trending

trending

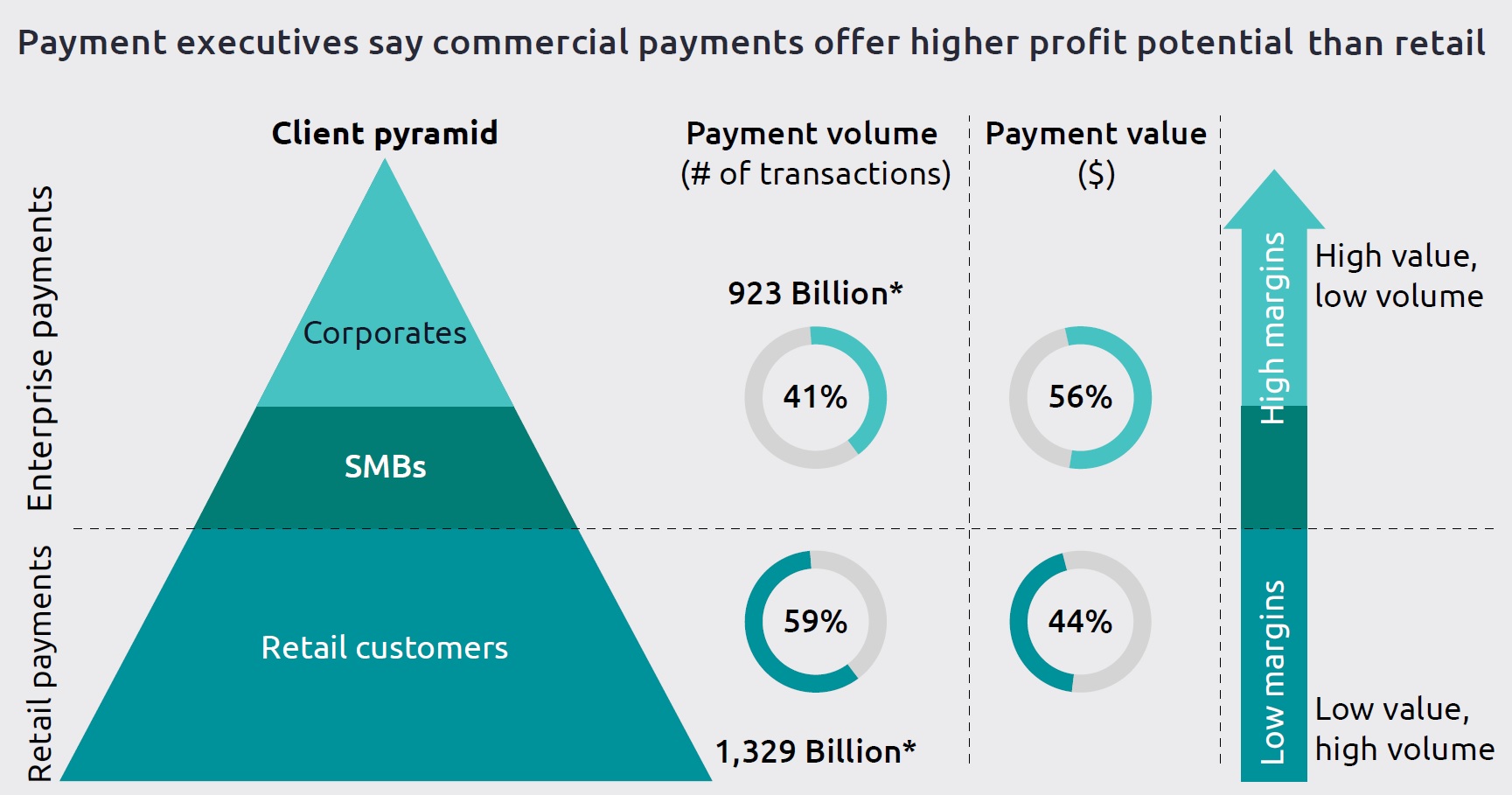

The World Payment Report 2023 Executive Survey results indicate that retail payments comprise 59% of total transaction volume while commercial payments comprise 41%.

However, in terms of value, commercial payments make up nearly 56%, while retail accounts for only 44% of total payments value.

Shares of value and volume change from region to region. In the Americas, commercial and retail payments account for 54% and 46% of total value, respectively.

In Europe, commercial and retail payments account for 62% and 38% of the share, respectively. And in the APAC region, the split between commercial and retail payments value share is nearly 50% each.

Globally, more than one in two payment executives agreed that commercial payments offer better profit potential than retail payments.

In Europe, this perspective is even more pronounced as nearly 56% of executives believe commercial payments have more high- profit potential than retail.

Global non-cash commercial payments will grow at compound annual growth of nearly 11.3% (2022–2027), primarily driven by Asia Pacific.

From a regional perspective, Europe leads the non-cash transaction volume share, followed by North America. APAC comes in third in value share yet is fast-trending to a 14.6% CAGR during the forecast period.

![]()

Nearly three-quarters (74%) of surveyed payments executives ranked the entry and building scale of new-age players (FinTechs and PayTechs) as drivers for growth in non-cash commercial payments in the forecast period.

Most new-age players seek to improve their unit economics profitably, and commercial payments offer a stable source of revenue with a smaller pool of competitors and long-term engagement scope.

As a result, challengers are launching commercial payment products and services to target SMEs, if not large global corporations.

As one example, the UK’s cloud-native Starling Bank launched a business ecosystem to target and nurture SME client relationships.

Commercial payments are catching up quickly with digital payments trends

Enterprise clients demand retail-like payments from banks and payment firms, such as digital and efficient experiences.

More than 60% of payment executives agreed that the demand for a better payment experience accelerates commercial payment digitalization.

Marc Andrews, Vice President, Financial Services and Insurance Industry Market Leader from Pega, said, “Commercial banking has been slower to implement digital automation and engagement capabilities in general.

However, things are beginning to change as their clients seek real time transparency into payment status and faster response to requests, especially when there is a processing problem or need to make a change, which can significantly impact corporate cash management.”

Regarding payment methods, around 60% of the corporate executives surveyed as part of the World Payments Report 2023 ranked commercial cards as the leading instrument.

Suppliers become stressed during periods of high inflation if payments are delayed significantly from the invoice date. High inflation makes money less worthwhile over time.

As a result, traditional payment instruments, such as paper checks, become less effective for all value chain stakeholders, making commercial cards a preferred choice.

Rising interest and acceptance of commercial cards are also fuelling innovation.

Card operators seek to deliver integrated value-added services such as highly configurable spend-control features, expense management, reporting, and budgeting tools for efficient and real-time visibility into enterprise spend.

In 2023, AMEX and Microsoft collaborated to build AI-powered intelligent expense management and reporting features for businesses.

In addition to cards, nearly 45% of corporate executives ranked digital wallets among the top three preferred payment instruments.

Another one-third of corporate executives ranked A2A payments as the preferred payment method.

With instant payments and real-time payment infrastructure maturing across critical markets, A2A payments and digital wallets are heading toward a watershed moment.

However, traditional payment methods are still relevant. For example, 57% of corporate executives said credit transfers and direct debits on conventional rails (ACH, SCT, etc.) are suitable payment methods.

Moreover, 37% of corporate executives said they still use paper checks as a payment instrument.

Commercial payments are fast catching up with the overall digital payments trend – borrowing innovation from retail to meet evolving corporate client demands.

And a particularly important aspect of commercial payments is cash management services.

Cash management revenue for banks suffered during the global pandemic in 2020; however, in 2022, it is now back on a growth trajectory because of growing corporate deposits and high net interest margins.

The accelerating shift away from paper-based processes, rising adoption of digital transactions, and FinTech collaborations are all contributing to fast evolution within the commercial payments segment, offering new and expanding cash management value pools for banks and payment firms.

However, maximizing value from cash management services require banks and payment firms to engage and meet the changing expectations of enterprise clients.

Comments