trending

trending

The payments industry’s 2022 performance, in terms of revenues and valuations, shows ongoing change with opportunities for growth and margin improvement across geographies and products.

A close look at revenues uncovers some structural changes, including new developments in instant payments and digital wallets according to the McKinsey Global Payments Report .

Also, recent public company returns suggest investors may be regaining confidence following the volatility of 2020–22.

Revenue results highlight the industry’s resilience

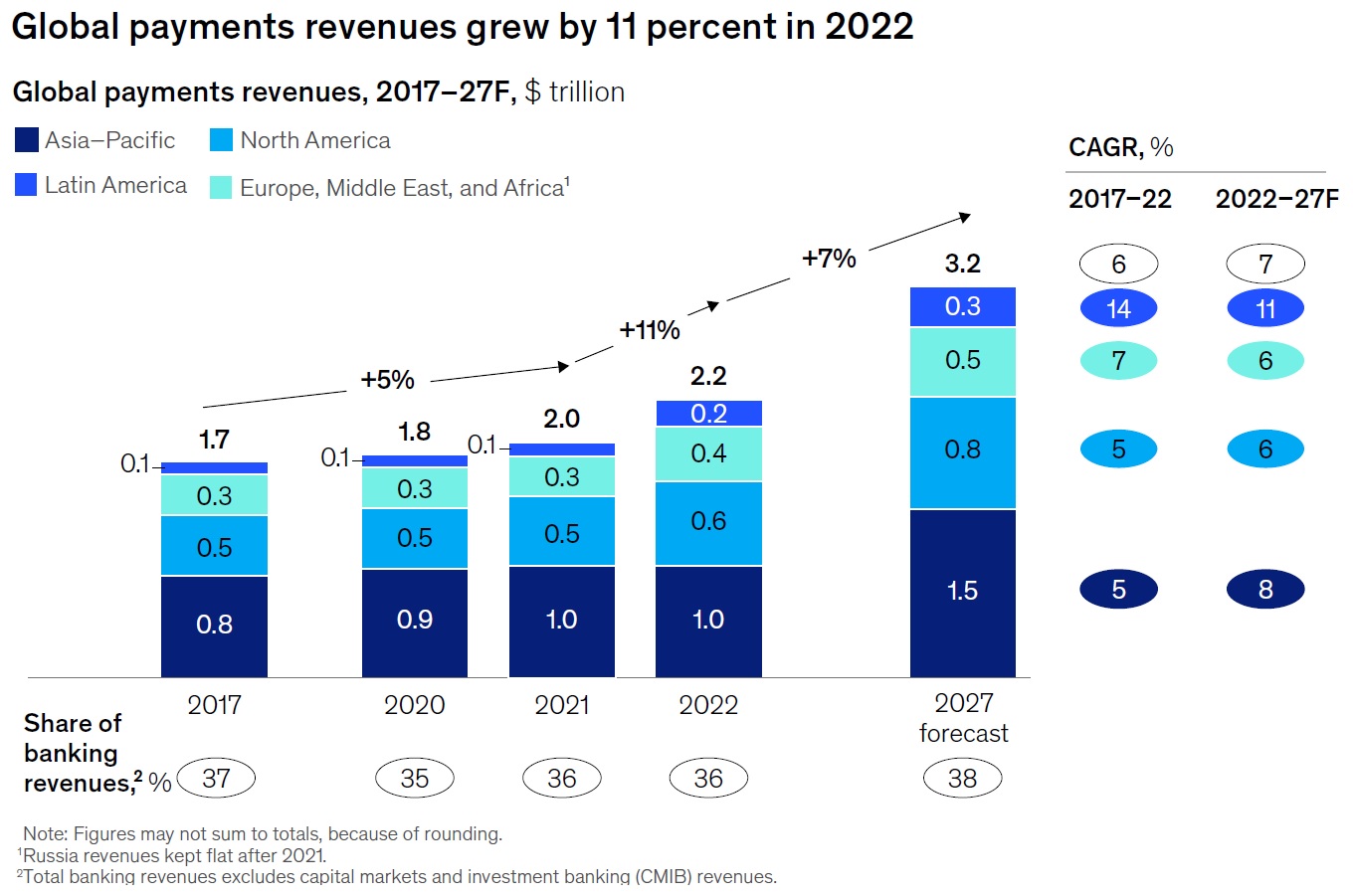

Globally, payments revenues proved remarkably resilient, overcoming a variety of regional headwinds to grow at rates well above the established long-term trend.

Payments revenues grew at 11 percent in 2022—a double-digit rate for the second consecutive year—reaching more than $2.2 trillion, an all-time high (see below).

Revenues by geography: Broad-based gains

Revenue growth was broadly distributed geographically, with three of the four regions posting their strongest increases in a decade. North America; Latin America; and Europe, the Middle East, and Africa (EMEA) all grew at double-digit rates.

The exception to this trend is Asia–Pacific. In recent years, this region, which accounts for 47 percent of global payments revenues, has served as the primary growth vector.

But in 2022, regional revenues rose just 4 percent, as a result of a 3 percent decline in payment revenues in China. Excluding China, however, the Asia–Pacific region grew at 25 percent—faster than in 2022.

Broadly speaking, the economies with the largest payments revenue pools delivered growth at or above the mean, contributing to 2022’s strong result.

This list, which includes Brazil, India, Japan, and the United States, posted solid results in both interest and fee-driven revenues.

A key factor in China’s results was the 5 percent decline in transactional fee revenue.

It fell to $255 billion as a result of smaller ticket sizes on card transactions and fee concessions implemented by payments providers to spur small and medium-size enterprise (SME) activity and counteract the COVID-19 macroeconomic shock.

By category, interest outpaced fees, commercial maintains lead

In many markets, about half of 2022’s revenue growth came from rising interest rates, interrupting a long-standing trend in which fees were the main source of growth.

The shifting interest rate environment had the greatest impact on the EMEA region, where net interest margins jumped markedly, reversing a trend of the past decade.

EMEA’s transaction-based revenue continued to grow at a steady pace (5 percent in 2022), while net interest income’s (NII) share of total revenues rose from 33 percent to 45 percent in a single year, bringing it closer in line with other regions.

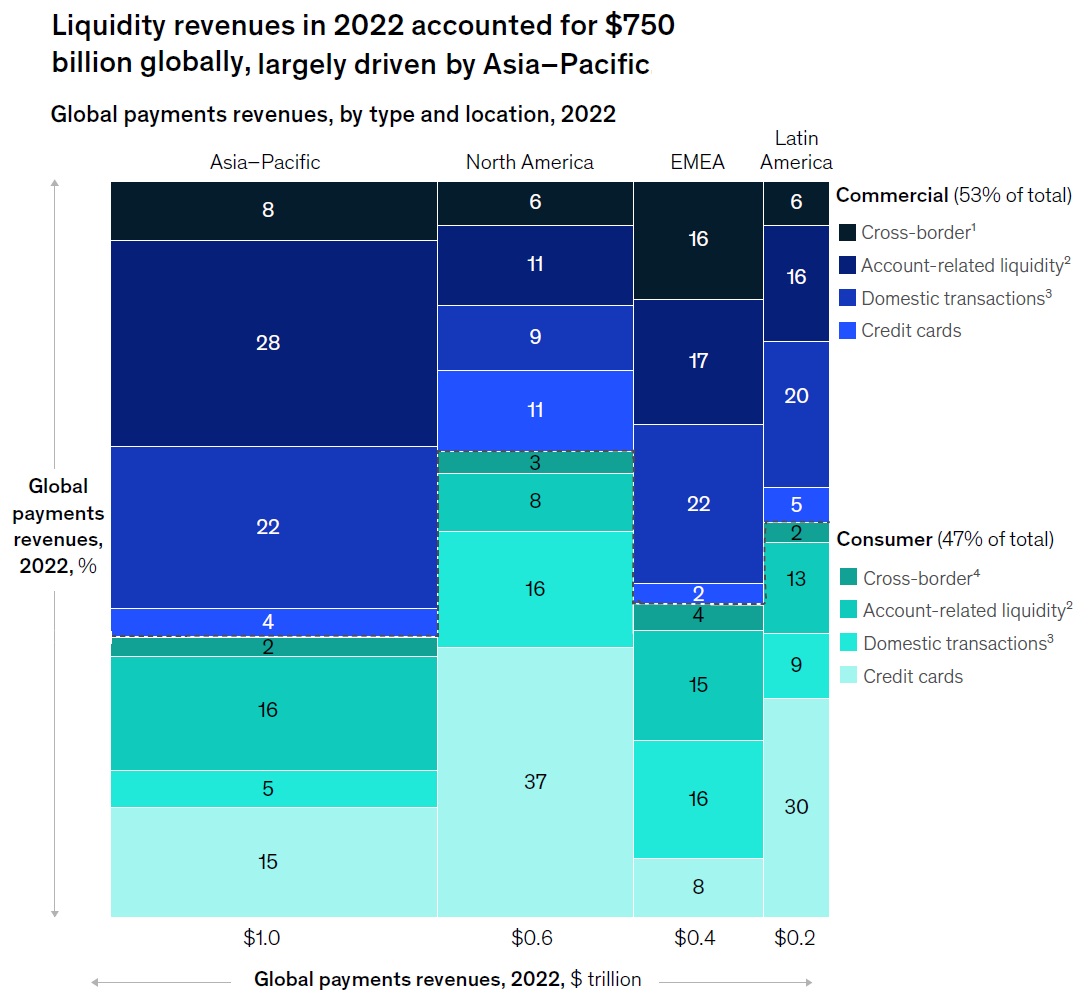

Another way to understand payments revenues is by customer segment (commercial and consumers) and the products that the industry delivers to each (see below).

The mix has been subtly but persistently tilting toward commercial across all regions for some time.

Overall, commercial now accounts for 53 percent of revenues and consumer 47 percent.

This proportion varies from region to region. Commercial revenues have long predominated in Asia–Pacific and EMEA.

Consumers still generate the majority in North America (63%) and Latin America (54%), where markets remain mostly card driven.

Cross-border payment dynamics were particularly robust. Flows reached about $150 trillion in 2022, a 13 percent increase in a single year.

This money movement generated an even greater increase in cross-border revenues, which rose 17 percent to $240 billion.

Revenues from cross-border consumer payments—both C2B and C2C— increased at double-digit rates, accelerating from high single digits in 2021.

Conversely, both forms of commercial payments (B2B and B2C) grew by 10 percent, somewhat slower than 2021’s post pandemic surge.

The United States–Latin America corridor remains the largest for C2C remittances, representing 11 percent of the total value of such flows. Central America has been an increasingly relevant destination for remittances and humanitarian aid from the United States.

While B2B remains the primary driver of cross-border revenue (69 percent of the total), the consumer categories carry higher margins and are projected to grow more rapidly over the next five years.

Much of the growth is expected to be in C2B, related to increased travel and e-commerce spending.

Comments