trending

trending

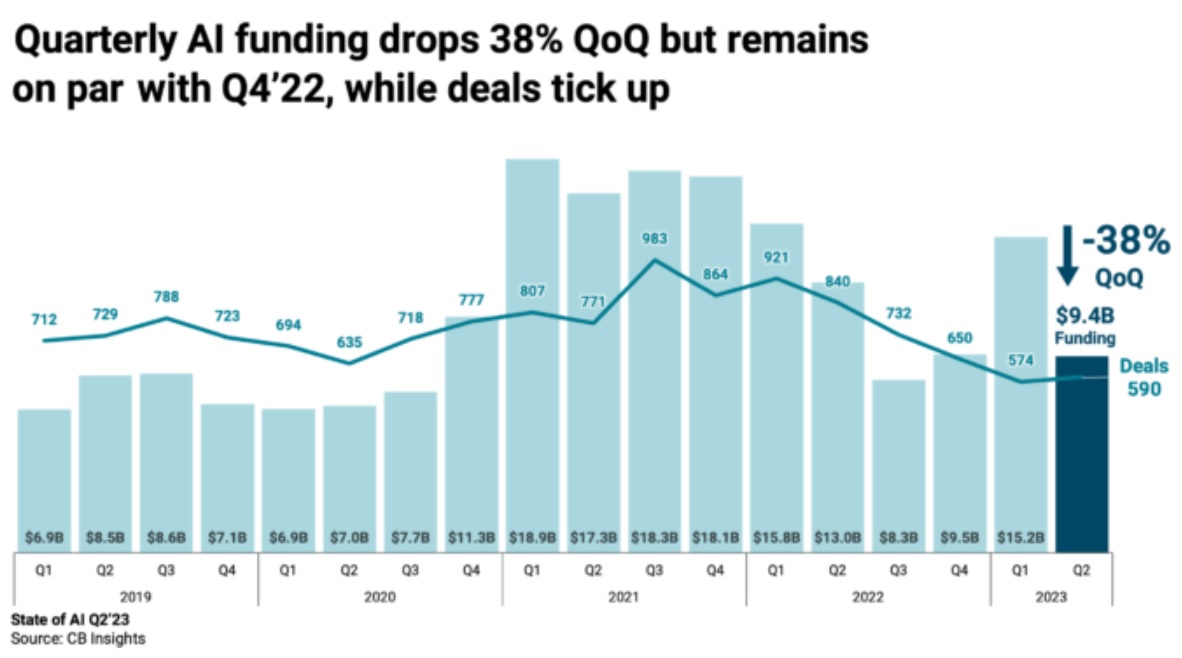

Amid the broader venture gloom, generative AI mega-rounds and unicorn births have kept AI investment levels relatively elevated, with Q2 2023 funding coming in at $9.4 billion.

Using CB Insights data, we dig into key takeaways of their State of AI Q2 2023 Report, including:

- Global AI funding in Q2’23 drops 38% QoQ (Quarter on Quarter), but remains on par with Q4 2022.

- The average AI deal size is up 48% in 2023 YTD, driven by mega-rounds.

- Q2’23 welcomes 7 new AI unicorns — including 5 generative AI companies.

- M&A deals increase by 13% QoQ, while public exits remain subdued.

- Funding to Canada’s AI start-ups surges by 13x QoQ.

Global AI funding — which spiked in Q1 2023 due to OpenAI’s $10 billion round — fell to $9.4 billion in Q2, a 38% drop quarter-over-quarter (QoQ).

However, if excluding OpenAI’s January mega-round, Q2 funding would have actually grown 81% QoQ.

Deals to AI start-ups ticked up for the first time in 5 quarters to reach 590 in Q2 2023. Over 40% of these went to US-based start-ups.

The buzz around generative AI continues to draw investors’ attention: Four of the top 5 largest funding rounds this quarter went to genAI companies.

At $29 million, the average deal size for AI companies in 2023 YTD has grown nearly 50% compared to 2022’s full-year total.

This is partly due to the genAI boom, with start-ups like Inflection AI, Cohere, OpenAI, and Anthropic attracting the top $100 million+ mega-rounds this quarter. Overall, the number of mega-rounds nearly tripled QoQ to reach 22 in Q2 2023.

The AI sector saw 7 private companies reach $1 billion+ valuations in Q2 2023. For comparison, the broader venture market saw just 18 new unicorns this quarter, meaning 2 out of every 5 new unicorns are AI companies.

Generative AI accounted for 5 of the entrants to the unicorn club, with Cohere, Replit, Runway, Synthesia, and Typeface all gaining $1 billion+ valuations.

Of the 7 new AI unicorns, 5 are based in the US, 1 hails from the UK, and 1 is in Canada.

There were 86 AI M&A deals in Q2 2023, an uptick of 13% QoQ for a third straight quarter of growth. Public exits remained sparse for AI companies with just 2 IPOs and no SPACs, consistent with Q1’23.

The US accounted for the largest share of global AI exits at 35% in Q2 2023, with Europe following closely behind at 33%.

Canada saw the greatest increase in AI funding among regions, surging over 1,000% QoQ to reach $693 million in Q2 2023.

AI deal count also jumped 35% to 23, the region’s highest level in 4 quarters. This funding surge was driven by mega-rounds to genAI model developer Cohere and AI traffic management startup Miovision.

Meanwhile, Asia and Europe saw more modest upticks in funding, growing 29% and 20% QoQ, respectively.

Comments