trending

trending

As cross-border payment volumes grow and technology becomes more sophisticated, we look at high-risk and lower-volume payments markets to find out what’s happening.

Is now the time for major international players to get involved?

Wild frontiers. Brave new worlds. While it all sounds very inspiring, it’s important – and revealing – to define what we mean by a “frontier”, or, “high-risk”, market.

When it comes to payments, fast growth and high risk don’t always go together.

For instance, the Law Society of England and Wales includes markets such as the UAE, Turkey and the Cayman Islands on its list of countries that are at high risk of money laundering payments – despite all three of these having solid rule of law and developed financial infrastructures.

At the other end of the scale, there are markets that might be considered as “emerging”, or, “fast growth” – only to reveal some aspects of growth, and therefore profit – that might seem disappointing to international players looking to invest.

Take Pakistan: on the face of it, it presents as a classic high-growth market, with cash-based transactions down 6.4% last year and a new instant payments architecture, Raast, introduced by the State Bank of Pakistan in 2022.

Scratch the surface, though, and other, more underwhelming facts appear, such as the fact that Pakistani e-commerce declined in volume last year.

Furthermore, while e-banking is rising fast, it’s still very much in its infancy, with only around 11% of the country’s population banking online.

High risk – and high reward

For the purposes of this article, we’re going to consider those markets that combine high risk with high reward.

On a regional basis, that means sub-Saharan Africa, much of Latin America, and Asian markets outside Japan, Singapore, Malaysia and China.

All of these geographies are characterised by rapid growth and high risks of various kinds, from significant fraud rates in Brazilian e-commerce through to low liquidity in markets like Malawi.

“Being able to pay – and get paid – is fundamental to investor confidence and economic growth.”

Companies doing business in Malawi cannot be sure of sufficient liquidity to enable the transfer of funds out of the country at any significant level.

On the other hand, demands for goods and services is such that any player able to invest with confidence will find rich rewards.

And being able to pay – and get paid – is fundamental to investor confidence, and vital for the economic development of these regions.

Sub-saharan Africa: plugging digital gaps

Part of the challenge in Southern Africa is, practically speaking, the capacity for governments to support new payments technologies at a systemic level.

While markets such as Kenya, Ghana and Nigeria have all invested in instant payment systems across their banking sectors, others – notably regional giant South Africa – still do not have a functioning instant payment system.

Outside the markets named above, banks and infrastructure providers are expected to invest in their own solutions, making the returns on a presence in some of these markets less attractive from an investor perspective.

Nonetheless, some markets are taking the plunge: Ethiopia has invested in a real-time payments infrastructure with Swiss banking services provider BPC, while Malawi’s Central Bank partnered with the Tony Blair Global Institute on the provision of electronic payment for government services across the country.

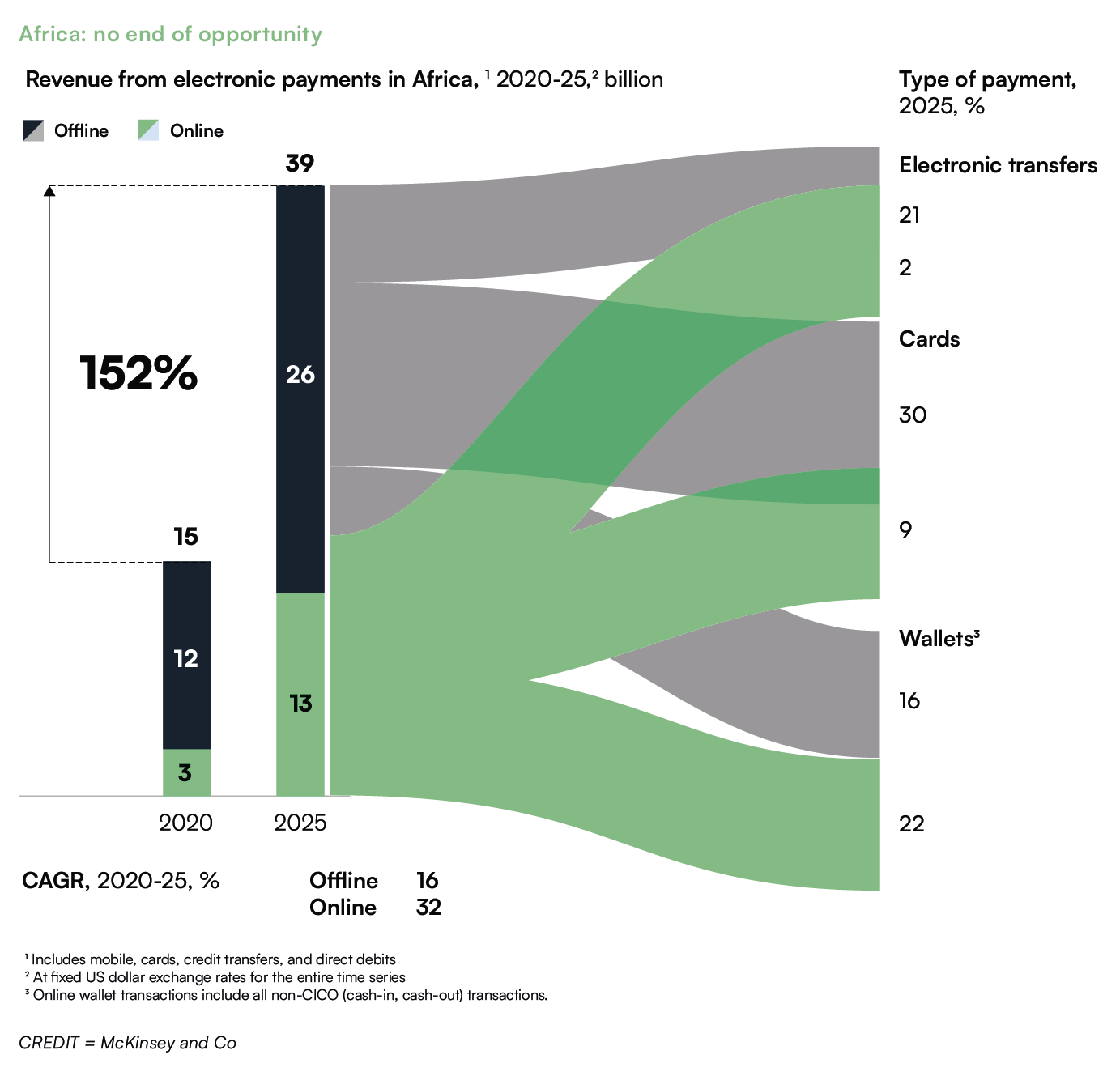

If effort is required on the part of international players, then the rewards are there: McKinsey & Co expect growth in African e-payments of 152% over the next three years, chiefly driven by smaller-value transactions made via mobile device.

Indeed, the work-arounds currently employed both for low liquidity and the absence of payments infrastructure could themselves pose a challenge for external investors.

After all, if it works for a company to bring US dollars in and out of a market, then switch to local currencies via paper-based transactions through local banking partners, why change?

Likewise, if telecom operators can provide peer-to-peer transfers as quickly as account-to-account payments, why switch?

“Growth in African e-payments is set to rise at 152% over the next 3 years.”

The short answers are: time and money. While so-called “mobile money” operators can transact funds rapidly, they still have to hold huge sums of money on account to cover settlement – hardly the most efficient use of capital.

Likewise, companies may be able to do business in dollars – but they won’t escape the headache of lots of paperwork and slow remittance of the money they owe to local suppliers.

Nkosi Moyo, Head of Global Payments at Crown Agents Bank, sees both banks and governments now shifting to invest in more automation and modern techniques such as the use of AI in controlling fraud risk.

He says that initiatives such as Pan-African Payment and Settlement System, or PAPSS, will make a huge difference.

Supported by the African Union and Afreximbank, PAPSS aims to deliver real-time transactions across borders throughout the continent.

“Once instant payments rails are operational, the rest will fall into place”, Moyo says. “We’ll see more investment by both financial institutions and central banks into broader payments infrastructure.”

Similar infrastructure problems beset Central Asian economies when it comes to payments.

The problems referenced above for Pakistan apply elsewhere across former Soviet countries such as Azerbaijan and Kyrgyzstan: while there’s a rapid and pronounced switch from cash to electronic payments, there is, quite simply put, not enough money to develop a coherent faster payments network in-country and, as many of these republics become more decoupled from Russia as a provider, arguably less incentive to develop a domestic system of their own.

It may be that the “Stans” either develop an independent payment network of their own outside Russia’s MIR system – or, more likely, turn to international giants such as UnionPay, Mastercard or Visa to help them develop this kind of system.

“Public-private partnerships would be a neat solution to the challenges facing some of these markets.”

Latin America presents an altogether different challenge for investors – while growth has been robust, especially in digital transactions, persistently high rates of fraud has increased the risk of losses and the cost of doing business, as international players seek to protect themselves against financial crime.

While e-commerce volumes are currently rising at around 30% a year in Latin America and stood at 16% of total retail last year according to EBANX, such rapid growth opportunities need to be balanced against higher risks and costs.

Across the board, it feels like public-private partnerships would make sense as a cost-effective means of building infrastructure and controlling risk, while making these frontier markets more attractive for investors.

How quickly such partnerships will happen depends entirely on the extent to which governments and banks in these markets recognise the centrality of safer, faster payments to the more rapid development of their economies.

Whether online or in the real world, it appears the penny is dropping at different speeds from market to market and region to region.

Why payments matter for economic growth

Governments in frontier markets should be as excited about payments innovation as the payments industry.

Although hampered by political risks, regulation and sometimes the most basic of problems – such as sufficient liquidity to support payments in and out of countries – there’s no doubt that modern payment systems make a huge difference to economic development.

Non-cash digital payments grew at twice the rate (25%) in emerging markets compared to developed markets (13%) last year, according to the World Bank.

While this is great news for the speed at which money moves around these economies, it creates regulatory headaches for governments who are struggling to keep up with the pace of change.

Crypto is blooming.

10 of the top 20 countries on the 2022 Global Crypto Adoption Index from Chainanalysis were classified as lower-middle-income countries, while eight were upper middle income.

Vietnam, the Philippines, Ukraine and India were the top five users of crypto in the world.

Despite sharp declines in value, Bitcoin was adopted as legal tender by the Central African Republic in April 2022.

Egypt, Kenya, Nigeria and South Africa, Africa’s four-largest economies, also boast the largest number of cryptocurrency holders on the continent.

Funding for small businesses. Alternative payment solutions play a key role in building financial resilience in frontier markets, where conflict, inflation and natural disasters can have an outsized economic impact.

For many lower-income countries, limited access to credit remains a major obstacle to growth and formalisation.

According to the International Finance Corporation, some 65 million firms – approximately 40% of all MSMEs – face an annual funding gap of $5.2 billion, indicating a sizeable opportunity for fintech operators.

One recent fintech innovation, BNPL, is already unlocking e-commerce potential in emerging markets and has the potential to narrow the credit gap for MSMEs.

From “banked” to “walleted” – as the figures for Non-Cash Digital Payments and crypto usage make clear, the old statistic, often touted, that there are huge unbanked populations in frontier markets is true – but misleading.

While there may still be 1.4 billion adults without bank accounts worldwide, many of these people hold digital wallets or use P2P transfer services of some description – and these services are blossoming into microlending, credit and money transfer operations – many of the key features of traditional branch banking.

Comments