billion in September 2022. This is a 70% growth rate YOY.

- Person to business payments are the fastest growing use case: 34% of all Pix transactions in September 2023 were consumers paying businesses – either transacting with merchants in-store or online or to pay billers. In September 2022, P2B transactions were only 22% of total.

- Innovation is driving Pix growth: Pix Credit, and Cross Border Pix payments are just two examples of how the Brazilian market is finding new ways to leverage Pix.

What It Means for the US

Instant payments adoption requires focus on user experience. While the Central Bank of Brazil required large institutions to offer Pix, consumers and businesses could still choose from many different payment methods.

Pix has become the dominant tender type because it’s easy to use, cheap, versatile to handle any use case, available 24X7 and safe.

In Q3 2023, Pix transactions exceeded 11 billion. This is 44% more than ACH transactions in the US and nearly double PayPal’s global transactions in Q2 2022.

While Zelle is growing at a swift clip in the US, its quarterly volumes are less than 1/10th that of Pix. And, RTP by The Clearing House has seen steady growth, but quarterly transaction volumes are in the tens of millions.

An average Pix transaction value was ~$80 in Q3 2023 compared to $279 for Zelle (Q2 2023), $2,577 for US ACH (Q3 2023), $573 for RTP (Q3 2023) and $62 for PayPal (Q2 2023)

Merchant Intervention

Merchants can change consumer payment behaviour.

Discounts and loyalty offered by merchants and billers helped convert consumers to pay with Pix. Merchants and billers tired of paying high prices to get paid for their goods and services willingly offer 10% off or more.

New revenue opportunities are emerging as the payment rail is leveraged for innovation.

Pix Credit is just one example where financial institutions can earn comparable revenues of a credit product and still settle payments instantly. It’s a win-win product; consumers can pay over time which helps sustain conversion rates for merchants, and merchants get paid instantly.

Credit card networks, processors and issuers in Brazil are all re-positioning their business to figure out ways to stay relevant as Pix continues to surge.

While it’s tough to predict when instant payments adoption will accelerate in the US, it’s clear there will be a land-grab of opportunities for players willing to commit.

“No one thought Pix would take off as it did in Brazil,” comments Carlos Netto, CEO of Matera.

“Financial institutions who weren’t ready to support their commercial customers with a Pix instant payment solution lost key, profitable business as a result.

US Financial Institutions have a strategic imperative to educate their commercial customers on the opportunities with instant payments, and test new use cases.

In the process they will surely find new revenue streams not possible with traditional payment methods.”

Comments